This policy brief is based on OECD Artificial Intelligence Paper No. 41, and as such it does not necessarily represent the official views of the OECD or of its member countries. The opinions expressed and arguments employed are those of the authors.

Abstract

This policy brief presents findings from the paper by Filippucci et al. (2025) on macroeconomic productivity gains from AI in G7 economies. Adapting the task-based framework of Acemoglu (2024) to a sectoral context, it combines existing estimates of micro-level performance gains with evidence on the exposure of activities to AI and likely future adoption rates. Across three scenarios considered – assuming AI adoption at a slow, medium or fast pace -, the projected annual aggregate labour productivity growth ranges between 0.4-1.3 percentage points in countries with high AI exposure due to stronger specialisation in highly AI-exposed knowledge intensive services such as finance and ICT and more widespread adoption (e.g. United States and United Kingdom). In contrast, the estimated range is 0.2 to 0.8 percentage points in countries where these determinants of AI gains are less favourable (e.g. Italy, Japan).

Fostering productivity growth remains a central priority for G7 countries amid persistently weak productivity performance weighing on per capita income and living standards. Artificial Intelligence (AI), with its rapidly expanding capabilities across diverse applications, is often viewed as the next General-Purpose Technology (GPT), comparable to electricity or digital innovations such as computers and the internet (Filippucci et al., 2024). Historically, transformative GPTs have often triggered periods of accelerated economic expansion (Varian, 2019; Agrawal, Gans and Goldfarb, 2019; Lipsey, Carlaw and Bekar, 2005). While uncertainty surrounds the future trajectory of AI – from scenarios of stagnation without major breakthroughs to the possibility of an Artificial General Intelligence (AGI) revolution where AI surpasses human-level abilities in all cognitive tasks – its emergence fuels optimism about a potential revival of productivity growth.

Predictions about AI’s macroeconomic impact on productivity vary significantly across recent studies. Depending on the choice of modelling frameworks and assumptions feeding into the calculations, predictions for labour productivity growth range from 0.1 percentage point annual growth over the next decade (Acemoglu, 2024) to about 1 percentage point (Aghion and Bunel, 2024; Filippucci et al., 2024) with even more rapid and accelerating growth if AI achieves AGI capabilities (Trammell and Korinek, 2023). However, most estimates in the literature tend to focus on the United States, with some exceptions that also provide assessments, for example, for Europe (Bergeaud, 2024; Misch et al., 2025).

This policy brief presents findings from the paper by Filippucci et al. (2025) on macroeconomic productivity gains from AI in G7 economies. Building on Acemoglu (2024) and on previous OECD research, it combines existing estimates of micro-level performance gains with evidence on the exposure of activities to AI and likely future adoption rates. Because harmonised data on AI adoption are lacking across countries, this study contributes by estimating and projecting firms’ high-intensity AI use in core business functions today and over the next decade.

To project sector-level productivity gains over the next decade, our work adapts Acemoglu’s (2024) analytical framework to a sector-specific context. The empirical application of this micro-to-macro approach incorporates three core elements: (1) micro-level productivity gains driven by AI, (2) the degree of exposure of tasks within each sector, and (3) forecasts of future AI adoption among firms. Wherever possible, the quantification of these three elements is based on country-specific assumptions. Further details on these components are set out below.

Recent research on the aggregate gains from AI primarily draws on micro-level evidence of performance improvements among workers that adopt AI. Micro-level experimental studies consistently show that AI enhances workers’ productivity across a wide range of tasks. For example, studies report gains of around 14% in customer service, up to 56% in coding, and significant improvements in areas such as professional writing and business consulting. To mitigate the risk that results from controlled experiments may disproportionately reflect instances where AI is particularly effective, we adopt a conservative approach. Specifically, our analysis relies on the three most precisely estimated effects, yielding an average baseline impact of 30%. Because much of these measured improvements reflect time savings in task completion while making use of both labour inputs and capital inputs (e.g. computers, office space), we interpret the gains as contributing to total factor productivity.

The potential for AI-driven productivity gains in a sector depends on two factors: first, the exposure of different tasks to AI and, second, the sector’s task composition. The identification of AI-exposed tasks relies on task-level AI exposure estimates provided by Eloundou et al. (2024) for each task in the O*NET database. Accordingly, individual tasks are evaluated based on whether they can be carried out significantly faster with the help of AI. Depending on the underlying AI capabilities – either baseline AI capabilities of Large Language Models (LLMs) as of 2023 or expanded capabilities enabled by additional software built on top of 2023 LLMs – a distinction is made between baseline exposure and expanded capabilities exposure of tasks. Aggregate AI exposure is calculated as the share of tasks within a country’s economy that are exposed to AI.

Exposure to AI varies across sectors in G7 economies, with knowledge-intensive services being the most affected. These services rely strongly on cognitive tasks, such as finance, ICT services (including software development, data services and telecoms), publishing and media, and professional services. In these sectors, between 50% and 80% of tasks are exposed to AI, depending on whether baseline or expanded AI capabilities are assumed. In contrast, the least exposed sectors include sectors with a strong manual, physical task component, such as agriculture, mining and construction. In these sectors, between about 10% and 30% of tasks are exposed to AI.

Given the important variation in AI exposure across different sectors, the sector composition of G7 economies plays a crucial role in determining to what extent micro-level productivity gains from AI materialise at the aggregate level. The value-added shares of the five most AI exposed sectors – ICT services, telecom, publishing and media, finance, professional services – varies substantially across the G7, ranging from 15% to 25%. In the United States, about one quarter of the economy consists of sectors that benefit the most from AI, predominantly driven by a large share of finance and professional services, i.e., consulting, legal and accounting, engineering, and science. The United Kingdom shows similarly high figures, around 23%. However, this share is much lower – around 15% – in G7 countries focused more on manufacturing or less knowledge intensive, personal services, such as Japan, Italy, or Germany.

In the empirical framework underpinning this policy brief, the adoption of AI by firms is a key determinant of macroeconomic productivity gains. To measure the share of firms using AI in all tasks that are exposed to the technology, we need to retrieve harmonised estimates of the share of firms that adopt AI in a systematic way. We thus focus on a more conservative proxy of AI adoption: AI use in core business functions – thus going beyond the ad-hoc use of AI, such as occasionally drafting an email with the help of a language model. However, the accurate identification of such AI use faces significant data challenges. Among national statistical offices of G7 countries, there are substantial differences in how data on AI adoption are collected – with variation in (i) questions on the purpose of AI use, (ii) the time period the statistics refer to, (iii) firm size coverage, (iv) industry scope, and (v) the survey design, i.e., the definition of a statistical unit and exemplary AI use cases.

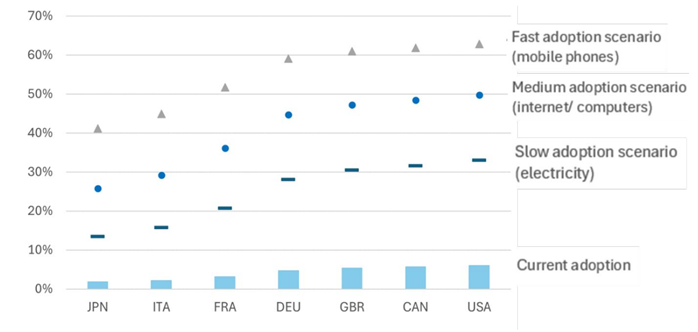

To address these discrepancies, we harmonise existing surveys that are sufficiently comparable in measuring high intensity, regular AI use by firms in core business functions. When such adoption rates are unavailable or highly incomparable with the majority of G7 countries (as is the case for the United Kingdom and Japan), we use imputed values from regressions that link adoption to digital infrastructure, skills and the sectoral composition of the economy. Finally, we project future AI adoption over the next 10 years, drawing on the diffusion patterns of past general-purpose technologies, which typically spread along an S-shaped curve, with gradual and then accelerating uptake followed by a slowdown near saturation. Importantly, we distinguish between slow, medium, and fast adoption scenarios, based on the historical experience with electricity, computers and the internet, and mobile phones, respectively.

Our estimations project that AI adoption levels will vary significantly across G7 countries by 2034. Across considered AI adoption scenarios – slow, medium and fast-, AI adoption in 2034 is expected to range from 30% to about 60% for the United States, Canada, the United Kingdom and Germany, while lower AI adoption levels are predicted for France, Italy and Japan, ranging between 15% to 50%. These differences across countries in terms of future assumed adoption rates reflect the ranking of estimates for current AI adoption levels – in which the United States, Canada and the United Kingdom, for example, show highest AI adoption across countries.

Figure 1. The expected increase in AI adoption varies a lot across countries

Current and future (10-year ahead), AI adoption rates based on the S-shaped adoption paths seen in GPTs, % of businesses

Note: Current adoption rates are taken from official national statistics after harmonisation steps (CAN, EU, United States) or when this is not possible, using predictions as a function of the digital infrastructure, skills and the sectoral composition (JPN, GBR).

Source: Authors’ calculations.

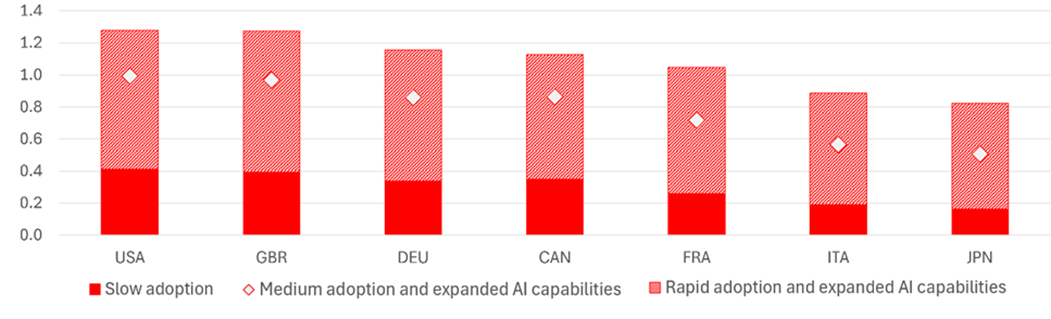

Our predictions for AI’s contribution to annual labour productivity over the next decade vary considerably across G7 economies and adoption scenarios (see Figure 2). Under the slow adoption scenario, estimates range from 0.2 to 0.4 percentage points, rising to between 0.5 and 1 percentage point under the medium adoption with expanded capabilities scenario, and further to 0.8 to 1.3 percentage points under the rapid adoption and expanded capabilities scenario. The variation in predicted productivity gains across G7 economies reflects both the pace of AI adoption and the sectoral composition of national economies. Japan and Italy, for example, record relatively modest gains (0.2–0.8 percentage points), consistent with their smaller share of AI-driven, knowledge-intensive services and greater reliance on manufacturing, where current AI applications remain limited. By contrast, the United Kingdom and the United States, with a stronger concentration of AI-affected sectors, show higher estimated gains of 0.4–1.3 percentage points. To put these numbers into perspective, during ICT boom in the United States in the mid-90s the contribution of ICTs to annual labour productivity growth was estimated to be about 1-1.5 pp per year (Byrne et al., 2013; Bunel et al., 2024).

Figure 2. AI’s macroeconomic productivity gains can be significant but adoption and sectoral specialisation are key

Predicted labour productivity growth contributions by AI over the next 10 years (in annualised percentage points)

Note: This figure shows projected annual labour productivity growth from AI over the next decade, based on three components: micro-level gains × AI exposure × AI adoption. Projections are provided for three scenarios: “slow adoption” with baseline AI capabilities, “medium adoption and expanded AI capabilities”, and “rapid adoption and expanded AI capabilities”. Source: Authors’ calculations.

Harvesting aggregate gains from AI is based on the effective use and adoption of AI by businesses and access to the globally most advanced AI models. Policymakers can consider a range of policy areas such as investing in digital infrastructure for AI – including high-speed, high-quality internet access and the presence of data centres -, strengthening AI-related skills including in the field of STEM sciences and ensuring healthy competition (OECD, 2023; Andre et al.,2025). Moreover, in view of often uneven productivity growth across sectors, policymakers should also aim for easing the movement of labour and capital across sectors, which may otherwise limit the overall economic benefits. In this context, enhancing retraining programs for workers and ensuring the effective functioning of capital markets are crucial steps. To inform such policies and strengthen the understanding of the drivers and mitigating factors needed to harness the benefits of AI, the OECD is advancing research – for instance, on how trade can affect the welfare impact of AI-driven productivity – while also stepping up efforts to collect and harmonise AI-specific data, including through the AI Observatory. In this context, sustained efforts by policymakers to achieve broad harmonisation of underlying data on AI adoption, particularly at the sectoral level, are essential.

Acemoglu, D. (2024), “The Simple Macroeconomics of Artificial Intelligence”, Economic Policy, 2024, eiae042, https://doi.org/10.1093/epolic/eiae042.

Aghion, P. and S. Bunel (2024), “AI and Growth: Where Do We Stand?”, https://www.frbsf.org/wp-content/uploads/AI-and-Growth-Aghion-Bunel.pdf.

Agrawal, A., J. Gans and A. Goldfarb (2019), “Economic Policy for Artificial Intelligence”, Innovation Policy and the Economy, Vol. 19.

Andre, C., M. Betin, P. Gal and P. Peltier (2025), “Developments in Artificial Intelligence Markets: new indicators based on model characteristics, prices and developers”, OECD Artificial Intelligence Papers, No. 37, OECD Publishing, Paris, https://doi.org/10.1787/9302bf46-en.

Bergeaud, A. (2024), “The Past, Present and Future of European Productivity”, paper prepared for the ECB Forum on Central Banking Monetary policy in an era of transformation, 1-3 July 2024, Sintra, Portugal.

Bunel, S., G. Bijnens, V. Botelho, E. Falck, V. Labhard, A. Lamo, O. Röhe, J. Schroth, R. Sellner, J. Strobel and B. Anghel (2024), “Digitalisation and productivity”, Occasional Paper Series 339, European Central Bank.

Byrne, D. M., S. D. Oliner and D. E. Sichel (2013), “Is the Information Technology Revolution Over?”, International Productivity Monitor, Centre for the Study of Living Standards, vol. 25, pages 20-36, Spring.

Eloundou, T., S. Manning, P. Mishkin and D. Rock (2024), “GPTs are GPTs: Labour market impact potential of LLMs”, Science, 384 (6702), 1306-1308.

Filippucci, F., Gal, P., Laengle, K., and Schief, M., (2025), “Macroeconomic productivity gains from Artificial Intelligence in G7 economies”, OECD Artificial Intelligence Papers, No. 41, OECD Publishing, Paris, https://doi.org/10.1787/a5319ab5-en.

Filippucci, F., P. Gal and M. Schief (2024), “Miracle or Myth? Assessing the macroeconomic productivity gains from Artificial Intelligence”, OECD Artificial Intelligence Papers, No. 29, OECD Publishing, Paris, https://doi.org/10.1787/b524a072-en.

Lipsey, R., K. Carlaw and C. Bekar (2005), “Economic Transformations: General Purpose Technologies and Economic Growth”, Oxford University Press, Oxford United Kingdom.

Misch, F., B. Park, C. Pizzinelli and G. Sher (2025), “AI and Productivity in Europe”, IMF Working Papers, 2025(067). https://doi.org/10.5089/9798229006057.001.

OECD (2023), OECD Employment Outlook 2023: Artificial Intelligence and the Labour Market, OECD Publishing, Paris, https://doi.org/10.1787/08785bba-en.

Trammell, P. and A. Korinek (2023), “Economic Growth under Transformative AI”, National Bureau of Economic Research Working Papers, No. 31815.

Varian, H. (2019), “Artificial Intelligence, Economics, and Industrial Organization”, The Economics of Artificial Intelligence: An Agenda, pp 399 – 422., University of Chicago Press.