This policy brief is based on De Haes et al. (2025). The views expressed are those of the authors and not necessarily those of the institutions the authors are affiliated with.

Abstract

We examine whether the Eurosystem’s Corporate Sector Purchase Programme (CSPP) affected bond yields through local supply effects. Using security-level data, we find that purchasing a specific bond did not significantly affect its own price, consistent with the Eurosystem’s market neutrality principle. However, purchases of close substitutes — bonds with similar maturities — significantly reduced yields by 40–45 basis points. These local supply effects are most pronounced for CSPP-eligible, more mature, and lower-rated bonds. Our findings suggest that central bank asset purchases can influence market segments unevenly, with implications for both monetary policy implementation and potential portfolio tilting strategies.

On 10 March 2016, the European Central Bank (ECB) announced the launch of the Corporate Sector Purchase Programme (CSPP), under which the Eurosystem purchased euro-denominated investment-grade bonds issued by non-bank corporations in the euro area. The CSPP was part of the broader Asset Purchase Programme (APP), aimed at easing financing conditions and supporting economic recovery. Purchases under the CSPP continued until December 2018, with the ECB emphasizing a market-neutral implementation strategy.

Our study investigates whether the CSPP generated local supply effects. If such effects are present, the yield on a given security would fall relative to the overall market in response to purchases of that security or, more generally, in response to purchases of securities with similar maturities. In homogeneous, frictionless, markets with full arbitrage, the specific bonds purchased should not lead to yield changes. However, in practice, frictions such as investor segmentation and scarcity of specific securities or close substitutes may cause yields to change due to purchases. D’Amico and King (2013) documented such effects in the U.S. Treasury market; we explore whether similar dynamics occurred under the CSPP.

We focus on stock effects — persistent changes in yields over the full duration of the programme — rather than flow effects, which are typically short-lived and particularly relevant during periods of market dysfunction, which was not the case in our sample period. Our analysis covers the period from the CSPP announcement on 10 March 2016 to the end of net purchases on 20 December 2018. The surprise nature of the announcement allows us to abstract from anticipation effects.

Our dataset includes 944 corporate bonds, of which 603 were CSPP-eligible. We use confidential Eurosystem bond-level purchases and match these with market data on prices, maturities, ratings, and issuance characteristics. As the interaction between asset purchases and yields is prone to endogeneity concerns, we apply a two-stage least squares (2SLS) approach, instrumenting purchase volumes with the following pre-announcement bond characteristics: weeks since issuance, on-the-run status, and amounts outstanding on the day of the CSPP-announcement. We define local supply effects not only for own purchases but also for purchases of substitutes, i.e. bonds grouped into maturity buckets of ±1 and ±2 years.

Our main finding is that own purchases did not significantly affect bond yields. However, for broader maturity buckets, we do find local supply effects. A 1 percentage point increase in purchases within a ±1-year maturity bucket reduced yields by approximately 5 basis points. Given that average purchases in these buckets were around 8.5% of amounts outstanding, the total yield impact is roughly 40–45 basis points. This is larger than the 30 basis points found by D’Amico and King (2013) for the U.S. Treasury market.

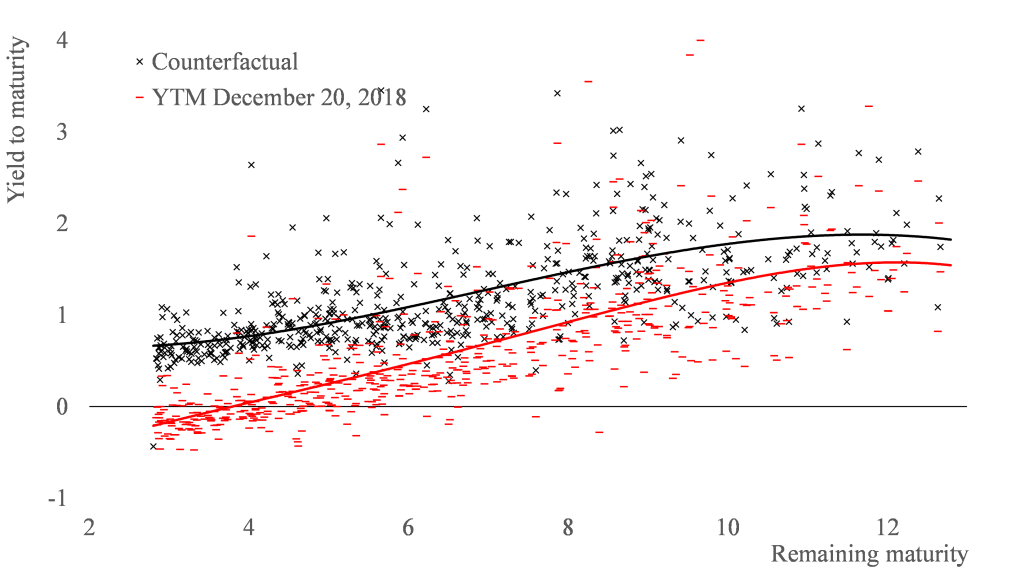

Figure 1 presents a graphical illustration, comparing actual yields at the end of the CSPP with counterfactual yields that adjust for local supply effects. The counterfactual is computed by applying the estimated yield impact from substitute purchases, which is based on bond-specific normalised purchase volumes and durations. The average effect is around 40 basis points, though the impact varies substantially across bonds, highlighting heterogeneity in the corporate bond market compared to more uniform sovereign markets.

The absence of local supply effects for bonds’ own purchases may seem counterintuitive, but we have two explanations for this finding. First, the ECB’s goal of avoiding market distortions meant that securities were selected and calibrated in a market-neutral way, i.e. avoiding any specific price impact on the bond itself. This is in line with findings by DeSantis et al. (2018). Second, own purchases may have encouraged new issuance by corporates whose bonds were bought, increasing supply and mitigating price pressure. We find a positive correlation between own purchases and subsequent issuance, supporting this interpretation. This correlation is insignificant for 1- and 2-year buckets, implying that issuance effects are only relevant for own purchases.

Figure 1. Yield to maturity end-2018 versus counterfactual (percent)

Note: The red dashes are bond-specific yields to maturity on December 20, 2018, i.e. at the end of the CSPP net purchases.

The black crosses are a counterfactual, using our estimates based on the 1-year bucket purchases.

The red and black trend lines are third-order polynomials.

We also explore heterogeneity in the local supply effects. The impact is stronger for:

These patterns are consistent with the preferred habitat theory, which posits that certain investors prefer specific market segments and are less willing to substitute across them. Less liquid or riskier bonds may require larger price adjustments to induce trading, amplifying the effects of purchases.

Our findings have implications for monetary policy implementation and the scope for portfolio tilting strategies. While market neutrality helps avoid distortions, the uneven impact of purchases across market segments suggests that central banks can influence specific sectors if desired. For instance, tilting purchases toward green bonds could lower their yields relative to others, supporting climate-related policy goals without necessarily altering the overall monetary stance.

In conclusion, we provide evidence that the CSPP generated significant local supply effects through purchases of substitute bonds, but not through own purchases. These effects vary across bond characteristics and highlight the importance of market segmentation in the transmission of asset purchase programmes. Our results suggest that central banks can shape market outcomes not only through the scale of purchases but also through their composition.

D’Amico, S., & King, T. B. (2013). Flow and stock effects of large-scale treasury purchases: Evidence on the importance of local supply. Journal of Financial Economics, 108(2), 425–448.

De Haes, Hudepohl and Kakes (2025), The local supply effect of asset purchases: evidence from the Eurosystem’s CSPP, DNB Working Paper No. 837.

DeSantis, R. A., Geis, A., Juskaite, A., & Vaz Cruz, L. (2018). The impact of the corporate sector purchase programme on corporate bond markets. ECB Economic Bulletin, Issue 3, 66–84.