Disclaimer: This policy brief should not be reported as representing the views of De Nederlandsche Bank (DNB) or of the Eurosystem.

Central banks have an interest in supporting an orderly transition to a low-carbon economy, as this would minimize the economic and financial risks posed by climate change. However, the literature has shown that monetary policy measures can have a pro-carbon bias. This article focuses on the climate impact of central bank refinancing operations by taking the third ECB’s Targeted Longer Term Refinancing Operations (TLTRO III) program as a case study. In particular, by combining sectoral emission data with information on banks’ take up and lending, we provide an assessment of its carbon footprint. We then use a theoretical model to show that a green credit-easing scheme in the euro area could increase banks’ costs for lending to polluting companies and, hence, re-direct loans to less-polluting firms. However, the financial stability implications of such a policy should be carefully considered, as well as the related legal and operational challenges.

Climate and environmental risks pose economic, financial and price stability risks. These risks would be minimized under an early and orderly transition to a low-carbon economy. Hence, central banks have an interest in supporting such transition. However, the existing literature shows that some monetary policy measures, in particular corporate bond purchase programs and collateral policies, suffer from a carbon bias, meaning that they disproportionately benefit highly emitting sectors, thus strengthening the carbon lock-in of the economy (e.g. Matikainen et al 2017; Oustry et al 2020).

While scholarly attention has extensively scrutinized these aspects, less attention has been so far devoted to the climate impact of refinancing operations. However, these latter are an important tool of monetary policy and have been already used by some central banks to support the transition to a low-carbon economy. Among the representatives of the major central banks, ECB board members have declared their openness towards a green Targeted Longer-Term Refinancing Operations (TLTRO) program. More recently, board member Frank Elderson has stated: “whenever there is a monetary policy need in the future to reconsider targeted longer-term refinancing operations for banks, there are compelling reasons to seriously consider greening them”.1 Some politicians as well have started to voice their concern about the fact that “[…] the private sector benefits from the same interest rates whether it finances renewables, gas or coal”.2

There are three reasons for the ECB to implement a green TLTRO. First, banks face climate transition risks when lending to polluting firms. As regulatory landscapes evolve to incorporate more stringent climate measures, companies relying on carbon-intensive practices may encounter financial setbacks, translating into potential losses for lenders. This scenario poses risk cascading effects, increasing the likelihood of diminished repayment rates and heightened credit risks, which can directly impact banks’ balance sheets. On aggregate, this could generate financial stability risks, a concern for the proper transmission of monetary policy. By introducing a green TLTRO, the ECB could incentivize banks to lend to green firms and thus induce a transformation in the economy. This shift not only aligns with global sustainability goals but also plays a pivotal role in mitigating financial stability risks by fostering a more resilient economic landscape.

Second, the ECB’s secondary mandate is to support policies implemented by the European Union (EU) and its member states. By aligning monetary strategies with EU objectives, the ECB not only contributes to the larger framework of collaborative policymaking but also amplifies the impact of environmental initiatives.

Third, targeted refinancing operations have been successful in channelling resources to the targeted objectives. Refinancing operations have indeed been effective in increasing lending to specific sectors by reducing the borrowing costs for firms (Afonso and Sousa-Leite (2020), Andreeva et al. (2021), Benetton and Fantino (2021), Da Silva et al. (2021)), without however increasing banks’ risk taking (Barbiero et al. (2022)). In addition, the ECB’s TLTROs have significantly reduced the funding costs of banks, thus ultimately benefiting the real economy. So far, there have been a number of proposals for green targeted lending operations (van ’t Klooster and van Tilburg (2020), Batsaikhan and Jourdan (2021), Böser and Colesanti Senni (2021), Monnet and van ’t Klooster (2023)). Meanwhile, green credit easing schemes have been already implemented by other central banks worldwide, and notably the Bank of Japan, the People’s Bank of China and the Central Bank of Malaysia. Nonetheless, the implementation of these policies is relatively recent and, to the best of our knowledge, there are as of yet no empirical evaluations of such programs. The present article, based on Colesanti Senni et al. (2023), aims at addressing this gap, thus contributing to the ongoing debate on the integration between climate change objectives and central banking practices.

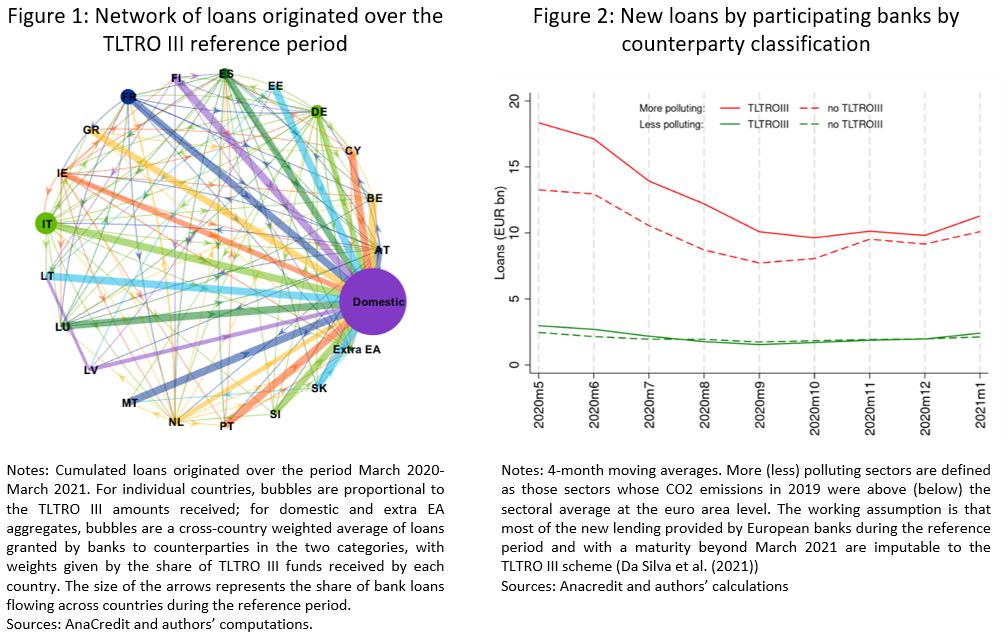

The obvious precedents to consider when talking about credit easing operations in the euro area are the targeted long term refinancing operations (TLTROs), first introduced by the ECB in June 2014. Specifically, the third series of such operations, the TLTRO III, is of particular relevance given its design as well as the remarkably high participation of eligible institutions (around 87% as of March 2020). In our analysis, we focus on the second tranche of the program, between March 2020 and March 2021 (reference period henceforth), since it is the first one featuring a lending rate below the deposit facility rate, which provided participating banks with a risk-free profit of 50 bps per euro borrowed.

In our analysis, we assess the carbon footprint of the program by combining information on: i) the banks’ participation to the TLTRO III during the reference period; ii) new loans granted by participating banks to non-financial corporations; iii) CO2 emissions levels of the counterparts’ sectors. Following part of the literature (Da Silva et al. (2021)), we rely on the working assumption that most of the new lending provided by European banks during the reference period and with a maturity beyond March 2021 are imputable to the TLTRO III scheme. Two interesting evidences emerge from our analysis. First, out of the 1000 participating institutions, 471 have granted new loans maturing beyond March 2021, thus qualifying for a reduction in the lending rate. The total amount of new loans by participating banks is around 25% higher compared to non-participating institutions; around 88% of these loans were granted to domestic counterparts (Figure 1). Second, the increase in new lending by participating institutions during the reference period is driven by loans to more polluting sectors, namely to sectors whose CO2 emissions in 2019 were above euro area sectoral averages (Figure 2). In particular, cumulated loans towards polluting companies represent more than 80% of newly issued loans. All in all, the CO2 emission content of new bank loans granted over the reference period amounts to about 151 CO2 megatons (MtCO2). This corresponds to 8% of overall CO2 emissions in the euro area at the end of 2019.

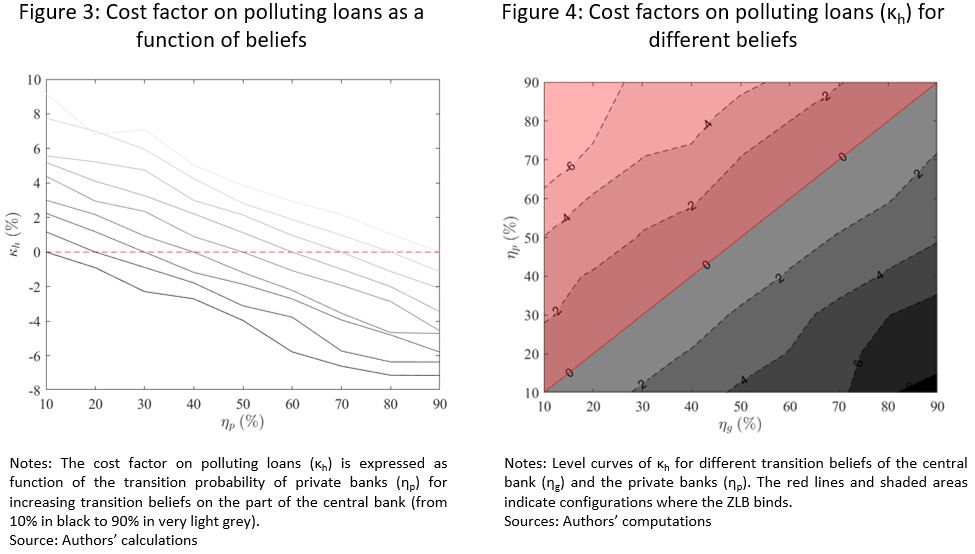

Absent a policy precedent in the euro area, we evaluate the potential effects of a “green” credit easing scheme by calibrating the general equilibrium model of Böser and Colesanti Senni (2021) to the euro area. In the model, two scenarios can materialize: i) the economy remains in the current regime (business as usual) or ii) the transition to a low carbon economy occurs (transition scenario). The central bank and the private banks assign distinct probabilities to those scenarios. A divergence across such probabilities might lead to a misallocation of loans in the decentralized equilibrium. Notably, if private banks assign a lower probability to the transition compared to the central bank, the allocation of loans to more polluting (risky) firms is larger than the central bank’s target.

Against this backdrop, the central bank can counteract the carbon bias in lending activities by imposing differentiated liquidity costs (in the form of cost factors) on banks, depending on the emission intensity of their loans. The bigger the wedge between private banks and the central bank’s beliefs, the higher the liquidity costs imposed on banks issuing loans to risky firms. This in turn worsens the funding conditions of polluting firms, thus constraining their activities and, ultimately, reducing CO2 emissions. Conversely, absent any divergence in beliefs across private banks and the central bank, no intervention is needed.

Under our baseline calibration, if the central bank assigns a 70% probability to the transition against a 50% probability for private banks, the former can align bank lending with its target by adding a cost factor of around 2% to loans to risky firms (Figures 3 and 4). This would make the equilibrium share of loans to less polluting (safe) firms increase from 49.38% to 49.63%. A green credit easing scheme would then be effective in steering lending. However, it might also have implications for financial stability. The higher refinancing costs imposed by the central bank can indeed generate losses on the banks’ balance sheets, which need to be carefully assessed when considering these types of monetary policy operations.

From a practical standpoint, the implementation of a green credit easing scheme poses challenges related to: i) the potential interference with the primary monetary policy mandate; ii) operational issues stemming from the difficulties in evaluating, measuring and verifying the climate impact of banks’ lending. Colesanti Senni at al. (2023) elaborate on these aspects.

While the existing literature reveals a carbon bias in certain monetary policies such as corporate bond purchase programs and collateral policies, the focus on the climate impact of refinancing operations remains relatively understudied. A green TLTRO program presents an opportunity to align monetary policy with a low-carbon transition. We assess the emissions content of loans issued under the ECB’s TLTRO III program and highlight a carbon-intensive trend in lending. Through the lens of a calibrated general equilibrium model, we show that a “green” credit easing scheme can counteract the carbon bias in bank portfolios, steering lending towards less-polluting firms. Our result also spotlights the importance of considering the potential risks for financial stability when designing such a program. Finally, we delve into the operational feasibility of implementing a green TLTRO program by considering various design options and potential challenges. With this exercise, the paper contributes to the ongoing debate on green monetary policy tools by offering a formal analysis that elaborates on some of the mechanisms underlying a prospective green TLTRO. The findings underscore the potential for central banks to play a role in supporting the transition to a low-carbon future.

Afonso, A. and Sousa-Leite, J. “The transmission of unconventional monetary policy to bank credit supply: evidence from the TLTRO”. The Manchester School, 88:151–171, 2020.

Andreeva, D. C. and Garcia-Posada, M. “The impact of the ECB’s targeted long-term refinancing operations on banks’ lending policies: The role of competition”. Journal of Banking & Finance, 122:105992, 2021.

Barbiero, F., Burlon, L., Dimou, M., Toczynski, J., 2022. “Targeted monetary policy, dual rates and bank risk taking,” Working Paper Series 2682, European Central Bank.

Batsaikhan, U. and Jourdan, S. “Money looking for a home”. Positive Money Europe, 2021.

Benetton, M. and Fantino, D. “Targeted monetary policy and bank lending behavior”. Journal of Financial Economics, 142(1):404–429, 2021.

Böser, F. and Colesanti Senni, C. “CAROs: Climate risk-adjusted refinancing operations”. Available at SSRN 3985230, 2021.

Colesanti Senni, C., Pagliari, M.S., van ‘t Klooster, J., 2023. “The CO2 content of the TLTRO III scheme and its greening,” Working Papers 792, DNB.

Da Silva, E., Grossmann-Wirth, V., Nguyen, B., and Vari, M. “Paying Banks to Lend? Evidence from the Eurosystem’s TLTRO and the Euro Area Credit Registry”. Banque de France Working paper, (848), 2021

Diluiso, F., Annicchiarico, B., Kalkuhl, M., and Minx, J. C. “Climate actions and macro-financial stability: The role of central banks”. Journal of Environmental Economics and Management, 110:102548, 2021

Giovanardi, F., Kaldorf, M., Radke, L., Wicknig, F., “The preferential treatment of green bonds,” Review of Economic Dynamics, 2023

Matikainen, S., Campiglio, E., and Zenghelis, D. “The climate impact of quantitative easing”. Policy Paper, Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science, 36, 2017.

Monnet, E. and van ‘t Klooster, J. “Using green credit policy to bring down inflation: what central bankers can learn from history”. The INSPIRE Sustainable Central Banking Toolbox, Policy Briefing Paper no 13., 2023.

Oehmke, M. and Opp, M. “Green capital requirements”. Swedish House of Finance Research Paper, (16), 2021

Oustry, A., Erkan, B., Svartzman, R., and Weber, P.-F. “Climate-related risks and central banks’ collateral policy: A methodological experiment”. Banque de France Working Paper, (790), 2020

Van ’t Klooster, J. and van Tilburg, R. “Targeting a sustainable recovery with green tltros”. Sustainable Finance Lab Positive Money Europe, 2020.

https://www.ecb.europa.eu/press/key/date/2023/html/ecb.sp231122~e12db02da3.en.html.

See “Macron lists France’s priorities for tackling climate change at COP28,” by P. Mouterde, Le Monde, 3 December 2023.