This policy brief is based on Banco de España, Series: Working Papers. 2605. The views expressed are those of the authors and not necessarily those of the institutions the authors are affiliated with.

Abstract

We examine how monetary policy shocks transmit to private equity activity, focusing on deal volumes, leverage, and pricing. Using a large dataset of approximately 55,000 transactions (2000–2020) and high-frequency identification of policy surprises, we find that policy tightening at the short end of the yield curve reduces deal volumes, lowers the likelihood of leveraged buyouts, and compresses valuation multiples. Valuation effects are non-linear, being stronger among high-multiple deals, indicating greater sensitivity to discount-rate changes. Shocks to long-term yields have weaker effects—some influence on volumes, little on pricing—consistent with the short-tenor, floating-rate financing of buyouts, and the all-equity nature of minority acquisitions, such a venture and growth capital investment. The results underscore the role of monetary policy in shaping private equity cycles at the margin.

Private equity has moved from a niche corner of finance to an important driver of corporate funding, restructuring, and innovation. Over the last two decades, dedicated funds have financed everything from early-stage ventures to ambitious buyouts of large, established companies. As this private market ecosystem has grown, so too has the importance of understanding how macroeconomic forces—especially monetary policy—shape it. In a recent working paper (Avalos et al, 2026), we explore a simple but consequential question: how does monetary policy actions affect private equity activity? The answer turns out to involve two straightforward but powerful channels—credit conditions and valuation—whose relative influence depends on whether we are looking at how many deals get done, how much debt those deals use, or how much buyers pay for targets.

What follows is a non-technical account of the study’s aims, methods, and findings, and why they matter policymakers.

Private equity funds—leveraged buyouts (LBOs), growth equity, and venture capital—have become major providers of risk capital. They are backed by institutional investors with long horizons and typically raise capital through closed-end structures that protect them from day-to-day redemption pressures. These features let private equity managers (often called general partners, or GPs) take on illiquidity and complexity in exchange for the potential to create value through operational improvements, strategic repositioning, and growth.

But private equity is not insulated from macro-financial conditions. Financing costs and public market’s appetite for risk shape both the feasibility and attractiveness of deals. A large buyout typically uses a combination of equity from the fund and debt (often floating-rate loans syndicated by banks). Even venture and growth investments—while usually all-equity at entry—are ultimately valued against discount rates that reflect risk-free rates and risk premia. In short, when policy rates move unexpectedly, the economics of private equity transactions can shift rapidly.

From a policy perspective, this matters because private equity influences corporate leverage and ownership patterns. A tightening cycle that discourages buyouts can slow the pace of restructuring and change how companies finance themselves. An easing cycle can do the opposite. Understanding these dynamics complements the broader literature on the “non-bank channel” of monetary policy, which has mostly focused on non-bank credit (e.g., direct lenders, bond funds) rather than equity acquisitions.

The analysis focuses on three segments of private equity activity:

These segments differ in their reliance on debt at entry, but they share an underlying logic: the acquisition of firms with the purpose of improving their future cash flows and profitability, under new ownership, governance, and strategic plans. That logic ties them directly to discount rates and financing conditions, which monetary policy helps shape.

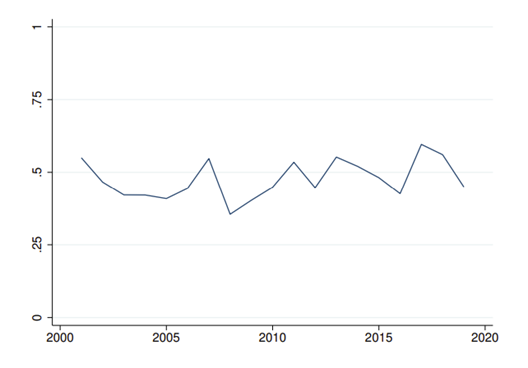

Private equity deal volumes have grown markedly since the early 2000s, interrupted by the global financial crisis and the early pandemic shock (see Figure 1), and then rebounding strongly in 2021. The long-term trend reflects rising institutional allocations to private markets and the maturation of the asset class.

Figure 1. Volume of private equity deals

For buyouts, the mix of debt and equity used at entry during this period has been relatively stable in aggregate over time at about 50% of deal value (see Figure 2). That stability masks significant deal-by-deal differences, but it suggests that the availability and price of credit mainly determine which deals close at a given leverage.

Figure 2. Share of debt in LBOs, as percent of deal value

To understand how policy surprises show up in private equity outcomes, the paper frames the analysis around two intuitive channels.

First, a credit channel. Monetary policy affects short-term risk-free rates and, through them, the cost of floating rate borrowing and risk appetite in credit markets. Tighter policy makes debt financing scarcer and more expensive, discouraging transactions that rely on leverage; looser policy does the opposite.

Second, a valuation channel. Policy affects the risk-free component of discount rates. In addition, investors’ required compensation for bearing equity risk—the equity risk premium—fluctuates with the macro-financial backdrop. Higher discount rates and higher equity risk premia lower the present value of future cash flows and reduce what buyers are willing to pay for a company’s future earnings today.

The first channel is especially salient for LBOs, which rely on debt at entry. The second channel matters for any deal where the value hinges on expected performance improvements and growth under private ownership—arguably the whole spectrum of private equity.

The study assembles a large dataset of private equity transactions from 2000 to early 2020 (around 55,000 deals, largely concentrated in the United States, though global in coverage). For each deal, it records:

The analysis links those deals to three macro-financial variables:

Three outcomes anchor the empirical work:

The goal is not to estimate a structural model but to identify directional, economically meaningful relationships that map cleanly onto the credit and valuation channels.

When short-term yields rise unexpectedly around policy announcements, the total dollar amount of closed PE transactions falls. This is a robust finding: it holds even when controlling for credit spreads and the equity risk premium.

The intuition is straightforward. PE funds operate under investment periods with committed capital, but the pace and feasibility of closing deals depend on the financing environment. When short-term funding costs jump, debt-supported deals become harder to pencil out or riskier to syndicate. Even for equity-only investments, higher discount rates lower valuations and make sellers less willing to transact at prices buyers can justify.

Credit spreads also help explain volumes. Wider spreads—independent of policy—signal tighter credit and lower risk appetite. In those moments, there are fewer opportunities to close deals at an acceptable price and risk level. By contrast, the equity risk premium has a more limited direct effect on aggregate volumes once policy and credit conditions are included, though it remains directionally consistent with the idea that lower premia encourage more activity.

The probability that a given private equity transaction is a leveraged buyout rather than a non-LBO declines after tightening surprises. In other words, when policy hikes short rates, the mix of PE transactions shifts away from debt-reliant acquisitions.

This result is consistent with how LBOs are structured: floating-rate loans, syndicated by banks, typically reference short-term benchmarks and reprice quickly. Equity-only venture and growth deals are less immediately exposed (at entry) to the price of debt, though they remain sensitive to the broader valuation channel.

Credit spreads again matter. Wider spreads make debt-funded deals less attractive or even infeasible, reducing the share of LBOs in the mix. By contrast, the equity risk premium plays a smaller role in explaining whether a deal is an LBO—its marginal effect on the LBO share is limited once policy and credit spreads are accounted for. That fits the idea that leverage decisions are mainly about credit availability and cost.

The price paid for targets, measured as the deal value-to-EBITDA multiple, declines after tightening surprises. This is a clean valuation story: higher discount rates lower the present value of expected improvements and cash flows under private ownership. The equity risk premium also matters a great deal for pricing: when it rises (i.e., investors require more compensation for equity risk), multiples fall, even after controlling for policy surprises. Once both policy and the equity risk premium are considered, credit spreads add little explanatory power to pricing.

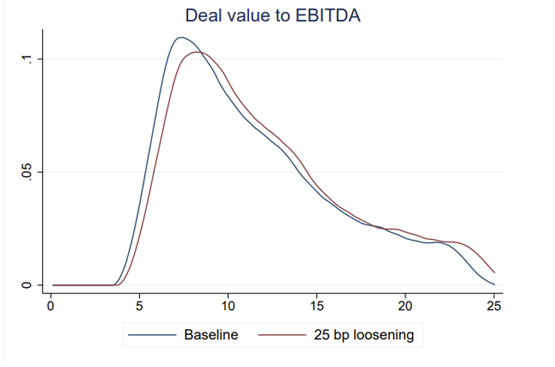

A notable nuance emerges when looking across the valuation distribution, presenting evidence of non-linearity on policy impact. The reduction in multiples is larger for deals at the high end—those commanding the greatest earnings multiples. This is exactly what one would expect if high-multiple transactions embed more distant or uncertain cash flows (e.g., ambitious growth stories or deep restructurings): as discount rates move, their present value swings more. Cheaper deals—perhaps anchored by nearer-term cash flows—are less sensitive.

Figure 3 depicts graphically this result, presenting the distribution of deal multiples across all transactions. After a modest easing surprise of 25 basis points, the whole distribution shifts to the right (higher prices), but the right tail—representing pricier deals—shifts a bit more. The mirror image happens after tightening.

Figure 3. Impact of 25 bps monetary policy easing

Policy surprises that move long-term yields—such as those related to central bank asset purchases or balance-sheet guidance—have a weaker effect on private equity:

On volumes, the long-end signal is noisier and generally less influential than short-end surprises, though there is still some evidence of a credit channel effect in certain specifications.

On pricing, the long-end surprises do not have a statistically or economically meaningful impact once short-end conditions and equity premia are considered.

This pattern aligns with financing structures. LBO debt is typically floating-rate and tied to short-term benchmarks, with maturities and repricing dynamics that make them sensitive to short-end policy. Even equity-only deals are valued in environments where the marginal cost of capital and near-term discount rates (proxied by shorter tenors) loom large. In that sense, conventional monetary policy—moving short rates and shaping expectations over the next few years—does most of the work in this segment.

Earlier studies offer two complementary insights. One strand shows that credit conditions, as captured by market-wide credit spreads, influence leverage and pricing in buyouts: cheap credit enables more debt and supports higher prices (Axelson et al, 2012). Another strand shows that equity risk premia shape private equity activity by changing the relative attractiveness of illiquid private investments versus public markets (Haddad et al, 2015).

Our paper integrates both strands under a monetary policy lens, offering additional nuances to previous findings. Credit conditions matter for how many deals close and how much leverage is used, and equity risk premia matter for how deals are priced. At the same time, it adds that unexpected shifts in short-end policy rates intensify both patterns: they curb volumes and leverage via the credit channel and depress pricing via the valuation channel.

Private equity’s rise has intertwined it with macro-financial conditions in ways that are increasingly important to understand. This study shows that the familiar levers of monetary policy—especially those that influence short-term rates—reach into private markets through intuitive pathways. Credit conditions govern how many deals and how much leverage; valuation conditions govern how much is paid. Both respond to policy surprises in meaningful, predictable ways.

When central banks tighten at the short end of the yield curve, floating-rate borrowing becomes more expensive, risk appetite in credit markets cools, and discount rates rise. The immediate consequences for private equity are fewer deals closing, a smaller share of transactions taking the form of leveraged buyouts, and lower prices paid per unit of current earnings—especially at the high end of the valuation spectrum.

Shocks that primarily move long-dated yields—absent big changes in short rates—are less consequential for private equity, consistent with the sector’s funding structures and the horizon at which discount rates are most salient for underwriting.

In practice, that means the private equity cycle is not just a story of dry powder, fundraising, or sector opportunities. It is also a story of the price of credit and the price of risk—two cores of monetary policy—translating into who buys what, at what price, and with how much debt. As private markets continue to expand and diversify, that translation will remain central to both investment decisions and policy assessment.

Axelson, U, T Jenkinson, P Stroemberg and M Weisbach (2013): “Borrow cheap, buy high? The determinants of leverage and pricing in buyouts”, Journal of Finance, vol 68, pp. 2223-67.

Avalos, F, B Hofmann, J M Serena (2026): “Monetary policy and private equity acquisitions: tracing the links”, BIS Working Papers, no 136, January.

Haddad, V, E Loualiche and M Plosser (2017): “Buyout activity: the impact of aggregate discount rates”, Journal of Finance, vol 72, pp. 371-414.