The opinions expressed in this paper are those of the authors and do not necessarily reflect the views of the ECB, Banca d’Italia or the Eurosystem.

The European Union aims to be climate-neutral by 2050, consistent with the commitment to keeping the increase in global average temperature to well below 2°C above pre-industrial levels. While elected governments are primarily responsible for meeting this goal, central banks may also play a role. One option on the table is to design a programme of green asset purchases, the so-called Green QE. We set up a model to study the potential effectiveness of Green QE alongside a transition to an economy with zero carbon emissions driven by a carbon tax. The carbon tax gradually increases over time and leads to progressive pollution abatement by firms. We find that the Green QE is more effective when the carbon tax is absent or low and so the timing of the purchases is crucial for the effectiveness of Green QE. As in the long run emissions go to zero anyway as a result of the carbon tax, so the programme is more useful to reduce emissions in the short/medium run, in order to get a larger effect on the pollution stock. For this reason, a temporary but more aggressive program where purchases are concentrated in the short run and then the portfolio is slowly run down is more effective than a gradual and long-lasting one of a similar size. While in our model the overall impact of this policy is somewhat limited, it does not capture other channels that can play an important role (e.g. signalling effect and R&D investments).

As of March 2022, almost all countries in the world had ratified the Paris Agreement, which has the ambitious goal of keeping the global temperature rise in the current century well below 2 degrees Celsius above pre-industrial levels. The European Union aims to be climate-neutral by 2050, by reaching net-zero greenhouse gas emissions. Designing effective environmental policies to meet these goals is primarily a task for elected governments, which manage the most appropriate instruments to address the climate challenge.

Several economists have suggested that central banks may also play a role in mitigating the increase in global temperature: according to De Grauwe (2019), Schoenmaker (2019), Brunnermeier and Landau (2020), one option is to design a programme of green asset purchases, the so called Green QE. Central banks such as the ECB, the Bank of England, and the Sveriges Riksbank have indeed started to study how to decarbonize their balance sheets and in particular their monetary policy portfolios.

In Ferrari and Nispi Landi (2022a), we analyze a permanent Green QE along the transition to a carbon-free economy, as opposed to a temporary Green QE (as in Ferrari and Nispi Landi, 2021). We set up a general-equilibrium model with two sectors: a green sector, which does not pollute, and a brown sector, whose production generates CO2 emissions and adds to the stock of atmospheric carbon. Brown firms reduce their emissions by spending on abatement. We assume that households enjoy utility from investing in green bonds and suffer disutility from investing in brown bonds. This assumption breaks the Wallace neutrality (Wallace, 1981), making green and brown bonds imperfect substitutes for households in the short and in the long run: if the central bank purchases green bonds by issuing reserves the spread between green and brown interest rates (the so-called “greenium”) widens (i.e. it becomes more negative), reducing brown production and emissions.

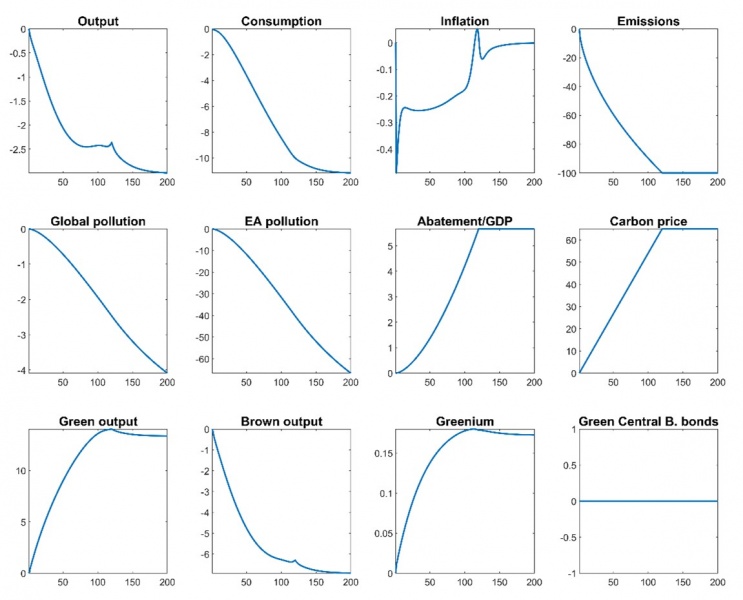

First, we simulate the transition to a carbon-free economy, without the intervention of the central bank (Figure 1). We assume that period 0 corresponds to 2019Q4, when the government introduces an emission tax that increases linearly for 120 quarters, such that by 2050 all emissions are abated. To fully abate emissions, the carbon price reaches around 65 Euro per ton of CO2 in 2050. This environmental policy is costly in terms of consumption, which strongly decreases along the transition. Interestingly, we find that the green transition is deflationary: as we show analytically in Ferrari and Nispi Landi (2022b), under perfect foresight the reduction in aggregate demand driven by lower expected income more than offsets the reduction in aggregate supply driven by higher tax costs.

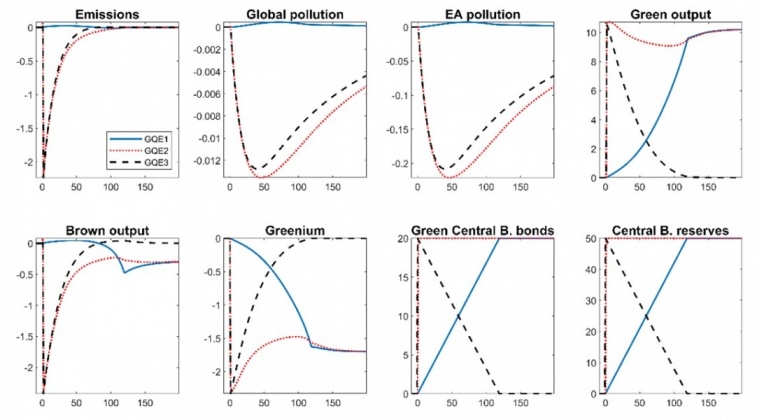

Second, we simulate the effect of Green QE along the transition. We assume that Green QE consists of a 50% increase in the stock of central bank’s reserves, which finances the purchase of green bonds only. We consider three different types of green purchases on top of the green transition (Figure 2), evaluated as deviations relative from the scenario represented Figure 1, i.e. with no central bank purchases. In the blue solid line, we simulate a gradual permanent increase in the stock of green bonds until 2050 (GQE1). In the red dotted line, we consider instead a one-shot permanent increase in the stock of green bonds by the central bank (GQE2). Finally, in the black dashed line, we simulate a transitory increase in the stock of green bonds, which gradually dies out over time until 2050, when the amount of green bonds comes back to the initial level (GQE3). In all scenarios, the purchase of green bonds by the central bank is only partially offset by households’ sales: green firms issue more bonds. As households enjoy utility by holding green bonds, they sell these bonds to the extent that the green interest rate decreases with respect to the brown rate and to the real policy rate. Green firms face a lower interest rate and expand capital and output. The higher supply of green production reduces its price, shifting demand from brown to green goods. Brown firms face lower demand: they cut production, reducing emissions and pollution.

Figure 1: The transition to a green economy

Note: Transition to a zero-emission economy, driven by an emission tax. Variables are in percentage deviations from the path they would have followed with no environmental policy except for inflation and greenium, whose responses are in quarterly deviations reported at annual rates, and for carbon price, whose response is expressed in level deviations. The path for the emission tax is announced in period 0.

The simulations in Figure 2 suggest two main results. First, green QE is more effective when the emission tax is absent or very small. The emission tax induces firms to spend in abatement, which in turn implies a lower reduction in emissions for any decrease in brown output: in other words, the tax weakens the link between brown production and emissions, which is the main channel of Green QE. For this reason, the timing of the purchases is crucial for the effectiveness of Green QE. Given that in the long run emissions go to zero anyway because of the emission tax, it is more useful to reduce emissions in the short/medium run, to get a larger effect on the pollution stock. This allows earlier permanent or transitory purchases (GQE2 and GQE3, respectively) to be more effective than permanent gradual purchases (GQE1). Remarkably, the transitory purchase has an effect comparable to the permanent-one shot purchase, without breaking the market-neutrality principle in the long run. Second, the impact on euro-area pollution is small in every scenario: at the peak, pollution driven by euro-area emissions falls only by 0.2% under GQE2 and GQE3, compared to the scenario with no Green QE. This evidence confirms the results of our previous study (Ferrari and Nispi Landi, 2021), extending those findings in a model for the green transition: Green QE is a limited tool to address the climate challenge under our model assumptions. Within these limits, the analysis suggests that the benefits of green purchases are more significant if they take place in the early stages of the transition, while their effectiveness decreases as environmental fiscal policy is enacted. However, our model is admittedly simple and does not include every channel that may in reality be relevant. For instance, we are abstracting from signaling or liquidity effect of central bank purchases: this could induce households to strengthen their green bias, thus enhancing the effect of central bank green purchases. Moreover, we assume that pollution does not affect TFP and so we are ignoring potentially relevant feedback effects from the environment to economic activity: in our model, the negative effects of climate change are underestimated. The model could be also enriched with an R&D sector, which can produce innovative green technologies that do not pollute or that reduce the cost of abatement, other things equal. By permanently and increasingly altering the relative productivity of the two sectors this could lead to a greater impact of central bank purchases on green production. We leave these extensions for future research.

Figure 2: The impact of Green QE

Note: Variables are plotted as the percentage deviation from the initial steady state in the scenario with Green QE minus the percentage deviation from the initial steady state in the scenario with no Green QE, shown in Figure 1, except the greenium, whose responses is in annualized level deviations, and for green bonds, whose response is in deviation from steady-state GDP. Blue solid line: Green QE is gradual and permanent. Red dotted line: Green QE immediately jumps to the new steady state in period 1. Black dashed line: Green QE is transitory. In all scenarios, Green QE is announced in period 0.

Brunnermeier, M. and Landau J.P., (2020). Central banks and climate change, Vox EU column, available at https://voxeu.org/article/central-banks-and-climate-change

de Grauwe, P. (2019). Green Money Without Inflation, blog post on Social Europe, available at https://www.socialeurope.eu/green-money-without-inflation

Ferrari, A. and Nispi Landi, V., (2021). Whatever it Takes to Save the Planet? Central Banks and Unconventional Green Policy, Temi di discussione (Bank of Italy economic working papers), 1320.

Ferrari, A. and Nispi Landi, V., (2022a). Toward a Green Economy: The Role of Central Bank’s Asset Purchase, Temi di discussione (Bank of Italy economic working papers), 1358.

Ferrari, A. and Nispi Landi, V., (2022b). Will the Green Transition be Inflationary: Expectations Matter, Questioni di Economia e Finanza (Bank of Italy occasional papers), 686.

Schoenmaker, D., (2019). Greening Monetary Policy, Bruegel Working Paper, No. 2019/02.

Wallace, N., (1981). A Modigliani-Miller Theorem for Open-Market Operations”, American Economic Review, Vol. 71, No 3, pp. 267-274.