This policy brief is based on De Nederlandsche Bank Working Paper No.853. The views expressed are those of the authors and not necessarily those of the Bank of Canada, De Nederlandsche Bank and the Eurosystem.

Abstract

We examine the optimal coordination of conventional and unconventional monetary policy tools in an environment characterized by household heterogeneity and mortgage debt. We develop a dynamic stochastic general equilibrium (DSGE) model with three types of households – savers, borrowers, and renters – and incorporate housing investment, fixed-rate long-term mortgages, and a housing production sector. The central bank controls both the short-term interest rate and the long-term rate via the relative supply of long-term bonds. We show that household heterogeneity significantly alters the optimal policy response to macroeconomic shocks. In particular, following a cost-push shock, the optimal policy involves raising the short-term rate to combat inflation while lowering the long-term rate to alleviate financial burdens on indebted households and renters. This policy mix accelerates investment recovery but increases consumption inequality. In contrast, in a representative-agent economy, both rates are raised. Our findings highlight the importance of accounting for distributional effects in monetary policy design and suggest that yield curve control can be a valuable tool in heterogeneous economies.

Recent inflationary surges in major advanced economies, including the United States and the Euro Area, reignited debates on how central banks should balance conventional and unconventional monetary policy tools. During the latest inflationary episode, central banks first halted asset purchase programmes and then rapidly raised short‑term policy rates. This sequence produced a sharp rise in long‑term interest rates and mortgage rates, significantly increasing the financial strain on heavily indebted households. These developments pose a critical question: should short-term and long-term policy instruments always move in the same direction when addressing inflationary pressures?

We address the key question of the paper through the lens of a dynamic stochastic general equilibrium (DSGE) model that places household heterogeneity at its core. The model distinguishes between three types of households: savers (patient households), borrowers (impatient households with fixed-rate long-term mortgages), and renters (hand‑to‑mouth households). This structure allows the model to capture the uneven effects of monetary policy across households. The framework also incorporates a housing production sector and fixed‑rate long-term mortgages, making long‑term interest rates a crucial channel for borrowers and housing investment. Importantly, the central bank controls not only the short-term nominal interest rate but also influences long‑term rates by adjusting the relative supply of long-term government bonds—an unconventional instrument akin to yield curve control. This design allows for a coherent study of how conventional and unconventional tools interact in an economy with mortgage debt and household heterogeneity.

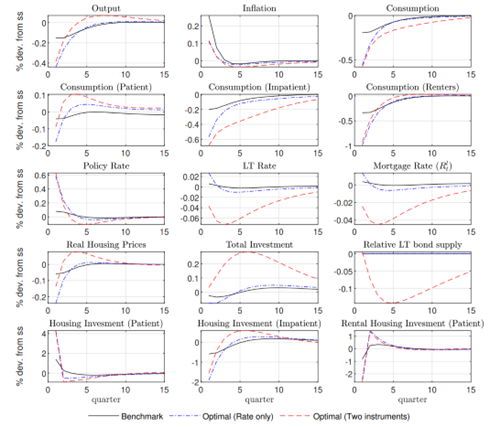

Figure 1 displays the impulse responses following an inflationary cost‑push shock. We focus on the case where the central bank sets optimally both the policy rate and the relative supply of long-term bonds (red dashed lines). We contrast this to two alternative cases, namely one (Benchmark with black solid lines) where the central bank sets the policy rate according to a Taylor rule while the relative long-term bond supply follows an exogenous process and another where only the policy rate is set optimally (blue-dashed lines). The optimal policy response with two instruments (red-dashed) involves raising the short‑term interest rate while simultaneously lowering the long‑term interest rate. Conventional policy tightening via higher short‑term rates is necessary to contain inflationary pressures. However, easing long‑term rates through unconventional policy mitigates the increased financial burden on indebted households and renters, who are most sensitive to mortgage and housing costs. In fact, impatient households’ housing investment recovers faster when both instruments are set optimally and overshoots more. This boosts total investment also allowing for a faster recovery of economic activity.

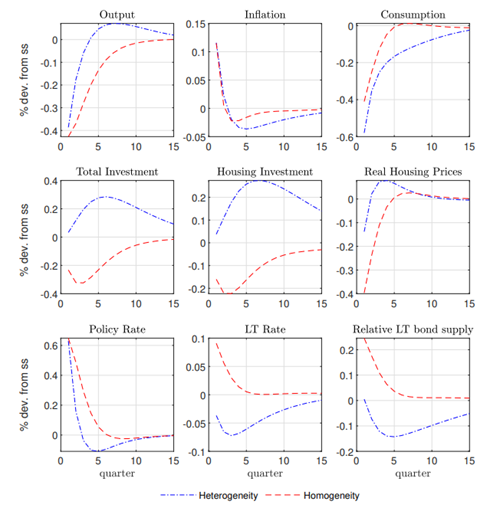

This result stands in sharp contrast to predictions from representative‑agent models (See Figure 2), where both short-term and long-term rates must be raised in response to inflationary shocks. In the absence of heterogeneity, long‑term financial conditions are assumed to affect all households similarly. But in a more realistic setting with mortgage debt, changes in long-term rates have pronounced distributional effects that alter the optimal policy strategy. We demonstrate that accounting for household-level differences leads to a policy prescription in which conventional and unconventional instruments may optimally be moved in opposite directions.

Figure 1. Impulse responses following a 1std cost-push shock

The model also highlights important distributional consequences. Impatient households raise their housing investment at the expense of their consumption for goods. At the same time the quick recovery of their investment in housing implies higher income for patient households from lending. This explains why their consumption (red dashed line) overshoots more relative to the other two cases. The optimal policy mix therefore increases consumption inequality. Nevertheless, the aggregate stabilisation benefits of this strategy outweigh its distributional drawbacks, especially in economies where mortgage debt is widespread. Policymakers should, however, remain aware of these distributional outcomes when deciding upon the monetary policy stance.

A significant implication of the paper relates to the value of yield curve control (YCC) or similar long-term asset purchase tools in heterogeneous economies. By directly influencing long‑term borrowing conditions, YCC allows the central bank to decouple its inflation‑fighting stance (implemented through short-term rate increases) from the financial pressures experienced by mortgage holders. The findings therefore support incorporating long-term rate management into the broader monetary policy toolkit.

Overall, the paper makes a strong case for rethinking the conventional assumption that policy instruments must move in the same direction. For central banks operating in economies with substantial mortgage debt and heterogeneous household balance sheets, the optimal policy mix is likely to involve a divergence between short-term and long-term rates. Short-term tightening combined with long-term easing can achieve inflation control while preventing excessive contraction in housing markets and avoiding disproportionate harm to financially vulnerable households. Neglecting such heterogeneity may lead to policy paths that are suboptimal or even counterproductive.

Figure 2. Impulse responses following a 1std cost-push shock; optimal policy using two instruments under homogeneity vs heterogeneity

We provide evidence that the design of monetary policy in mortgage-dependent economies may require a more nuanced mix of tools than traditionally assumed. By explicitly incorporating household heterogeneity, mortgage structures, and housing investment dynamics, policymakers can design strategies that better balance inflation stabilisation with financial resilience. Yield curve control emerges as a valuable instrument in this context, and its strategic use could enhance the effectiveness of monetary policy in future inflationary episodes.