This policy brief is based on ECB Working Paper 3177, also published as IMF Working Paper 2025/125. The views expressed are those of the authors and do not necessarily reflect the official views or policies of the institutions with which the authors are affiliated.

Abstract

The EU’s Carbon Border Adjustment Mechanism (CBAM) is designed to reduce carbon leakage and level the playing field between EU and non-EU producers as EU climate policy tightens. Using input-output tables and sector-level carbon intensity data of CBAM-covered imports, we simulate the implied carbon fees for EU member states and their trading partners. We find that the direct, first-round impact of the current CBAM design is modest overall. On average, CBAM would increase the value of EU imports by about 0.1% and the cost of non-EU exports to the EU by around 0.04%, with a maximum of 1.2% for the most affected country. However, the impact is highly concentrated with certain products — notably iron, steel and aluminium — and some individual suppliers face much higher costs. This concentration helps explain the political salience of CBAM despite its limited aggregate trade effect. Looking ahead, a broader sectoral coverage and higher carbon prices could turn CBAM into a more material driver of trade costs and international climate policy incentives.

Countries that are more ambitious in cutting greenhouse gas emissions face a dilemma: achieve their emissions reduction objective without weakening their competitiveness vis-à-vis less ambitious partners. Tightening mitigation policy raises domestic production costs, especially in energy- and emissions‑intensive sectors. To comply with stricter climate regulations, firms must invest in cleaner technologies, pay carbon taxes, or surrender emission allowances. These measures incentivise decarbonisation, but they may weaken international competitiveness in the short to medium term.

A related concern is carbon leakage, i.e., the relocation of CO₂‑intensive production from jurisdictions with stringent climate policies to those with laxer rules and, potentially, more emission intensive production technologies. If emission-intensive manufacturing activity simply votes with its feet in response to more stringent domestic climate policy — shuffling around rather than reducing global emissions — the environmental benefits of ambitious unilateral policies are undermined, and the political support for unilateral climate action may erode.

The leakage risk is particularly acute in high‑emitting, trade‑exposed sectors such as steel, cement, aluminium and fertilisers. To date, most jurisdictions have tried to protect these sectors through relatively simple tools such as exemptions from carbon pricing, free allocation of emissions allowances, and output-based rebates or direct compensation schemes. These measures reduce apparent competitiveness risks but have been increasingly criticised for weakening the carbon price signal, distorting incentives to decarbonise, and limiting fiscal revenues. The EU’s response has been to shift away from such mechanisms and toward a border-based approach that aligns climate ambition with trade policy: the Carbon Border Adjustment Mechanism (CBAM).

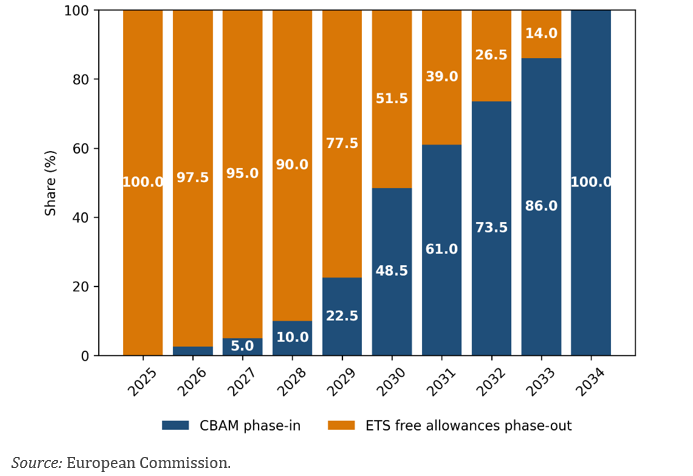

Introduced in October 2023 as part of the EU’s ‘Fit for 55’ package, the CBAM complements the EU Emissions Trading System (ETS). It is set to gradually replace — between 2026 and 2034 — the free allocation of emission allowances to industries at risk of carbon leakage, according to the schedule depicted in Figure 1. The objective is to level the playing field between EU producers (subject to the ETS) and foreign competitors while reducing the risk of carbon leakage as the EU tightens its climate policy.

Figure 1. Timeline for CBAM phase-in and ETS free allowances phase-out (Percent)

Several design features of the CBAM are relevant in assessing its effects, particularly in terms of environmental effectiveness and administrative feasibility.

In contrast to some conceptual proposals in the literature, the current CBAM does not include export rebates. EU producers exporting to countries without carbon pricing still bear the full domestic carbon cost, while competitors from jurisdictions without comparable carbon price signals do not. This asymmetry may become more salient as free allowances are phased out and EU carbon prices rise.

The CBAM has attracted some criticism, especially from developing and emerging economies. It is perceived as a de facto trade barrier, increasing the cost of exporting to the EU and potentially distorting global trade patterns. Critics also argue that it contradicts the principle of ‘common but differentiated responsibilities’ by imposing similar carbon costs on countries with very different historical emissions and income levels. Furthermore, it entails potential risks of retaliatory measures and escalating trade tensions. Indices such as the CBAM opposition index developed by Overland and Sabyrbekov (2022), for example, suggest that opposition is strongest among countries with a high share of CBAM‑exposed exports to the EU, high carbon intensity in these sectors, and low levels of technological capability and innovation.

Given these sensitivities, quantifying who is directly affected — and by how much — is crucial for an evidence‑based policy debate.

In Dolphin and Ferrucci (2026), we develop a simple analytical framework to quantify the direct trade cost implications of the EU CBAM. We use 2021 sector‑level input‑output tables and sectoral carbon intensity data to estimate the embedded CO₂ content of EU imports in CBAM‑covered sectors. For each exporting partner and product, we calculate the implied CBAM carbon fee, expressed as an ad valorem tariff equivalent — that is, as if the CBAM were an extra percentage tariff on EU imports and countries’ exports to the EU.

The analysis is intentionally partial equilibrium. It assumes current trade patterns continue, without modelling how exporters or importers may adjust quantities, re‑route trade, or change production technologies in response to CBAM. It ignores potential knock‑on effects on downstream industries within the EU that use CBAM‑covered goods as inputs. It also does not endogenise the impact of CBAM on the EU ETS carbon price, even though the CBAM is expected to influence prices in the EU ETS by affecting production and emissions levels. As such, the estimates are best interpreted as upper‑bound, near‑term, first‑round effects of applying the full CBAM levy to today’s trade structure.

Despite the limitations, a partial equilibrium approach is fit for the purpose of our analysis, as it allows for a detailed product-by-product impact assessment while avoiding both the undue complications and the excessive simplifications associated with a general equilibrium framework.

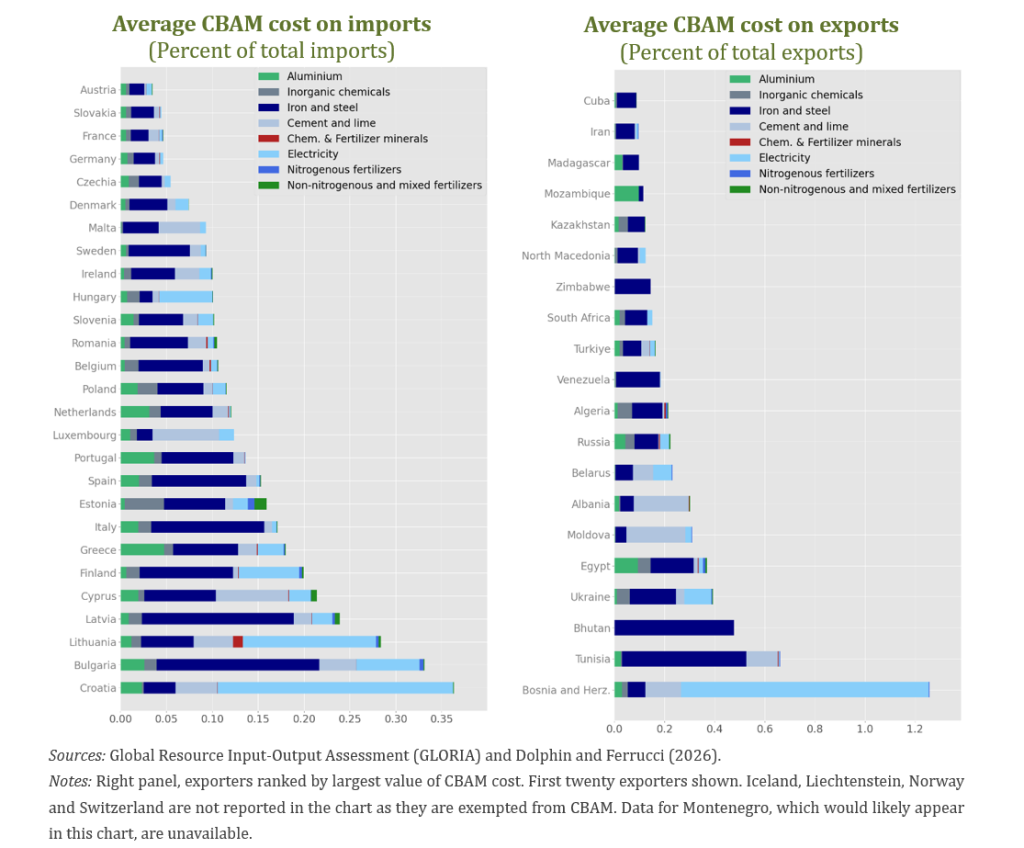

Across the EU and its trading partners, we find that the aggregate direct cost impact of the current CBAM is limited, ranging from 0.025% of the value of total imports in Austria to 0.35% in Croatia (Figure 2, left panel). On average, CBAM would add approximately 0.1% to the value of EU imports.

For non‑EU trading partners, CBAM translates into an average additional cost of about 0.04% of their exports to the EU, with a maximum impact of 1.2% for the most exposed country (Figure 2, right panel).

Figure 2. Trade-weighted CBAM cost

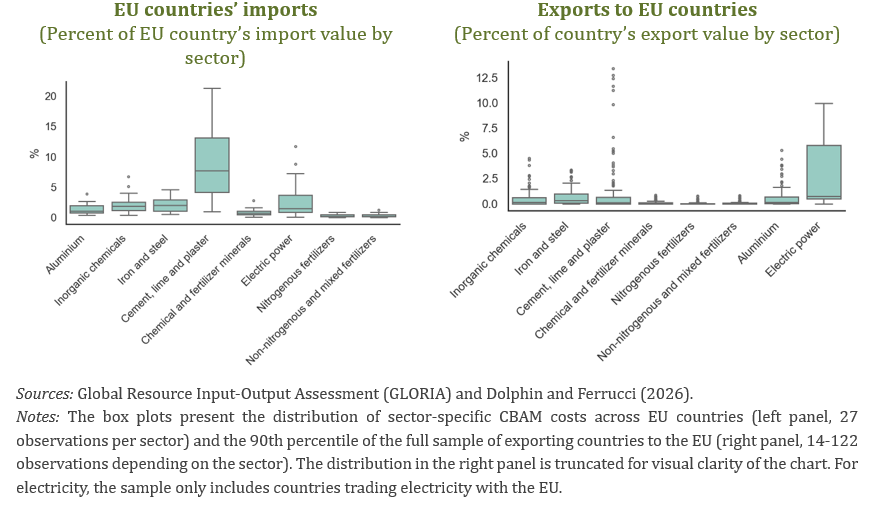

However, the aggregate picture hides important concentration of costs. Cement, electric power, iron and steel, and aluminium stand out as sectors where CBAM‑induced costs can be sizeable, particularly for exporters with high emissions intensity (see Figure 3). For some individual countries heavily specialised in these CBAM‑covered products, the implied ad valorem equivalent can reach levels that are politically and commercially meaningful, even if their economy‑wide average remains small. This concentration helps explain why CBAM has attracted strong political reactions from a subset of countries, despite the average effect remaining modest relative to the total value of these countries’ exports.

Figure 3. Product-level CBAM cost

Our analysis suggests that, at current scope and carbon prices, CBAM costs are manageable even for the countries that will be most affected by its full implementation, with CBAM likely to trigger adjustments, but no major disruption in trade flows. Yet its sectoral and country‑specific impacts are non‑negligible and politically salient, especially in the trade of cement, electric power, iron, steel and aluminium. This leads to several policy implications.

For EU policymakers, the concentration of costs implies that a small group of trading partners is likely to be disproportionately affected, particularly as the scope and coverage of CBAM expand and carbon prices increase. Phased implementation, as currently planned, together with transparent communication, can help ease tensions with trade partners. In addition, targeted climate‑finance and technical‑assistance initiatives could support low‑income exporters in their decarbonisation efforts.

The absence of export rebates may also need to be reconsidered if the carbon price differential between the EU and non-EU countries widens over time, and EU exporters face intensifying competition in third‑country markets. However, implementing export rebates could raise concerns about their consistency with WTO rules. Their design will need to strike a careful balance between these conflicting objectives.

For non‑EU trading partners, the fact that CBAM allows a credit for comparable domestic carbon pricing means that countries developing credible carbon pricing systems can partially offset the mechanism’s impact on their exporters. This strengthens the incentive to adopt or deepen domestic climate policies — which is one of the objectives of CBAM — especially if accompanied by domestic recycling of carbon revenues to address distributional concerns.

CBAM sits at the intersection of climate policy and trade policy. While the current evidence suggests limited aggregate trade disruption as CBAM is progressively phased in, the mechanism has broader strategic implications. It can support global decarbonisation by limiting leakage and nudging other regions towards explicit carbon pricing. But if perceived as unilateral or protectionist, it could undermine multilateral cooperation, especially with developing countries that emphasise equity and differentiated responsibilities. Future CBAM reform — covering scope, the treatment of export rebates, and alignment with WTO rules — will determine how strongly CBAM incentivises foreign jurisdictions to adopt carbon pricing, whether it mitigates or exacerbates concerns about fairness and unequal historical responsibility and how stable the mechanism will be in the face of trade disputes.

Ambec, S., F. Esposito, and A. Pacelli (2024), “The Economics of Carbon Leakage Mitigation Policies”. Journal of Environmental Economics and Management, vol. 125.

Beaufils, T., H. Ward, M. Jakob, and L. Wenz (2023), “Assessing Different European Carbon Border Adjustment Mechanism Implementations and Their Impact on Trade Partners”. Communications Earth & Environment, 4(131).

Bellora, C. and L. Fontagné (2023), “EU in search of a Carbon Border Adjustment Mechanism”. Energy Economics, vol 123.

Carbone, J. C., and N. Rivers (2017), “The Impacts of Unilateral Climate Policy on Competitiveness: Evidence from Computable General Equilibrium Models”. Review of Environmental Economics and Policy 11, no. 1: 24-42.

Clausing, K. A., and C. Wolfram (2023), “Carbon Border Adjustments, Climate Clubs, and Subsidy Races When Climate Policies Vary”. Journal of Economic Perspectives, 37(3): 137-62.

Dechezleprêtre, A., A. Haramboure, C. Kögel, G. Lalanne, and N. Yamano (2025), “Carbon Border Adjustments: The potential effects of the EU CBAM along the supply chain”. OECD Science, Technology and Industry Working Papers No. 2025/02.

Dolphin, G., and G. Ferrucci (2026), “The EU’s CBAM: implications for member states and trading partners”. ECB Working Paper No. 3177.

Fontagné, L., and K. Schubert (2023), “The Economics of Border Carbon Adjustment: Rationale and Impacts of Compensating for Carbon at the Border”. Annual Review of Economics, Vol. 15, September, pp. 389-424.

Overland, I., and R. Sabyrbekov (2022), “Know your Opponent: Which Countries Might Fight the European Carbon Border Adjustment Mechanism?”. Energy Policy, Vol 169, October.