Opinions expressed by the authors do not necessarily reflect the viewpoint of the Oesterreichische Nationalbank or the Eurosystem.

Abstract

The tariffs imposed and postponed by the Trump administration so far seem erratic and not well thought-through. But a paper published by Stephen Miran already before Trump’s second inauguration makes a case for tariffs as an instrument to balance the overvaluation of the US-Dollar and hence to make US goods more competitive in foreign markets. He pleads for international cooperation to correct exchange rates in a so called “Mar-a-Lago Accord”. We discuss the pros and cons of his proposal and question the logic of current policy implementation. Past examples of successfully coordinated exchange rate realignments relied on trust among participants and mutually shared policy goals, not on threats and escalating tactics.

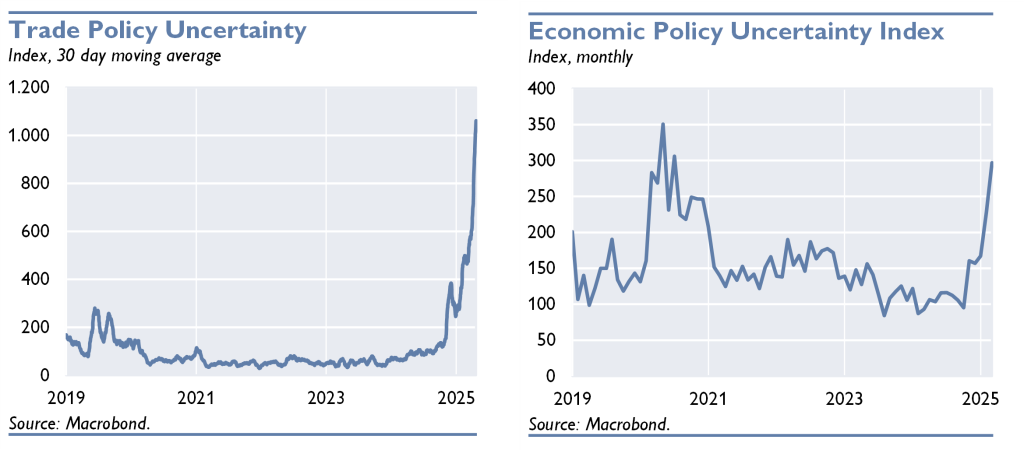

The USA is imposing tariffs and delaying them. In January, President Trump announced punitive tariffs on imports from Canada and Mexico, only to suspend them a few days later; the economic consequences of these tariffs have been analyzed by De Luigi et al. (2025). At the end of March, the next escalation followed: From April, imports of cars and car parts as well as aluminum and steel are subject to a 25 percent tariff. Trump announced so called “reciprocal” tariffs on April 2 on most countries, only to pause them one week later while maintaining a tariff floor of 10% for everybody (except for China that will face a tariff of at least 145%).

These erratic announcements may seem purely arbitrary, yet they have far-reaching consequences: According to the Economic Policy Uncertainty Index, economic uncertainty in the world today is higher than during the peak of the pandemic or the financial crisis.

There are indications that this economic policy is not (exclusively) a product of chance. Stephen Miran, a member of the Council of Economic Advisers, detailed his strategy for a new global economic order as early as November 2024. In his much-discussed essay “A User’s Guide to Restructuring the Global Trading System,” Miran outlines a concept that understands tariffs as a central instrument to foster the industrial competitiveness of the USA. In this essay, he recommends the use of tariffs to correct structural imbalances in American foreign trade with the long-term goal of reindustrializing the USA. Miran’s statements have also been discussed in the media, for example by Gillian Tett and Martin Wolf in the Financial Times, while economists Brad DeLong and Paul Krugman consider his plans misguided and their media reception largely as “sanewashing.”

At the center of Miran’s analysis is a well-known problem of economic policy: the Triffin dilemma. Due to the role of the US dollar as a global reserve currency, the USA benefits from an exorbitant privilege in international financial systems – for example, by being able to sanction other countries or by enjoying lower financing costs of their national debt.

However, the permanent demand for dollars for reserve holdings also leads to persistent current account deficits in the USA (3.9% of GDP in 2024). The high demand for dollars causes a overvaluation of the currency. In this context, the idea of creating a strategic Bitcoin reserve by the US government seems reasonable: if Bitcoin would substitute the dollar partially as reserve asset, the dollar exchange rate could decline.

For Miran the sustained overvaluation is the main cause of the deindustrialization of the USA in recent decades. The fact that industrial employment has declined in other countries like the United Kingdom to a similar extent as in the USA, although their currency does not serve as global reserve asset, sheds some doubt on this account. Deindustrialization made the US strategically vulnerable according to Miran, especially regarding China and security-relevant supply chains, and it impoverished formerly prosperous US regions. The loss of well-paid industrial jobs particularly affected the population in the rust belt of the USA, which might have caused some former Democratic strongholds there to increasingly vote for Republicans in recent years.

Against this background, Miran proposes an aggressive tariff policy – not as a protectionist measure in the traditional sense, but as a strategic move to bring the global economic system back into balance. His main points are:

Miran explicitly refers to the first Trump administration: despite higher tariffs, the dollar fell, and inflation remained low. The US Treasury received billions in additional revenue through tariffs – according to Miran, financed by the exporting countries subject to tariffs. However, not many economists share this view; some empirical studies explicitly find that US consumers bore the burden of tariffs, see for example Amiti et al. (2019) or Fajgelbaum and Khandelwal (2021).

A significant factor that could reduce the inflationary effect of tariffs is their circumvention, as Miran himself points out. If a country subject to a US tariff exports its goods to a tariff-free third country and they are then sold from there to the USA, no tariff is paid. Thus, the USA does not generate revenue and the desired steering effect of imported goods to domestically produced ones also fails. Raising tariffs on almost all countries as it was announced on April 2 would reduce that loophole.

In Miran’s plans, no nation subject to a US tariff takes countermeasures like imposing tariffs on American imports. In fact, with all the fog created by the reciprocal tariffs, the EU decided almost unnoticed to suspend countermeasures for 90 days that were originally intended to counter the tariffs on aluminum and steel. However, these later measures remain in place and most countries did not react to the still remaining 10 % tariffs thus far. However, this may not be the final state and the escalating trade war with China (PIIE, 2025) demonstrates the precariousness of this assumption.

For a successful reindustrialization of the USA, long-term investments by the corporate sector over many years would be necessary to augment the productive capacities of the US. Erratic changes in trade and economic policies that have characterized Trump’s previous administration (and his current term so far) are not conducive to promoting such investments. Miran suggested in his essay that “policy will proceed in a gradual way that attempts to minimize any unwanted market consequences” which is not how it played out. It is also questionable whether the overvaluation of the dollar was the most important reason for the relocation of industrial production from the USA to other countries.

Miran also proposes an ambitious and complex currency adjustment, modeled after the Plaza Accord of 1985. The goal of this coordinated adjustment, as it was back then, would be a controlled devaluation of the US dollar to strengthen the international competitiveness of the US economy. However, the countries involved in the Plaza Accord, which held the majority of dollar reserves back in the day, were close political allies of the USA. Almost all had supported the NATO Double-Track Decision, some of them even against considerable public resistance in their own electorates. Today, the countries that hold most dollar reserves have less close political relations with the USA: Miran estimates that China holds ten times as many and India still twice as many dollar reserves as the Eurozone. Whether the required degree of cooperation for the proposed coordination can be found today seems unlikely because the geopolitical situation has changed significantly.

Given the most recent events, it also seems not very realistic that a sufficiently large number of countries could be forced to cooperate by threats. Currency arrangements and trade relations are based on closely knit international networks. Serious disruptions of these networks can be detrimental for all participants and, given the high degree of complexity, escalatory policies might easily run out of control. In the field of geopolitics, a risk-accelerating strategy is referred to as brinkmanship, but Thomas Schelling cautioned that failure is highly probable due to many unknowns and unknowables. Nevertheless, Miran assumes that the major trading partners will cooperate, and he calls their hypothetical future agreement the “Mar-a-Lago Accord” after Trump’s holiday resort in Florida.

Without cooperation from other states, the USA could also devalue its currency by purchasing foreign currency reserves via a yet-to-be-established sovereign wealth fund or by levying fees on US treasury bonds from foreign buyers based on executive orders, making them less attractive. Miran is aware that lower demand for US treasury bonds will also lead to rising interest rates but hopes to mitigate this effect through closer cooperation between the US Treasury and the Federal Reserve. Despite these attempts to make the dollar less attractive as a reserve currency, its role as a unit of account in international trade should remain untouched.

In his essay, Miran provides a provocative alternative to the existing financial order. Nevertheless, essential questions remain open. If the goal of the tariff policy is a weaker dollar, a devaluation of other currencies would be counterproductive; however, this devaluation is assumed to avoid the inflationary effects of tariffs. The existing supply chains of the US industry often operate cross-border, with many suppliers of the American auto industry located in Canada and Mexico. Tariffs make their inputs more expensive, thus also inflating the prices of American production.

Miran understands that other countries may respond to American tariffs with countermeasures but considers the risk of significant reactions to be low. He seems to assume that threats from the USA to withdraw their security guarantees are sufficient to impose the USA’s trade policy will on many countries. However, this fundamental attitude of the current US administration threatens to destabilize the world order that the US has so far dominated as a hegemon. If countries that have been closely allied with the US so far are expected to pay a higher price for this alliance in the future they might reconsider and use these funds instead to prop up their own defense. One of the reasons for relying on the protection of a superpower is its reliability. If the reliability of the US is in dispute, the whole security architecture becomes questionable.

The quite erratic mix of announcements of tariffs and their postponement or suspension corresponds to a transactional understanding of politics that judges the international security or financial architecture solely based on the profits that are reaped by the US. Threats of high tariffs or the annexation of foreign territory are, in this sense, only negotiating positions that can be arbitrarily built up or abandoned. This approach is referred to as “escalate to de-escalate,” a term that US Treasury Secretary Bessent used last year in relation to Trump’s trade policy. The fact that these policy changes destroy a lot of trust, which is a crucial prerequisite for international cooperation, is not taken into account.

Although Miran recognizes that these policies contain many risks, he considers them calculable. His proposal aims to readjust the American position in an overstretched system – not by retreat, but by actively redistributing the subjectively perceived burdens. Whether his proposals will be fully implemented remains open – but they provide insights into the economic beliefs of Donald Trump’s second presidency. The debate about tariffs, reserve currency status, and currency coordination will not disappear – on the contrary, it could shape the coming years.

Mary Amiti, Stephen J. Redding and David E. Weinstein (2019) The Impact of the 2018 Tariffs on Prices and Welfare. Journal of Economic Perspectives 33 (4): 187–210.

Anne Case and Angus Deaton (2020) Deaths of Despair and the Future of Capitalism. Princeton University Press.

Clara De Luigi, Wolfgang Lechthaler and Fabio Rumler (2025) The Economic Fallout of Trump’s Tariff Policies: Impacts on the US and Euro Area. SUERF Policy Brief No 1091.

Pablo Fajgelbaum and Amit Khandelwal (2021) The Economic Impacts of the US-China Trade War. NBER Working Paper No. 29315.

Harold James (1996) International Monetary Cooperation Since Bretton Woods. Oxford University Press.

Ivo Maes (2021) Robert Triffin: A Life. Oxford Studies in the History of Economics.

Peterson Institute for International Economics (2025). US-China Trade War Tariffs: An Up-to-Date Chart. (link)

Thomas Schelling (1980) The Strategy of Conflict. Harvard University Press.