References

‘Natural catastrophes an inflation in 2022: a perfect storm’, Sigma, Swiss Re Institute, No 1/2023.

‘Climate Change And Monetary Policy In The Euro Area’, ECB, September 2021.

J. Pisani-Ferry, ‘Climate Policy is Macroeconomic Policy, and the Implications Will Be Significant’, Peterson Institute for International Economics, August 2021.

‘Sectoral Winner And Losers Form The Energy Transition’, Oxford Economics, 1 March 2023.

B. Eichengreen et al., In Defense Of Public Debt, Oxford, 2021.

E. Gagnon et al., ‘Understanding the New Normal: the Role of Demographics’, Finance and Economics Discussion Series, Board of Governors of the Federal Reserve System, 2016.

C. Carvalho et al., ‘Demographic Transition and Low US Interest Rates’, Federal Reserve Bank of San Francisco Economic Letter, 2017.

N. Lisack et al., ‘Demographic trends and real interest rate’, Bank of England Staff Working Papers, 2017.

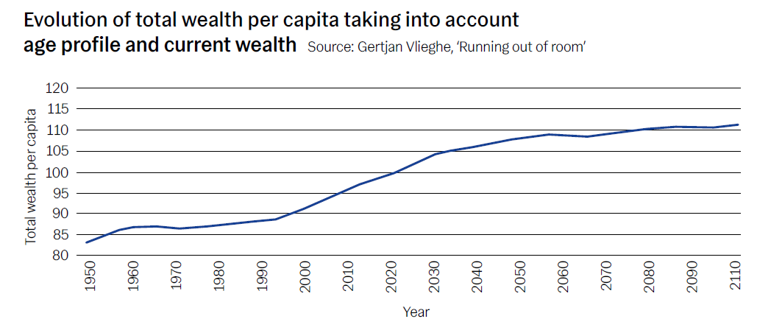

G. Vlieghe, ‘Running out of room: revisiting the 3D perspective on low interest rates’, 26 July 2021.

M. Juselius & E. Takáts, ‘The enduring link between demography and inflation’, BIS Working Papers No 722, May 2018.

R. Baldwin, ‘The Peak globalization Myth: Part 2’, VoxEU, 1 September 2022.

D. A. Cerdeiro et al., ‘Sizing Up the Effects of Technological Decoupling’, IMF Working Paper, March 2021.

A. Azhar, ‘Exponential’, New York, 2021.

A. Bergeaud et al, ‘Productivity Trends In Advanced Countries Between 1890 And 2012’, Review Of Income And Wealth, 62(3), September 2016.

‘Global Economics Comment: Technology and the Productivity Rebound (Zhestkova)’, Goldman Sachs, 19 November 2021.

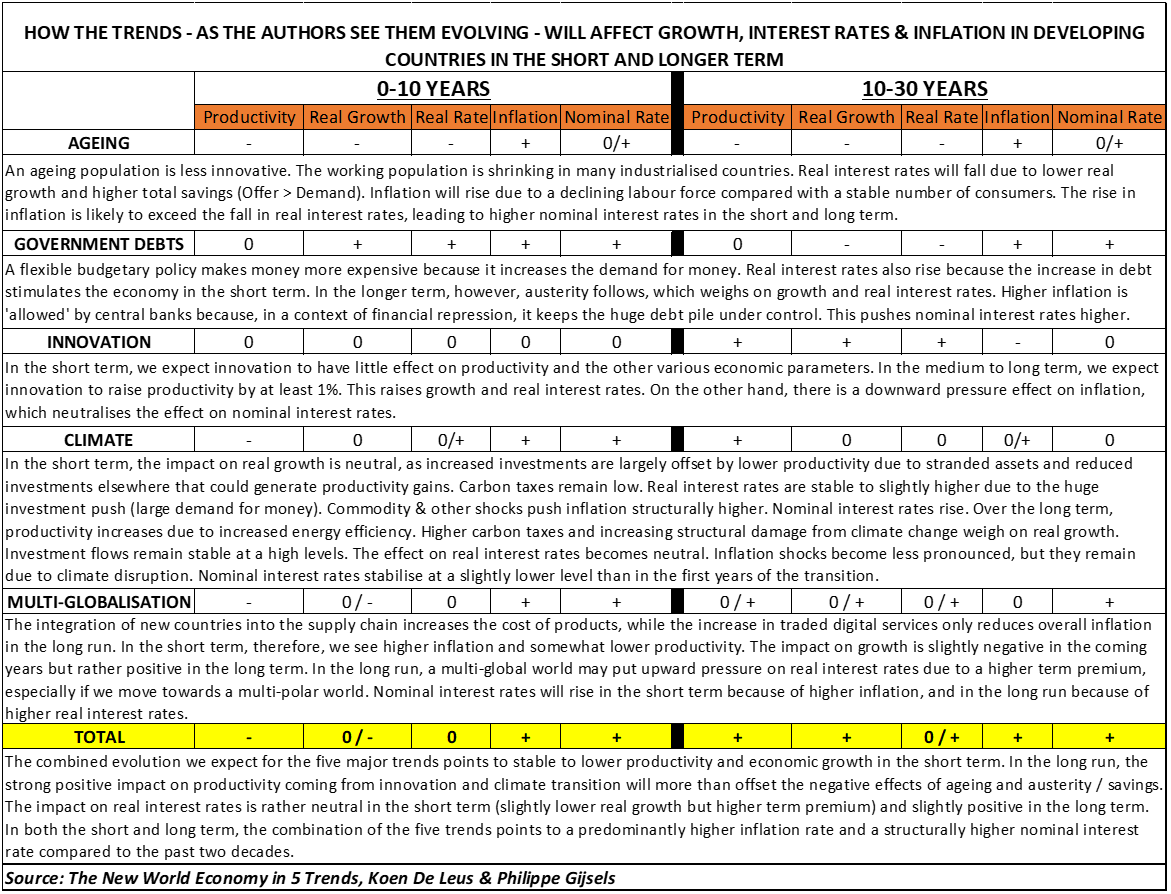

Source: The New World Economy, Koen De Leus, Philippe Gijsels.

Source: The New World Economy, Koen De Leus, Philippe Gijsels.