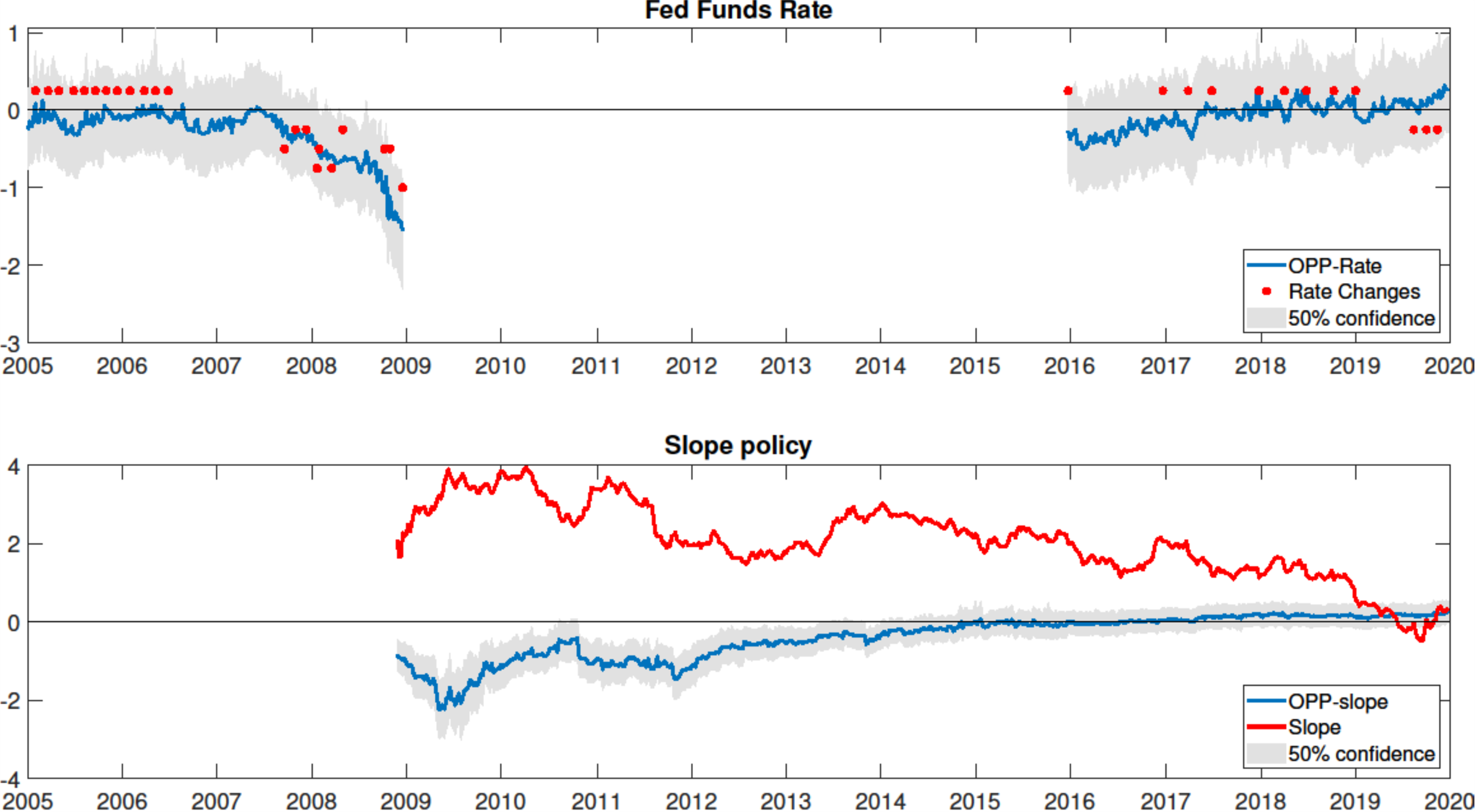

Notes: Top panel: Real-time OPP statistic (in percentage points) for the Fed Funds rate and realized changes to the Fed Funds target rate. Bottom panel: Real-time OPP statistic (in percentage points) for the slope policy and the slope of the yield curve defined as the difference between the 10-year bond yield and the Fed Funds rate. Shaded areas represent impulse response and model uncertainty at 50 percent confidence.

Notes: Top panel: Real-time OPP statistic (in percentage points) for the Fed Funds rate and realized changes to the Fed Funds target rate. Bottom panel: Real-time OPP statistic (in percentage points) for the slope policy and the slope of the yield curve defined as the difference between the 10-year bond yield and the Fed Funds rate. Shaded areas represent impulse response and model uncertainty at 50 percent confidence.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Privacy Overview