Following the adoption in 2015 of the Paris Agreement on climate change and the UN 2030 Agenda for Sustainable Development, the ECB has been urging the credit institutions under its direct supervision to incorporate climate-related and environmental (C&E) risks into their risk management frameworks and decision-making processes. But banks’ progress has been slow, partly due to the lack of reliable climate-related data and standardised climate risk indicators. As part of its supervisory strategy on climate, and in an effort to help bring about comparable, reliable and high-quality climate-related data, the ECB is currently benchmarking banks’ self-assessments on how they are planning to comply with the ECB’s supervisory expectations relating to C&E risk management and disclosures. The overall snapshot shows that most banks are, at best, only partially aligned with the ECB’s expectations, and some are not aligned at all. However, there are certain areas where they have made substantial progress. The ECB recognises that some banks have effectively raised the bar, and those lagging behind should take inspiration from them and follow suit.

Following the adoption in 2015 of the Paris Agreement on climate change and the UN 2030 Agenda for Sustainable Development, governments around the globe have been making progress towards transitioning to low-carbon and more circular economies. The European Green Deal aims to make Europe the first climate-neutral continent by 2050. The financial sector is expected to play a key role, as enshrined in the European Commission’s strategy for financing the transition to a sustainable economy.

In its field of competence, ECB Banking Supervision has been taking steps to encourage the credit institutions under its direct supervision to incorporate climate-related and environmental (C&E) risks into their risk management frameworks and decision-making processes.

But banks’ progress has been slow on this front, partly due to the lack of reliable climate-related data and standardised climate risk indicators. These are crucial for financial institutions, investors and policymakers to be able to assess financial stability risks, properly price and manage C&E risks and take advantage of the opportunities arising from the transition to a low-carbon economy. Given that this is a new topic, data on C&E risks – both externally available and internally produced by banks – have remained patchy and inconsistent across institutions, and this has resulted in underdeveloped risk metrics.

The absence of standardised, comparable data on C&E risks, as well as the need to collect these data, can be likened to the circumstances in which national accounts were developed after the Great Depression in the 1930s.

Back then, governments were also struggling to find an effective solution for a daunting challenge: stabilising an economy that was plummeting at an unprecedented pace. They ultimately understood that finding metrics for gauging economic damage and potential output was crucial to developing effective countercyclical policies and getting a grip on the economy. After experimenting with an array of different tools, the development of national accounts by economists like Kuznets in the United States and Clark in the United Kingdom gave policymakers their first fairly concrete picture of how the economy was doing. The modern concept of gross domestic product was created and applied for the first time. And although it was a faulty measure, as national accounts were not harmonised and data were patchy and incomplete at first, it made it possible to roughly measure economic activity for the first time and thus constituted a fundamental step towards lifting economies out of the Great Depression. So history teaches us that patchy data is a good start. Our societies’ capacity for gathering and processing data, including data on the effects of climate change, has drastically increased in recent decades. As imperfect as those data may be for now, they will enable progress to be made on climate issues, just as patchy national accounts helped governments chart a course out of the Great Depression.

Despite the fact that C&E metrics and tools are still evolving and that, currently, data available in institutions are incomplete, the ECB is convinced that banks already have a wide array of risk management instruments at their disposal that can allow them to start making real progress on the strategic management and disclosure of these types of risks.

In its Guide on climate-related and environmental risks the ECB reiterates that it does not expect C&E risks to be excluded from banks’ risk assessment frameworks just because they are difficult to quantify. Where methodologies are still not final, the ECB expects banks to follow practices proposed by international networks and standard setters and to use plausible assumptions to develop proxies for assessing these risks. Banks should identify the gaps compared with current data and devise a plan to overcome these gaps and tackle data insufficiencies.

The ECB Guide also provides some concrete suggestions for approaches that banks can follow to start incorporating C&E risks into their risk management frameworks using only patchy data1. In addition, a recent report from the Network for Greening the Financial System proposes several other ways in which financial institutions can overcome incomplete data and make better use of their available sources, such as proxies, qualitative approaches and new data tools. In terms of disclosures, the ECB is not prescriptive about C&E metrics or any other specific tools, but it does expect reference methodologies, definitions and criteria to be disclosed.

The ECB is determined to promote the safe and prudent management of C&E risks by European banks and to help bring about consistent, reliable and high-quality climate-related data.

In 2019 and 2020 it identified C&E risks as a key risk driver for the euro area banking system. In November 2020 it published its Guide on climate-related and environmental risks, setting forth its expectation that the banks under its direct supervision take a strategic, forward-looking and comprehensive approach to considering C&E risks (which include the risks of biodiversity loss and pollution, among others2).

Following the publication of this Guide, in 2021 the ECB asked banks to conduct a self-assessment relating to the expectations set out in that Guide and to draw up action plans for how they intend to align their practices with them. The ECB is currently benchmarking the banks’ self-assessments and action plans and will then challenge them as part of ongoing supervision. This supervisory exercise, which covers action plans that encompass €24 trillion of banking assets, will also offer banks a strong incentive to bolster their ability to identify and quantify their exposures to climate risks and their tolerance of these risks.

Next year, the ECB will conduct a full supervisory review of banks’ practices for incorporating climate risks into their risk frameworks, as we gradually roll out a dedicated Supervisory Review and Evaluation Process (SREP) methodology that will eventually influence banks’ supervisory requirements. In addition, in 2022 the ECB will conduct its next supervisory stress test on climate-related risks.

The results of this stress test exercise, will only be reflected in qualitative measures; a possible impact, if any, will be indirect, via the SREP scores on Pillar 2 requirements. At the same time, the ECB has already stressed that qualitative and indirect supervisory measures are merely a stepping stone. Climate-related and environmental risks will start being treated in the same way as any other risk, meaning that they will be reflected in all relevant supervisory requirements in the future. The ECB will continue to develop its supervisory approach to managing and disclosing C&E risks over time, taking into account regulatory developments and evolving practices in the industry and in the supervisory community.

The ECB will continue to develop its supervisory approach to managing and disclosing C&E risks over time, taking into account regulatory developments and evolving practices in the industry and in the supervisory community.

Looking more closely at how banks are doing in terms of managing and reporting on climate risks, the ECB found that almost all banks under its direct supervision have already developed implementation plans for C&E risks, and many have started to progressively improve their practices. This, in and of itself, is good news. However, the overall initial snapshot is rather disappointing. None of the banks under the ECB’s direct supervision meet all its expectations. All banks have several blind spots and may already be exposed to material climate risks. They are all still a long way off meeting the supervisory expectations laid out for them: 90% of reported practices are deemed by the banks themselves to be only partially or not at all aligned with the ECB’s supervisory expectations. Against this backdrop, the ECB has stressed the importance of all banks making serious efforts to catch up.

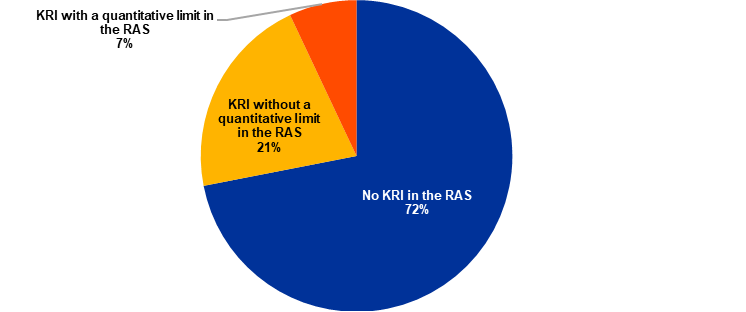

More than half of the banks we directly supervise have no approach whatsoever for assessing the impact of climate risks. This finding is made all the more striking by the fact that, of the 20% of banks that do have a systematic approach to assessing climate risks, almost all find that climate risks are already having, or are about to have, a material impact on their risk profile. Of the banks that did deem C&E risks material in the short term, only a quarter have actually developed risk indicators to manage them, and a mere 7% have C&E risk limits in place (Figure 1).

Figure 1. Does the institution include C&E key risk indicators in its risk appetite framework?

Source: ECB preliminary benchmarking of banks’ self-assessments of C&E risk management and disclosures.

On top of this, only around 40% of banks have assigned explicit responsibility for managing climate risks to the management body – and of those, three in four do not report on climate risks to management. Management bodies that are unaware of C&E risks are effectively prevented from managing them.

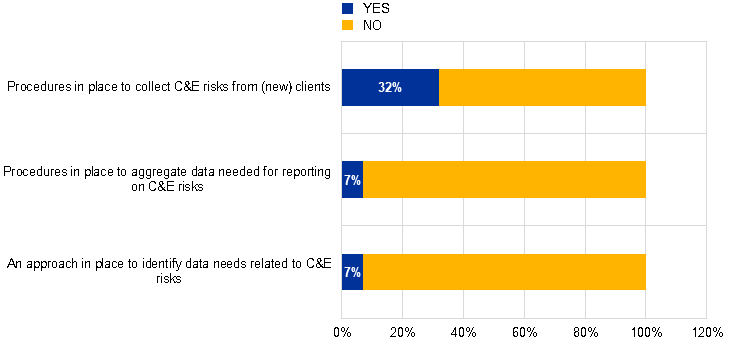

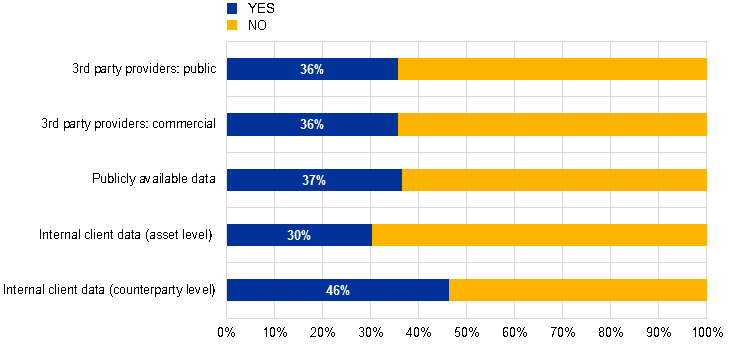

In addition, roughly only one-third of banks have procedures in place to collect new data on C&E risks from their clients. Similarly, most banks are not using publicly available data or data from third-party providers to measure C&E risks (Figure 2). This seems to indicate that banks are not taking a sufficiently proactive approach to collecting the data required to identify and measure the risks, and not making sufficient use of already available data to understand and measure the risks they are facing (Figure 3).

Figure 2. Share of banks under the ECB’s direct supervision that have practices in place to identify and collect data on C&E risks

Source: ECB preliminary benchmarking of banks’ self-assessments of C&E risk management and disclosures.

Figure 3. What kind of data do banks use to measure C&E risks?

Source: ECB preliminary benchmarking of banks’ self-assessments of C&E risk management and disclosures.

A key focus of the ECB’s benchmarking of banks’ self-assessment is ensuring that all banks understand that they need to harness all currently available information on climate risks and start assessing the materiality of the climate risks they are facing. At the same time, the ECB will also be monitoring banks’ entire risk management framework and how their structures are allowing them to more actively manage and disclose C&E risks.

The inertia shown by a number of banks on climate issues also serves as a clear reminder to the supervisory authorities that the soundness of the global financial system also hinges on them holding banks accountable for how they manage climate risk. We should be expanding our capacity and expertise to deal with climate topics, and we should be shining a light on good practices around the globe.

The overall snapshot is not what we would have hoped for, especially given the fact that C&E risks are already starting to materialise for many financial institutions – the May 2021 edition of the ECB’s Financial Stability Review suggests that around 80% of European banks are already exposed to climate-related physical risks. But it’s not all bad news.

There are some areas where banks have made substantial progress. For instance, roughly half of them have started to integrate climate risks into their client due diligence. They have developed dedicated client questionnaires to better understand the climate risks to which they are exposed, and they use this information when deciding to whom they grant credit. In addition, roughly half of banks are now integrating climate risks into their lending policies, sometimes requiring that a specialised climate-related risk function advises them on higher-risk transactions.

What is remarkable is that the progress we are seeing on all these fronts was identified in banks from different countries, with different business models and different asset volumes.

Some banks have also been proactively trying to overcome the scarcity of climate-related data by independently developing their own indicators – such as financed carbon emissions, financed technology mix and energy performance certificates – to identify corporate clients with high sensitivity to climate transition risks. They have then set limits at portfolio level to manage those risks. And one bank has developed a climate risk dashboard to present to its Board’s risk committee on a quarterly basis. This shows that data scarcity can be overcome.

Finally, some banks have already started to identify and manage other environmental risks beyond climate, such as those associated with biodiversity loss and pollution. For instance, one bank has started to develop a methodology to measure the biodiversity footprint of its investment and lending portfolios, while others have developed a dedicated group policy regarding their commitments and lending criteria related to biodiversity risks. In our Guide, we recognise that other environmental factors related to the loss of ecosystem services, such as water stress, biodiversity loss and resource scarcity, have also been shown to drive financial risk. And we therefore expect banks to evaluate all environmental risk-related information, beyond merely climate risks, to ensure that their risk profile is sufficiently covered against them.3

These practices are proof that, contrary to some of the industry’s claims, what the ECB is asking is not unreasonable or impossible. Some banks have effectively raised the bar, and those lagging behind should take inspiration from them and follow suit.

Just as national accounts helped chart a course out of the Great Depression, the accurate mapping of climate risks allows us to navigate the transition to a carbon-neutral economy. For all their many flaws, national accounts data continue to be extremely useful for policymaking to this day. They have been, and will certainly continue to be, extensively reviewed and gradually harmonised – the same path we should expect for climate data and the architecture supporting them. The preliminary results of the self-assessment show that no bank has the full picture on climate risks yet. But the good news is that many pieces of the climate risk puzzle can already be found scattered across the banking union. By following up with supervisory requirements when needed, the ECB will see to it that every bank is making swift progress in embedding climate risks into their organisations. There are risks to acting on the basis of partial data, but in the case of climate change and environmental degradation, the risks of inaction are far greater.

See, for example, Box 8 and Box 10 of the ECB Guide.

In a recent report, 50 of the world’s leading biodiversity and climate experts highlight that climate change and biodiversity loss cannot be managed in isolation from one another. See Pörtner, H.-O., Scholes, R.J. et al. (2021), IPBES-IPCC co-sponsored workshop report on biodiversity and climate change, Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services and Intergovernmental Panel on Climate Change. De Nederlandsche Bank recently examined the material exposures of Dutch financial institutions to risks stemming from biodiversity loss. According to its report, Dutch financial institutions have provided €510 billion in finance worldwide to companies that are highly dependent on ecosystem services, with €28 billion exposed to products that depend on pollination alone. See De Nederlandsche Bank (2020), “Indebted to nature – Exploring biodiversity risks for the Dutch financial sector”, June.

See the Guide on climate-related and environmental risks for more details.