This policy brief is based on Franconi and Hack (2026): “Import Tariffs and the Systematic Response of Monetary Policy“. The views expressed in this brief are those of the authors and do not necessarily reflect the views of the Banque de France or the Eurosystem.

Abstract

Import tariffs have returned to the center of economic policy, raising two key questions. First, what are the macroeconomic effects of tariffs? Second, how should central banks respond? In Franconi and Hack (2026), we show that U.S. tariffs reduce output and raise consumer prices, confirming that tariffs act as adverse supply shocks. The Federal Reserve responds by lowering interest rates to cushion the output decline. To understand the effects of alternative policy scenarios, we present several monetary policy counterfactuals that help to quantify the policy tradeoff due to tariffs. Strict inflation stabilization deepens the output contraction by 36%, while output stabilization nearly doubles peak inflation. The results also challenge common justifications for tariffs: trade balance improvements are at best transitory, and the net fiscal revenue effect tends to be negative.

Tariffs are back. Most notably, in April 2025, the Trump Administration implemented the most sweeping increase in U.S. import duties in nearly a century, declaring the trade deficit a national emergency (The White House, 2025). Yet, despite the prominence of tariffs in today’s policy landscape, there is little direct empirical evidence on their macroeconomic effects. Obtaining empirical evidence is particularly relevant because theoretical predictions deliver different implications, depending on model assumptions. For example, tariffs can be expansionary or contractionary, leaving open whether they act as supply shocks, demand shocks, or something in between (e.g., Auclert, Rognlie, and Straub, 2025).

Understanding the nature of tariff shocks is particularly important for monetary policy. When prices and output move in the same direction, as under a demand shock, stabilizing one automatically helps stabilize the other. But if tariffs behave like supply shocks, monetary policy faces an unpleasant tradeoff: tightening to contain inflation amplifies the recessionary impact, while easing to support real activity fuels further price increases.

Such considerations are of high practical relevance. For example, as Fed Chair Jerome Powell noted at the IMF’s Polak Conference in November 2023, the standard rationale for attenuating the monetary response to supply-driven price increases is that tightening would otherwise amplify the decline in employment that the shock already causes (Powell, 2023). But for how long should central banks look through supply shocks and tolerate elevated inflation? How much inflation must be tolerated to cushion the recessionary impact? And, conversely, if central banks start to fight inflationary pressure with higher interest rates, what are the associated output and employment consequences?

To answer these questions, in Franconi and Hack (2026), we use vector-autoregression models and U.S. time series data between 1990 and 2024. We establish that tariff shocks are both contractionary and inflationary, confirming that tariffs act as adverse supply shocks that imply a meaningful monetary policy tradeoff. To quantify this tradeoff, we construct monetary policy counterfactuals without relying on a microfounded structural model. Instead, we follow McKay and Wolf (2023) and use empirically identified monetary policy shocks to build counterfactuals that are robust to model misspecification and the Lucas critique.

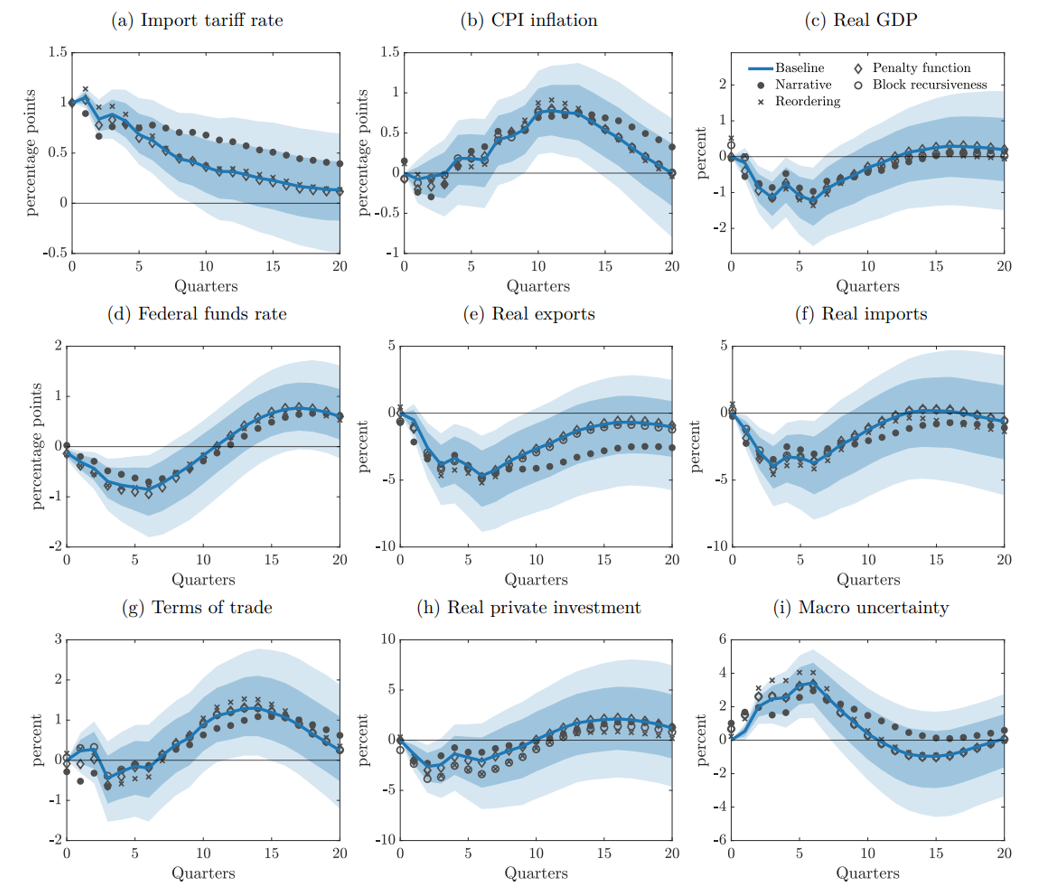

A 1 percentage point increase in the trade-weighted U.S. import tariff rate — defined as customs duties divided by dutiable imports — lowers real GDP by 1.23% at the trough, reached after six quarters. Consumer price inflation responds with a delay of about one year but then rises continuously, peaking at 0.78 percentage points after eleven quarters. The inflation effect is persistent and significant for over four years.

The Federal Reserve has historically responded to tariff shocks by easing policy. The federal funds rate falls by 0.85 percentage points at its trough, also reached after six quarters. This accommodation cushions the decline in output but contributes to inflationary pressure. Interestingly, the partial monetary accommodation is consistent with theoretical prescriptions for the optimal monetary response to tariff shocks (Bergin and Corsetti, 2023; Bianchi and Coulibaly, 2025; Monacelli, 2025; Werning, Lorenzoni, and Guerrieri, 2025).

Beyond the core macroeconomic variables, the tariff shock reduces real investment, increases macroeconomic uncertainty, and lowers both real imports and real exports. The terms of trade improve, though with a delay. These patterns are consistent with tariffs acting as adverse supply shocks.

Figure 1. Responses to the import tariff rate shock

Note: This figure shows the macroeconomic responses to the import tariff shock. The solid blue line represents the posterior median, and the shaded areas are 68% and 90% credible sets. The baseline estimates impose the identifying restriction that the shock affects only the import tariff rate and the federal funds rate contemporaneously. The gray markers show the posterior medians using alternative identification approaches that relax the baseline assumptions. Reordering: We relax each zero restriction individually by reordering the VAR vector. Block recursiveness: we jointly relax the zero restrictions for all “fast moving” variables, which are macro uncertainty, terms of trade, and CPI inflation. Penalty function: we identify the tariff shock by maximizing the impact on the tariff rate for the first four quarters after the shock. Narrative: We compile a time series that captures changes in tariffs due to narratively identified tariff policy changes, include this series as an additional exogenous variable to the VAR, and present responses to a shock to this series.

To obtain these effects, we need to confront the following identification challenge: even if tariff policy is plausibly exogenous to current macroeconomic conditions, innovations to the trade-weighted average tariff rate are not necessarily exogenous. The reason is that the trade weights depend on import composition and prices, which may also respond to other macroeconomic shocks. In Franconi and Hack (2026), we address this identification challenge by employing several distinct identification approaches, including short-run timing restrictions, a penalty function approach, and a narrative approach that focuses on tariff changes primarily due to policy events. Across all identification approaches, we obtain similar results, underscoring the robustness of our findings.

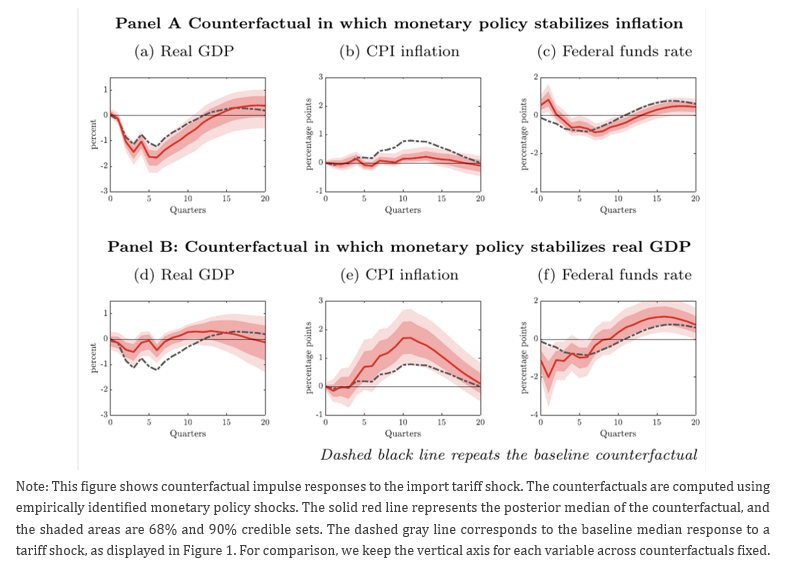

The finding of partial monetary accommodation raises an immediate policy question: what would happen under alternative central bank responses? To answer these questions, we construct counterfactual scenarios using the method of McKay and Wolf (2023), leveraging empirically identified monetary policy shocks. A key advantage of this approach is that the resulting counterfactuals are valid in a broad class of macroeconomic models — including conventional New Keynesian frameworks — and are robust to the Lucas critique.

In the first counterfactual, monetary policy aims to strictly stabilize consumer prices. Instead of partial accommodation, the central bank raises the federal funds rate sharply — by 0.82 percentage points — in the quarter after the tariff shock. This short-lived tightening is effective: peak inflation drops from 0.78 to just 0.21 percentage points, strongly dampening the inflationary impact. But the cost is substantial. The output contraction deepens by 0.44 percentage points at the trough — a 36% increase relative to the baseline. The adverse output effects are also more persistent, taking 16 quarters to return to the baseline path.

In the second counterfactual, monetary policy targets strict output stabilization while ignoring inflation. The federal funds rate falls by 2.0 percentage points at its trough — more than twice the baseline easing. This aggressive cut substantially dampens the output decline but does not fully eliminate it.1 The inflation cost, however, is high: the peak inflation effect nearly doubles, rising by 0.93 percentage points above the baseline. Since full output stabilization would likely require even more aggressive easing, this inflation amplification represents a lower bound for the true cost of fully offsetting the output decline.

Figure 2. Responses under counterfactual monetary policy

These counterfactuals are obtained using the high-frequency identified shock from Miranda-Agrippino and Ricco (2021) and the Taylor rule residual from Romer and Romer (2004). Importantly, the results are similar when using alternative shock measures, including one that accounts for time variation in systematic monetary policy from Hack, Istrefi, and Meier (2024), and a shock identified based on heteroskedasticity from Jarocinski (2024).

A common argument for tariffs is that they generate government revenues and protect domestic producers from foreign competition, which may shrink the trade deficit. The Trump Administration has prominently advanced both claims — framing the trade deficit as a national emergency and promising that tariff revenues would contribute to deficit reduction and potentially substitute for income taxes (NPR, 2025). Our evidence casts doubt on each of these claims.

Studying the trade balance response to tariffs, we find that any improvement is, at best, highly transitory. Focusing on the government revenue side, the picture is equally unfavorable. While tariff shocks do generate customs revenues, we find that government receipts from other sources decline, likely because of the recessionary effects of tariffs. Overall, the latter effect tends to dominate because government debt rises over the medium term in response to a tariff shock. Put differently, tariffs raise revenue from customs duties but lose more than they gain by shrinking the economy.

Three conclusions stand out.

First, tariffs are supply shocks. They simultaneously raise prices and reduce output, creating a genuine tradeoff for monetary policy. The partial accommodation observed historically — where the central bank cuts rates to cushion the recessionary impact while tolerating some inflation — is a reasonable response and aligns with theoretical prescriptions for optimal policy.

Second, tariffs do not deliver on two of their most commonly cited benefits. The trade balance does not meaningfully improve, and the net fiscal effect tends to be negative. While customs duties rise, the contractionary consequences of tariffs erode the broader tax base by more than enough to offset the tariff revenue, resulting in higher public debt.

Third, the monetary policy tradeoff is quantitatively large. Fully stabilizing prices after a tariff shock requires a sharp — albeit temporary — interest rate increase that deepens the output contraction by more than a third. Conversely, attempting to stabilize output requires more aggressive rate cuts, causing the peak inflation response to be twice as large.

Auclert, A., M. Rognlie, and L. Straub (2025): “The Macroeconomics of Tariff Shocks,” Working Paper 33726, National Bureau of Economic Research.

Bergin, P. and G. Corsetti (2023): “The Macroeconomic Stabilization of Tariff Shocks: What is the Optimal Monetary Response?” Journal of International Economics, 143, 103758.

Bianchi, J. and L. Coulibaly (2025): “The Optimal Monetary Policy Response to Tariffs,” Working Paper 33560, National Bureau of Economic Research.

Franconi, A. and L. Hack (2026): “Import Tariffs and the Systematic Response of Monetary Policy,” Banque de France Working Paper No. 1035.

Hack, L., K. Istrefi, and M. Meier (2024): “The Systematic Origins of Monetary Policy Shocks,” CEPR Discussion Paper 19063.

Jarociński, M. (2024): “Estimating the Fed’s Unconventional Policy Shocks,” Journal of Monetary Economics, 144, 103548.

McKay, A. and C. K. Wolf (2023): “What Can Time-Series Regressions Tell Us About Policy Counterfactuals?” Econometrica, 91, 1695–1725.

Miranda-Agrippino, S. and G. Ricco (2021): “The Transmission of Monetary Policy Shocks,” American Economic Journal: Macroeconomics, 13, 74–107.

Monacelli, T. (2025): “Tariffs and Monetary Policy,” CEPR Discussion Paper 20142.

NPR (2025): “Trump announces reciprocal tariffs on dozens of nations and sweeping 10% tariff,” April 2, 2025.

Powell, J. (2023): Opening remarks at “Monetary Policy Challenges in a Global Economy,” 24th Jacques Polak Annual Research Conference, International Monetary Fund, Washington, D.C., November 9, 2023.

Romer, C. and D. Romer (2004): “A New Measure of Monetary Shocks: Derivation and Implications,” American Economic Review, 94, 1055–1084.

The White House (2025): “Regulating Imports With a Reciprocal Tariff to Rectify Trade Practices That Contribute to Large and Persistent Annual United States Goods Trade Deficits,” Executive Order of the U.S. President Donald Trump from April 2, 2025.

Werning, I., G. Lorenzoni, and V. Guerrieri (2025): “Tariffs as Cost-Push Shocks: Implications for Optimal Monetary Policy,” Working Paper 33772, National Bureau of Economic Research.

Exact stabilization of any single variable would require infinitely many distinct monetary policy shocks. The counterfactual method uses two identified shocks, which achieve approximate but not perfect stabilization. See McKay and Wolf (2023) for a formal discussion.