Climate change has profound effects not only for societies and economies, but also for central banks’ ability to deliver price stability in the future. This Brief starts by documenting why climate change matters for monetary policy: it impacts the monetary transmission mechanism, the policy space available to central banks and has implications for the design of the monetary policy framework. Specific implications are drawn for inflation-targeting central banks. Next, we survey several possible ways central banks can respond to climate change. These range from protective actions to more proactive measures aimed at mitigating climate change and supporting green finance and the transition to a low-carbon economy. We also discuss the constraints and trade-offs faced by central banks as they respond to climate risks. The costs and benefits of any action aimed at proactively mitigating climate change need to be carefully balanced.

Climate change is profoundly affecting our societies and economies. Adapting to it and mitigating its consequences requires a swift transition to a low-carbon economy. The primary responsibility for addressing the market failure inherent in the climate challenge rests with governments. They are legitimised and have a broad spectrum of policy levers at their disposal, such as setting the necessary price of carbon emissions, defining a regulatory framework to reduce emissions, and undertaking needed investments. Yet, government action alone may not be sufficient and fast enough to address the complexity and scale of the economic transformation required to achieve climate goals. Many observers have thus argued that a comprehensive policy package involving fiscal, structural and financial policy instruments would be more effective. Calls have intensified for central banks to support the transition to a low-carbon economy not only in their financial stability capacity, but also with monetary policy measures (Krogstrup and Oman, 2019).

In Boneva et al. (2021), we discuss various rationales why central banks have a clear interest, and in some cases the obligation, to assess the impact of climate change on the economy and financial system, incorporate climate considerations into their policy framework and reflect on how they may support the efforts of their respective governments in achieving carbon emission reduction goals.

First, climate change, and policies to counter it, affect the structure and dynamics of the economy and the financial system, posing risks to both price and financial stability (ECB, 2021). These risks are traditionally divided into physical risk arising from a greater incidence of natural hazards, and the risk arising from the transition to a carbon-neutral economy. They can impact directly on the central banks’ inflation aim, create financial instability and affect the transmission of monetary policy, the equilibrium interest rate and the “room” for conventional monetary policy.

Second, climate change in its various dimensions could increase the riskiness of the assets held on central banks’ balance sheets, potentially leading to financial losses. Climate change risks can translate into higher credit risk by affecting the ability of counterparties, issuers and other debtors to service their obligations (ECB, 2021). Central banks are exposed to such risks directly and over potentially long horizons, through their holdings of financial assets, such as those arising from asset purchases for monetary policy purposes. They can also be exposed indirectly over shorter horizons, for example through collateral pledged by counterparties.

Third, the mandate of many central banks obliges them to support the general economic policies of their respective governments, often subject to the requirement that such actions do not prejudice price stability (Dikau and Volz, 2021). Central banks can decide to support the transition to a low-carbon economy, by investigating how climate considerations can be integrated into their monetary policy frameworks and operations. They can also avoid inadvertently obstructing or acting counter to these policy objectives through their operations, for example by favouring polluting sectors.

Macroeconomic and financial market disruptions linked to climate change and transition policies can affect the conduct of monetary policy and the ability of central banks to deliver on their price stability mandate through various channels (ECB, 2021).

Several studies postulate that the carbon transition might lift the general level of prices and render it more volatile and less predictable overall (McKibbin et al., 2020). Extreme weather events may also lead to upward pressure on commodity and food prices, and hence on inflation.

Moreover, the stranding of assets and sudden repricing of climate-related financial risks could generate losses in the financial system and impair financing flows to the real economy, affecting the transmission of monetary policy.

Climate change could also make it harder to identify a monetary policy stance that is considered “neutral”. The natural rate of interest (r*) provides an important benchmark to assess how accommodative the monetary policy stance is given the level of the policy rate. Several risks related to climate change may imply a dampening force on r*, on top of the factors that have already driven its secular decline over the past few decades.2 At the same time, green investments and new technologies could push r* up, all else being equal. The net effect of these two opposing forces is uncertain ex ante. Should the downward forces prevail, the lower r* would reduce the policy space for conventional monetary policy. Among other things, this would strengthen the case for non-standard measures to become part of the ordinary monetary policy toolkit.

ECB (2021) presents some model simulations illustrating how physical and transition risks related to climate change could combine with existing financial and fiscal fragilities, which themselves could be the result of the materialisation of climate risks, and could significantly restrict the ability of monetary policy to respond to standard business cycle fluctuations.

Climate change could also bear implications for the design of the monetary policy regime. Focusing on inflation-targeting central banks, by far the most popular monetary policy regime worldwide, in Boneva et al. (2021) we consider how certain design features of this framework might interact with, and evolve in response to, the climate challenge.

Inflation-targeting central banks may re-examine the link between headline and core inflation to look through shocks when they are assessed to be temporary and do not threaten the anchoring of inflation expectations. Appropriate communication emphasizing the relative stability of underlying inflation measures may underpin the case for a policy stance that looks through those shocks.

The relative merits of point versus range targets may also be reconsidered. Point targets precisely communicate the policy aim of the central bank, signal the medium-term nature of the inflation objective, and anchor expectations. Range targets, or tolerance bands, convey the sense that inflation does not need to be kept at a specific value at any point in time, thereby adding policy space for the central bank to accommodate temporary shocks to prices and permitting a certain degree of output stabilization. However, range targets may blur the precision of the inflation target and lead to less stable inflation expectations in a situation in which strong inflation shocks may increase the risk of de-anchoring.

Concerning the target horizon, as climate-related shocks impact the economy over different horizons and with different persistence, inflation-targeting central banks may need to monitor the optimal length of the policy horizon. While longer target horizons can limit the decline in output and employment and mitigate their volatility, under flexible inflation targeting, the credibility of the central bank may be at risk if the time horizon is extended too far into the future and inflation misses become too frequent.

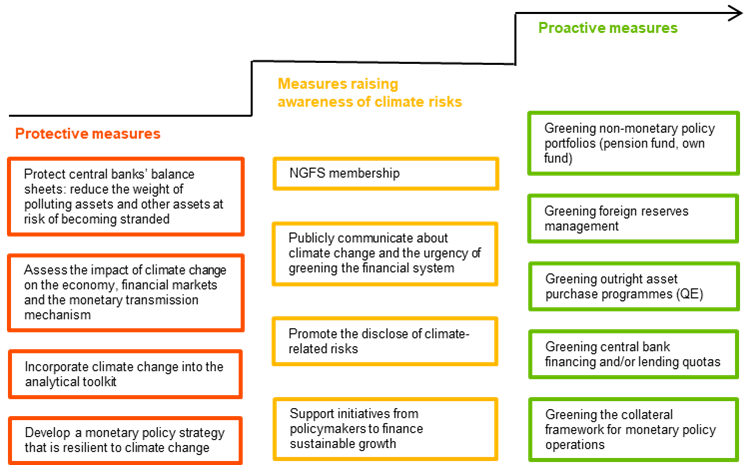

The literature on the policy options available to central banks to respond to climate change is vast and still fragmented. We propose a classification of several policy measures into three categories ranging from protective to proactive depending on their aim (Figure 1).

Figure 1. Possible central bank actions to respond to climate change

The first category includes measures protecting central banks’ balance sheets and preserving their ability to deliver on their price stability mandate against the materialisation of climate risks. Central banks have a duty to preserve the integrity of their balance sheets and prudently manage the resources entrusted to them as a means of ensuring that they are consistently able to deliver on their price stability mandate over time. Policies could be considered to reduce the weight of assets at risk of becoming “stranded” in central banks’ portfolios, provided there is evidence that these risks are not correctly understood and priced by the markets and that such assets can be objectively identified. Measures aimed at expanding and enhancing the central banks’ analytical toolkit to gain a better understanding of the impact of climate change on the economy also belong to this category. This involves developing new models to assess the impact of climate change on the economy and financial markets (NGFS, 2020 and 2021). Monetary policy frameworks should be reviewed to assess how they may adapt to climate-related risks and shocks, as recently done by the ECB (2021).

The second category includes measures aimed at raising awareness of climate risks that could also help to promote green finance and sustainable growth but without the central bank having to make an active use of its balance sheet. They cover a range of actions, from communicating with the public and financial community about climate risks to disclosing the carbon footprint of the central banks’ own balance sheets. These measures might benefit from a classification scheme to rank sectors and activities and sort polluting from green investments – such as the EU Taxonomy – promoting more efficient market pricing of climate risks. Many central banks are also actively contributing to the work of the Network for Greening the Financial System (NGFS), a forum of central bankers and financial supervisors.

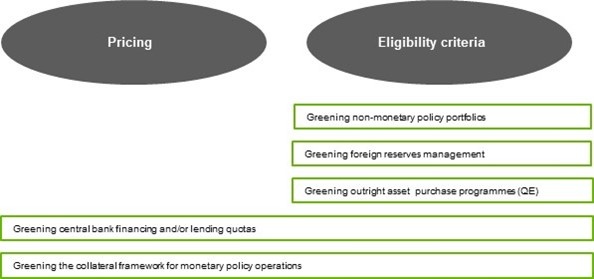

The third category of measures includes actions aimed at proactively mitigating climate change and promoting the transition to a low-carbon economy, including through an active use of central banks’ balance sheets. Some of these measures might be regarded as controversial and expose central banks to trade-offs. Depending on central banks’ legal mandates and operational framework, active support for the transition to a low-carbon economy can be achieved by either changing the pricing of central bank facilities or changing the eligibility criteria (Figure 2). Given the size of current central banks’ balance sheets, the effects of greening central banks’ portfolios could be substantial in some cases. Moreover, there could be important signalling effects for market participants, compounding the direct effects.

Figure 2. Greening central banks’ portfolios via the pricing or eligibility criteria

Non-monetary policy portfolios, such as staff pension funds and own funds, constitute a suitable starting point for actively greening central banks’ portfolios. Many central banks have already taken steps in this direction.

Recently, some central banks have also started allocating part of their foreign reserves to green securities. This is likely to create further trade-offs for reserve managers because of the potentially lower liquidity of green bonds and their still relatively small market share. However, in an illustrative exercise, BIS (2019) finds that holding both green and conventional bonds can help central banks improve risk-adjusted returns by reaping diversification benefits.

The policy portfolios of all major central banks have grown in recent years due to a need for protracted asset purchases to achieve price stability when the policy rate has hit its lower bound. Many central banks carry out these purchases in proportion to outstanding market shares. However, this practice gives rise to a “carbon bias” in central banks’ portfolios because carbon-intensive companies are usually also capital-intensive and so have a larger weight in corporate bond markets compared to their less carbon-intensive peers. Given this “climate change market failure”, traditional benchmarks for central banks assets purchases based on market neutrality might not be appropriate to support the transition towards a low carbon economy. Schoenmaker (2021) proposes a tilting approach that steers central bank asset holdings towards low-carbon companies.

Similarly, bank lending also reveals a carbon bias. To counter it, central banks might condition access to certain credit facilities on how much individual counterparties contribute to climate change mitigation and adaption through their lending, or how much they plan to do so in the future. For example, concentration limits for high-polluting assets or minimum shares of low polluting assets could be required for counterparties to access certain central bank facilities, as discussed for example in NGFS (2021).

Moreover, central banks can green their implementation framework by reviewing the pricing or eligibility criteria for collateral they accept as part of lending operations. This could be done by introducing climate-related disclosure requirements for using private sector assets as collateral in central bank operations. Alternatively, central banks could pursue negative or positive screening for certain types of financial assets when used as collateral, if feasible.

Central banks taking an active role in raising awareness about climate risks are likely to encounter diverse constraints and criticisms. For example, publicly communicating about the urgency to green the financial system could be perceived as an attempt to acquire more tasks and accumulate more powers.

Most central bank mandates do not explicitly refer to sustainability (Dikau and Volz, 2021). However, around half of central banks worldwide have an indirect mandate to support the policy objectives of their respective governments. This raises the question whether an indirect mandate is sufficient to cover a more active role by the central bank in tackling climate change.

In the case of a central bank wishing to deliver a desired monetary stance in a “green way”, the timing or phasing-out of some measures could be affected by the particular phase of the monetary policy cycle. For example, the fact that an asset purchase programme is expected to be wound down as inflation sustainably reverts back to a level consistent with the central bank’s inflation goal means that this type of instrument cannot be used as a permanent tool for the central bank to support climate-related objectives.

Greening monetary policy could also distort financial markets, especially given the current scarcity of green assets. The transmission of monetary policy could be hampered if, for example, certain institutions are excluded from accessing central bank facilities. Moreover, in the absence of a clear taxonomy and accepted market standards of what is “green” and what is polluting investment, and without implementable guidelines, central banks lack an objective definition and possibly a legal underpinning to ground their green policies. Given these constraints and trade-offs, central banks need to carefully balance the costs and benefits of any activity aimed at proactively mitigating climate change.

BIS (2019), “Green bonds: the reserve management perspective”, Quarterly Review, September.

Boneva, L., Ferrucci, G. and Mongelli, F.P. (2021) “To be or not to be ‘green’: how can monetary policy react to climate change?”, ECB Occasional Paper Series, No 285.

ECB (2021) “Climate change and monetary policy in the euro area”, ECB Occasional Paper Series, No 271.

Dikau, S. and Volz, U. (2021), “Central bank mandates, sustainability objectives and the promotion of green finance”, Ecological Economics, Vol. 184.

Krogstrup S. and Oman, W. (2019), “Macroeconomic and financial policies for climate change mitigation: a review of the literature”, IMF Working Paper, No 19/185.

McKibbin W., Morris, A., Panton, A. and Wilcoxen, P. (2020), “Climate change and monetary policy: issues for policy design and modelling”, Oxford Review of Economic Policy, Vol. 36(3), pp. 579–603.

NGFS (2020), Climate change and monetary policy: initial takeaways, Technical Document, Network for Greening the Financial System, Paris, October.

NGFS (2021), Adapting central bank operations to a hotter world: reviewing some options, March.

Schoenmaker, D. (2021), “Greening monetary policy”, Climate Policy, Vol. 21, Issue 4, pp. 581-592.

The views expressed in this Policy Brief are those of the authors and do not necessarily reflect those of the European Central Bank (ECB).

These include, for example, lower productivity and labour supply due to heat stress and higher morbidity (NGFS, 2020).