China has become a major player in the global economy. The analysis, based on a new and original database of Chinese macroeconomic surprises, shows the significant impact that these surprises have on equity and commodity markets worldwide, on the US nominal effective exchange rate, and on the VIX Index. We also establish that positive Chinese macroeconomic news is associated with an expansion of global trade and world industrial production. Overall, we provide evidence of the growing role of the Chinese economy as a driving force for both the real and the financial global cycle.

China’s economic developments have attracted growing global attention; this is not surprising since this country is the second-largest economy in terms of GDP, accounting for 18.5% of global output, and it has a significant presence in the equity market, representing 10.5% of global equity capitalization. Moreover, China’s role as the largest importer of various commodities further amplifies its economic influence. Although there is a widespread consensus that Chinese developments matter for the global economy, accurate assessments of China spillovers are still rare. First, the idiosyncratic mechanisms and institutional settings governing the Chinese economy complicate the identification of the policy tools employed by the Chinese authorities. Second, some recent works have questioned the reliability of official Chinese statistics, in particular its GDP figures (Fernald et al. 2021, Clark et al. 2017). Consequently, the existing literature has generally encountered difficulties in evaluating the international spillover effects originating from the Chinese economy; some exceptions being Miranda-Agrippino et al. (2020) and Barcelona et al. (2022).

In this study, we propose an alternative approach to assess the spillover effects of the Chinese economy on the rest of the world, building on the framework proposed by Boehm and Kroner (2023) for the US economy. To this purpose, we first construct a novel dataset of Chinese macroeconomic news leveraging the information reported by the Refinitiv economic monitor. Specifically, for a list of key macroeconomic variables, we define surprises as the difference between the analysts’ estimates provided by Refinitiv in its “Smart Estimate” and the released macroeconomic value; this value is then normalised by its standard deviation over our sample (2018-2022).

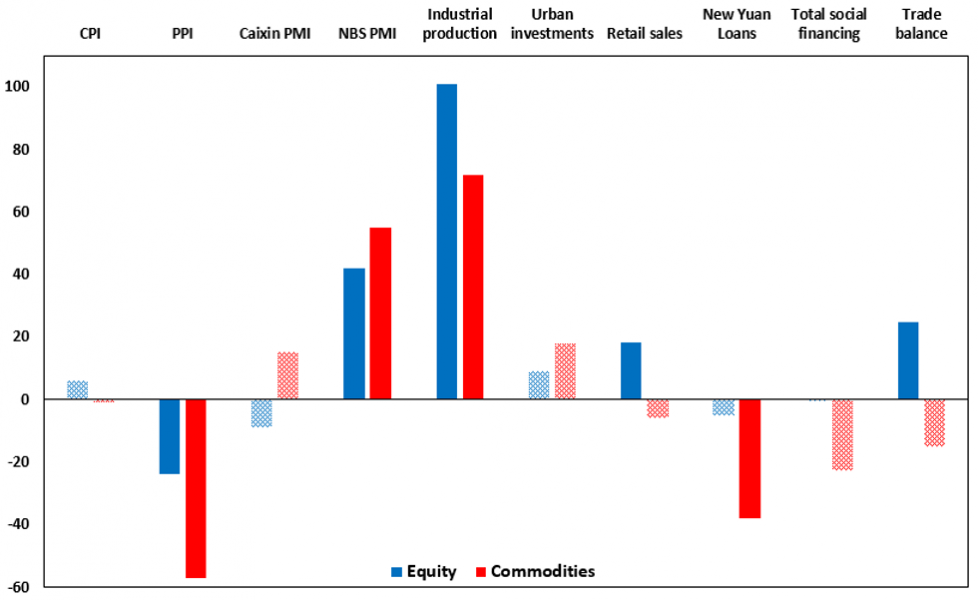

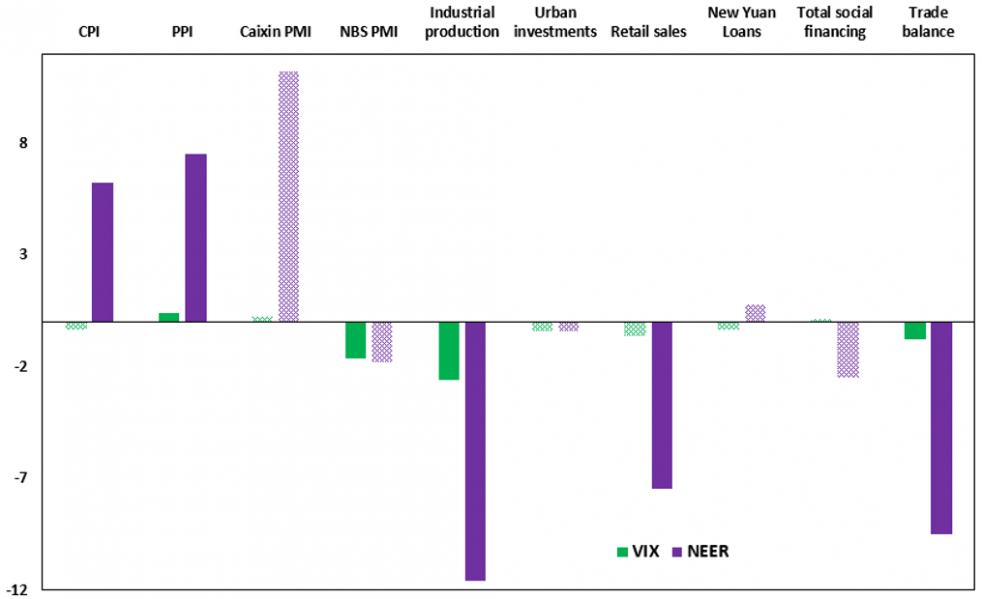

In our first empirical exercise, we assess the influence of macroeconomic surprises on the daily performance of international financial markets, commodity prices, and the level of risk aversion, which we proxy using the US dollar nominal effective exchange rate (US NEER) and the VIX. Results are reported in Figure 1 and are expressed as the reaction of the dependent variable to a one standard deviation increase in Chinese macroeconomic surprises. The impacts exhibit sound signs and are statistically significant for abound half of the variables, in particular for the producer price index (PPI), the NBS PMI index, industrial production, retail sales, and the trade balance. As an example, focusing on industrial production, which presents the most sizable average impact across various types of macroeconomic announcements, a one standard deviation increase in the macroeconomic surprise is associated with an increase of 101 basis points in stock market returns, 72 basis points in general commodity index returns, 12 basis points in the US NEER, and nearly 3 index points in the VIX. These findings remain consistent at a lower frequency as well, wherein we aggregate the informational content of Chinese macroeconomic surprises into weekly and monthly indices, confirming the influence of the Chinese economy on global financial markets and commodity prices.

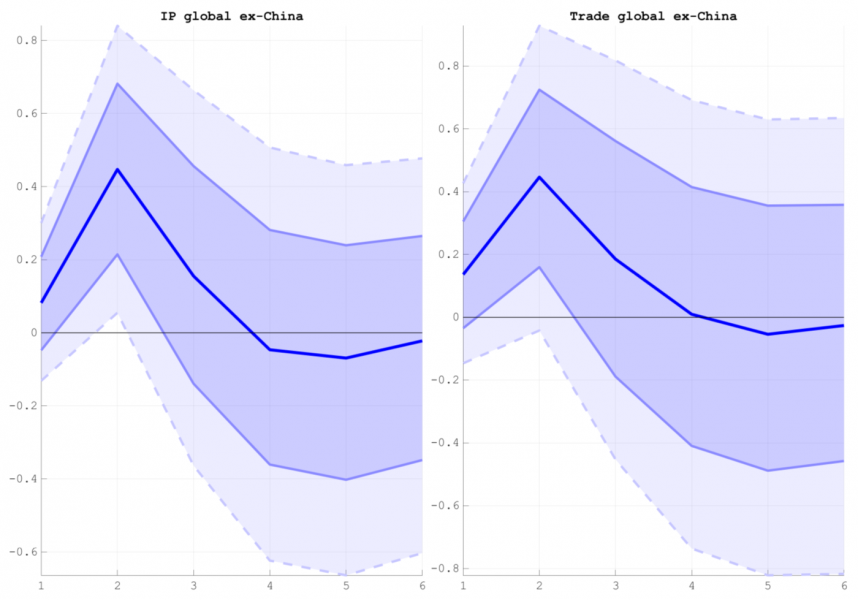

In a second empirical exercise, we evaluate whether the effects of Chinese macroeconomic surprises propagate beyond financial asset prices into global macroeconomic developments. For this purpose, we employ a Bayesian VAR model to assess the dynamic correlation between our series of Chinese surprises and the foreign real economy. We specifically examine the impulse response functions (IRFs) of global industrial production and global trade (both excluding China) to a one standard deviation increase in the monthly aggregated index of Chinese macroeconomic surprises. These impulse response functions provide insights into the spillover effects from the Chinese economy to the rest of the world and are presented in Figure 2. The results indicate that in response to a one standard deviation shock to our Chinese surprise index, both global industrial production and world trade experience an increase of approximately 0.45 percentage points. The shock exhibits a gradual propagation, albeit with noticeable persistence. Therefore, the influence of Chinese surprises holds significance not only from a financial perspective but also from a macroeconomic standpoint.

Figure 1: Impact of Chinese macroeconomic surprises

a) Equity and commodity markets

b) Level of risk aversion (VIX and US NEER)

Note: Impact of Chinese macroeconomic surprises measured in basis points for all variables except the VIX (index points). Shaded bars indicate non-statistically significant estimates.

Figure 2: BVAR – IRFs to an aggregate surprise shock

Note: The Bayesian VAR is estimated on data 2018 – 2022 with two lags under a Minnesota prior. The plots report median response to a one standard deviation increase in the Chinese monthly surprise index (blue solid line) together with 68% (blue shaded areas) and 90% (light blue shaded areas) credible sets.

We uncover that macroeconomic news in China reverberates through the rest of the world with significant and persistent impacts on equity and commodity markets, and on the global risk aversion. We additionally show that positive Chinese macroeconomic surprises are associated with increased global trade and production. Our analysis suggests that the role of the Chinese economy as spillover originator is increasing and international financial markets immediately price its macroeconomic developments. This work paves the way for further exploration of the channels through which the Chinese footprint propagates to the rest of the world: the real dimension, in particular trade and commodity markets, as well as the financial side, wherein financial intermediaries respond to Chinese macroeconomic news, influencing global asset valuations.

Barcelona, W., Cascaldi-Garcia, D., Hoek, J., and Van Leemput, E. “What Happens in China Does Not Stay in China”, International Finance Discussion Paper, (1360) (2022).

Boehm, C. E. and Kroner, T. N. “The US, economic news, and the global financial cycle”, NBER working paper (2023).

Clark, H., Pinkovskiy, M., and Sala-i Martin, X. “China’s GDP growth may be understated”, NBER working paper (2017).

Corneli, F., Ferriani, F., and Gazzani, A. “Macroeconomic News, the Financial Cycle and the Commodity Cycle: the Chinese Footprint”, Economics Letters, forthcoming.

Fernald, J. G., Hsu, E., and Spiegel, M. M. “Reprint: Is China fudging its GDP figures? Evidence from trading partner data”, Journal of International Money and Finance, 114:102406 (2021).

Miranda-Agrippino, S., Nenova, T., and Rey, H. “Global footprints of monetary policies”, CFM, Centre for Macroeconomics (2020).