The views expressed are those of the authors and not necessarily those of the Bank for International Settlements.

We document that the relationship between external financial openness and inequality varies considerably over time and across the main components of total external liabilities. In emerging market economies (EMEs), an increase in financial openness is typically associated with an initial rise and a subsequent fall in inequality. This suggests that the inequality-increasing channels tend to be active immediately, while the channels working in the opposite direction tend to operate with a lag. In advanced economies, the link between financial openness and inequality is much weaker than in EMEs.

Recent increases in inequality have prompted a lot of interest in its determinants. While existing research has identified international financial openness as one of the main potential drivers, the existing evidence is not conclusive. This is largely due to the use of different measures and methods across studies. Most papers have focused on legal restrictions on capital flows as a measure of openness (“de jure measures”). The few that have examined measures based on actual external financial positions (“de facto measures”) have used only a subset of the key metrics.

In a recent study, we conduct a comprehensive empirical examination of the link between inequality and external financial openness for a sample of 48 countries between 1991 and 2013 (Avdjiev and Spasova (2022)). In contrast to most existing research, we focus on de facto rather than de jure measures of financial openness. Furthermore, we examine not only gross external liabilities, but also their main components – foreign direct investment (FDI), portfolio equity, portfolio debt and other investment.

External financial openness can impact inequality through a number of channels.

FDI flows could lead to a rise in inequality through the skilled premium (SP) channel. An inflow of FDI into a given economy is typically associated with the introduction of new production technologies in that economy. Since such technologies are likely to increase capital intensity and the returns to skill, the benefits tend to accrue to higher-income individuals, who are likely to own more capital and to be more highly skilled than the rest of the population (Aghion and Howitt (1998) and Figini and Görg (2011)).

FDI flows could also lead to a fall in inequality through the technological diffusion (TD) channel. While this channel is generated by the same mechanism as the one driving the skilled premium channel, it typically takes longer to materialise and goes in the opposite direction. As the improved technology brought about by the influx of FDI spreads through the recipient economy in a diffusion-like learning process, the share of the population employed in the high-skilled industries increases (Aghion and Howitt (1998), Firebaugh and Goesling (2004), Hilbert (2014)). This ultimately results in a decline in inequality as the wage distribution starts to converge towards the new, higher-level equilibrium.

The skilled premium channel and the technological diffusion channel should be stronger for EMEs than for AEs, since the former tend to have lower initial technology levels and are, therefore, more likely to experience greater technological advances as a result of FDI inflows.

Greater external financial openness could lead to a fall in inequality through the funding conditions (FC) channel. International financial inflows into a given economy increase the availability of funding in that economy. This eases credit conditions, boosts consumption and investment, and ultimately increases employment. The resulting drop in unemployment should lead to a fall in inequality.

External financial openness could also decrease inequality via the access to credit (AC) channel. The easing of funding conditions generated by an increase in external financial inflows is likely to increase low-income individuals’ access to credit, which should, in turn, enhance their income generation opportunities (Beck et al. (2007)). This channel is likely to be more powerful in EMEs, where the share of the population with limited access to credit is larger than in AEs.

The foreign exchange rate (FX) channel could also lead to a negative relationship between external financial openness and inequality. External financial flows into a given country tend to lead to an appreciation of that country’s exchange rate. This tends to improve the creditworthiness of borrowers with currency mismatches on their balance sheets (Bruno and Shin (2015a), Bruno and Shin (2015b) and Hofmann et al. (2016)). In turn, this improves their access to credit, which, as discussed above, expands their income-generating opportunities.

External financial openness could increase inequality through the special interest group (SIG) channel. If the quality of institutions in a given country is low, special interest groups could capture the financial gains stemming from international financial openness (Claessens and Perotti (2007)). Since institutional quality is generally lower in EMEs than in AEs, the SIG channel should be more powerful in the former group of countries.

Portfolio equity flows could increase inequality through the capital gains (CG) channel. All else the same, an inflow of portfolio equity into a given country would increase equity prices in that country. Since equity holdings tend to be concentrated in wealthy individuals, the capital gains triggered by foreign flows would increase inequality.

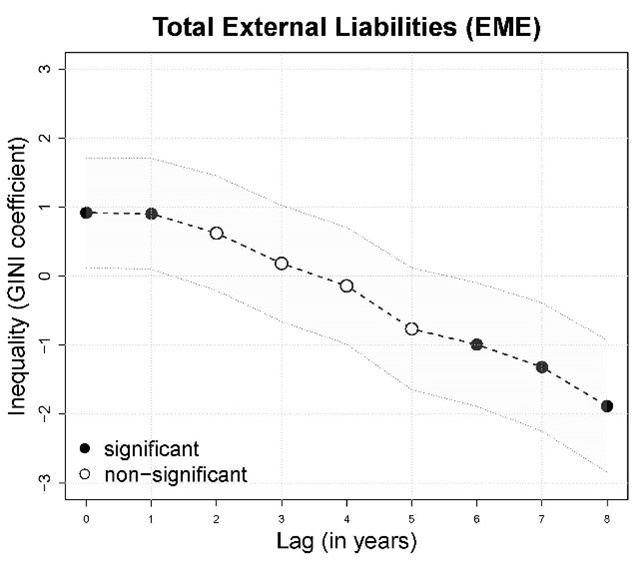

The impact of external financial openness on inequality in EMEs varies considerably over time (Figure 1, left-hand panel). An increase in a country’s external liabilities is associated with a rise in inequality in the year in which it occurs and in the subsequent year. The impact then becomes insignificant between the second and the fourth year after the increase in external liabilities. Finally, it turns negative and statistically significant from the sixth year onwards.

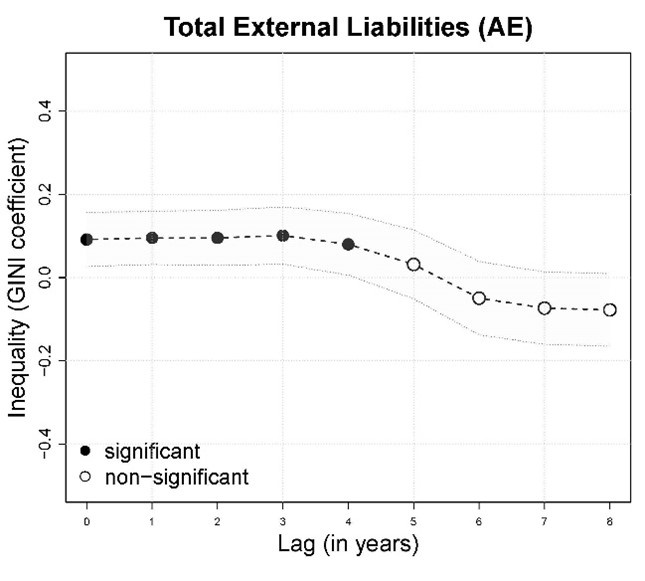

The relationship between financial openness and inequality tends to be considerably weaker in AEs than in EMEs (Figure 1, right-hand panel). An increase in external financial liabilities in AEs is associated with a statistically significant, but small increase in inequality. The relationship becomes insignificant after five years.

Figure 1: Aggregate financial openness and inequality

|

|

Note: Dots represent estimated coefficient. A filled dot denotes that the respective coefficient is statistically significant at the 10% level. Dotted lines represent 90% confidence bands.

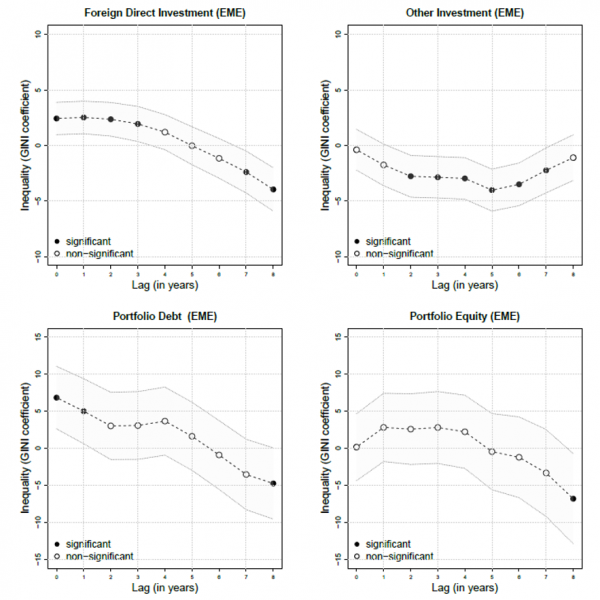

The above aggregate patterns conceal considerable heterogeneity among the main components of financial openness, especially in EMEs (Figure 2).

An increase in the FDI liability stock of an EME is associated with an initial increase and a subsequent decline in inequality. As predicted by the theoretical model of Aghion and Howitt (1998), the skilled premium (SP) channel begins to operate immediately. After several years, as the technological diffusion (TD) channel gathers momentum, its effects start to dominate, ultimately resulting in a decline in inequality.

While the overall dynamic patterns for portfolio debt (PD) are similar to those for FDI, there are important differences. Most notably, the initial increase and the subsequent decline in inequality associated with a PD increase are larger in magnitude than their FDI counterparts. Intuitively, the SIG channel (which leads to an increase in inequality) tends to operate immediately, while the FC channel (which leads to a decline in inequality) tends to work with a lag.

An increase in other investment liabilities tends to be associated with a statistically significant fall in inequality, albeit with a lag of a couple of years. The decline tends to be fairly persistent, lasting for seven years. Thus, the AC, FC and FX channels appear to dominate the SIG channel.

Finally, the relationship between portfolio equity (PE) and inequality tends to be insignificant. This implies that the CG and the SIG channels are largely offset by the AC and FX channels.

Figure 2: Component-specific financial openness and inequality (EMEs).

Note: Dots represent estimated coefficient. A filled dot denotes that the respective coefficient is statistically significant at the 10% level. Dotted lines represent 90% confidence bands.

In summary, we document that the relationship between external financial openness and inequality varies considerably not only over time, but also across the main components of total external liabilities. We also demonstrate that the relationship is considerably stronger in EMEs than in AEs, most likely due to the fact that the key channels through which external financial openness impacts inequality tend to be weaker in AEs than in EMEs. The key dynamic patterns that we document appear to be driven by the fact that the channels through which financial openness increases inequality tend to be active almost immediately, while the inequality-decreasing channels tend to operate with a lag.

Aghion, P. and Howitt, P. (1998). Endogenous Growth Theory. Cambridge, MA: MIT Press.

Avdjiev, S. and Spasova, T. (2022). Financial openness and inequality. BIS Working Papers, no 1010.

Beck, T., Demirgüç-Kunt, A., and Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27-49.

Bruno, V. and Shin, H. S. (2015a). Capital flows and the risk-taking channel of monetary policy. Journal of Monetary Economics, 71, 119-124.

Bruno, V. and Shin, H. S. (2015b). Cross-border banking and global liquidity. Review of Economic Studies, 82(2), 535-564.

Claessens, S. and Perotti, E. (2007). Finance and inequality: channels and evidence. Journal of Comparative Economics, 35(4), 748-73.

Figini, P. and Görg, H. (2011). Does foreign direct investment affect wage inequality? An empirical investigation. The World Economy, Wiley Blackwell, 34(9), 1455-1475.

Firebaugh, G. and Goesling, B. (2004). Accounting for the recent decline in global income inequality. American Journal of Sociology, 110(2), 283-312.

Hilbert, M. (2014). Technological Information Inequality as an Incessantly Moving Target: The Redistribution of Information and Communication Capacities Between 1986 and 2010. Journal of the Association for Information Science and Technology, 65(4), 821-835.

Hofmann, B., Shim, I., and Shin, H. S. (2016). Sovereign yields and the risk-taking channel of currency appreciation. BIS Working Papers, no 538, revised May 2017.

The views expressed are those of the authors and not necessarily those of the Bank for International Settlements.