Low or even negative interest rates make speculative investments into riskier asset classes, such as equity and bonds, more attractive as they do not only boost the excess returns but also dampen the volatility of those riskier assets. This has important implications for financial market dynamics and ultimately for financial stability: investors tend to crowd in riskier asset positions during times of low rates and low volatility, including by means of cheap leverage. However, when adverse shocks and higher volatility hit financial markets, those riskier positions may need to be unwound sharply. Such dynamics may further raise the selling pressure on riskier assets and market volatility, thereby reinforcing the initial sell-off. This Policy Brief formalises these stylised facts about the interplay between risk-free interest rates and volatility in riskier asset classes inter alia by replicating the likely shifts in portfolios following popular investment strategies (namely Markowitz or Risk Parity portfolios) during the Covid crisis in financial markets in March 2020.

This Policy Brief summarises our ECB working paper1 which is organised in three parts.

First, we provide empirical evidence of a positive relationship between risk-free interest rates and volatility: lower or negative rates tend to coincide with lower price volatility across equity and bond markets, and vice versa. This finding is consistent with the well-known “volatility smile”, that is: the empirical regularity that volatility tends to be lower when asset prices appreciate as typically is the case when risk-free interest rates are lower.2

Second, we study the implications of low interest rates for financial stability from the perspective of investors that seek an optimal balance between risk and return in portfolios with one risk-free and several riskier assets, known as Markowitz or risk parity portfolios. We do so by gauging the extent to which they build-up risky asset positions in their portfolios, including through taking on leverage, during calm periods and the extent to which they subsequently re-allocate away from riskier assets into cash in the event of higher volatility. We propose a quantitative measure of portfolio instability that gauges the rebalancing flows from risky to risk-free assets in investor portfolios that would be needed to return portfolios to an optimal balance in response to standardized volatility shocks. We then compare that portfolio instability measure for different assumptions on the level of the risk-free interest rate. And, as expected, portfolio instability rises for lower levels of risk-free interest rates, with the share of risky assets which would have to be sold to an increasing amount when an external shock worsens their risk-return profile and vice versa for higher levels of risk-free interest rates.

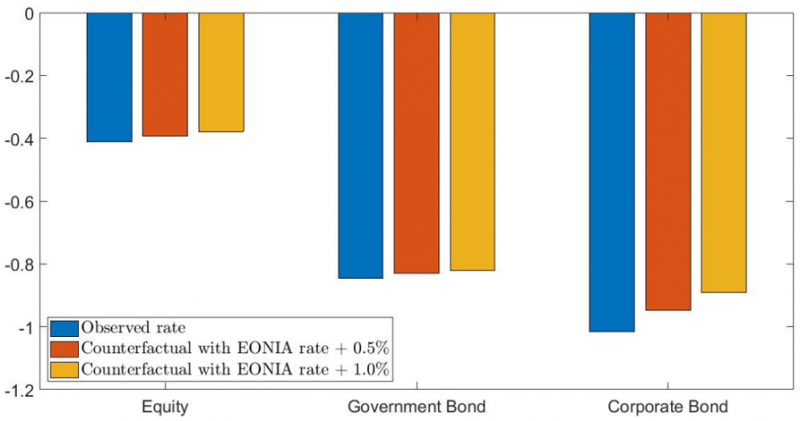

Third, we investigate the economic significance of the amplifying effect of low risk-free rates in a market sell-off in the semi-natural experiment posed by the initial Covid-related turmoil in financial markets in February and March 2020. Specifically, we replicate the portfolio shifts in Markowitz and risk parity portfolios with multiple assets, that were likely incurred by Covid turmoil. We use historical benchmark prices of representative asset classes in the euro area and the US (equity, government and corporate bonds) as well as the corresponding risk-free rates. Consistent with the theoretical presumptions, the simulated optimal portfolios feature large initial leveraged positions across all risky asset classes before the onset of the market stress. Conversely, large outflows from all riskier positions – amounting to multiples of the invested capital – were needed to re-optimise the portfolio when the Covid shock hit (see blue bars in Chart 1). Finally, in counterfactual scenarios with higher initial levels of interest rates, initial leverage ratios and subsequent sales of riskier assets would have been significantly smaller (see red and yellow bars in Chart 1). That is, the magnitude of the effects is inversely related to the interest rate level, implying that portfolio instability in such portfolios increases disproportionately as interest rate approach the effective lower bound of interest rates.

We conclude that low risk-free interest rates provide incentives for high levels of risk-taking by leveraged investment funds, in particular, by raising the excess return and lowering the volatility of riskier asset classes. Under more volatile market conditions, large positions in these assets have to be unwound suddenly to preserve an optimal asset allocation, thereby amplifying the selling pressure in financial asset markets. Conversely, current – substantially higher – levels of risk-free rates across the globe may cushion a future market downturn that may occur in response to an economic shock of a similar size and under otherwise similar conditions.

Chart 1: Simulated portfolio flows in optimised risk parity portfolios with three assets between January and March 2020 in the presence of historical and counterfactual risk-free rates

Source: Hermans, Kostka and Vassallo (2023).