More than 75 central banks around the world are examining whether they should offer central bank money to the public not only as banknotes and coins but also in digital form (Auer et al., 2021). This new form of money is often referred to as central bank digital currency or retail CBDC.

Most central banks, including the ECB, view their work on retail CBDC as a strategic project. It should enable universal access to central bank money in a future in which digital payments are becoming more important, while the payments market could be dominated by new private intermediaries. The design space for retail CBDC spans technical, economic, and legal aspects. Central banks’ projects are driven by administrative prudence and strategic foresight. Issues like the continued universal access to central bank money, control over monetary policy as well as questions of sovereignty take a lot of room in the discussions of central banks and policy makers. Consumers, by contrast, seem often unaware of these debates.

In our study we want to better understand the perspective of potential users. We analyze responses from a survey of 2,006 Austrian residents from the age of 16 onwards that has been conducted in summer 2021. The respondents were asked about their demand for a “digital euro”, and we elicited preferences regarding key features of a retail CBDC, such as the access model (account vs digital token), offline functionality, and the ability to conduct person-to-person payments. Respondents were also asked to rate the importance of attributes, such as payments security and privacy (i. e., data protection).

A special focus of our analysis is to evaluate results across a typology of consumers based on the degree of technology-savviness, the reported ownership of cryptoassets, and the use of payment instruments (cash or non-cash). Tech-savvy consumers and current cryptoasset owners are interesting because they are more likely to be among the first adopters of CBDC. At the other end of the spectrum, cash users are interesting, too: on the one hand, it is well conceivable that they will not have a demand for a (new) digital payment instrument—simply because cash fulfills their needs. On the other hand, CBDC could as well be attractive to cash-affine users in particular if the use of CBDC is convenient, inexpensive, and resolves the concerns that might have stopped them from adopting digital payments offered by the private sector.

Before discussing results, we note that the survey started with a general and simplified explanation of the digital euro. It was explicitly stated that a digital euro would be a complementary offer to cash, and that one digital euro would have the same value as one euro in cash. In addition, respondents were told that digital euro payments would be free of charge, secure, and convenient.

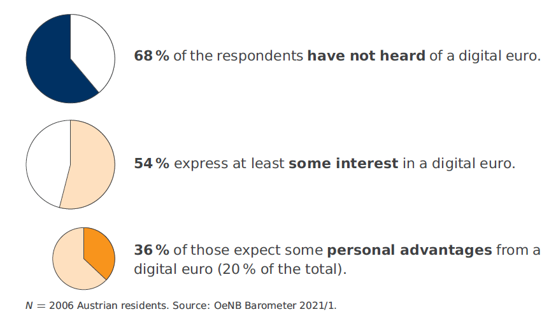

Given the hotness of the CBDC topic in monetary policy circles, it is instructive to see that about two thirds of respondents have not even heard of a “digital euro” before the interview. After having been informed about the basic concepts, about 17% of the sample express an explicit interest in the topic and 37% state that their interest is rather limited. 46% of the sample are not interested at all. Further questions on the digital euro are only posed to those who express at least some interest. We note that the use of this filter is not innocuous: cash-affine and older consumers are considerably underrepresented, while tech-affine and younger consumers are overrepresented in all following analyses. It is important to keep this sample selection in mind.

Figure 1: Respondents’ awareness and interest in a digital euro

In terms of user needs, roughly one third of the respondents expect some advantages for themselves, should a digital euro be available as a payment instrument. Not very surprisingly and in line with the previous surveys of OMFIF (2020) and Bijlsma et al. (2021), the responses show that younger people see more advantages than older ones. Cash-affine respondents are less likely to see an advantage from the digital euro than tech-savvy respondents or cryptoasset owners. The sharp divide between cash-affine users and the others is corroborated by the fact that this user group not only is hesitant about the adoption of a digital euro, but also wants to see an important role for cash in the future.

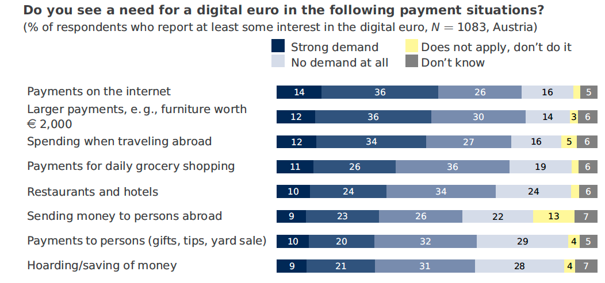

When investigating for which transaction types potential users see a specific need for a digital euro (see Figure 2), the overall picture we obtain is that the need for a digital euro is not pronounced in any transaction type included in the study. Instead, respondents show a high level of satisfaction with the existing payment options. This indicates that at present there is no pressure from users on the central bank to provide a digital euro soon.

Figure 2: Need for a digital euro in selected transaction types

CBDC developers face a number of challenges when choosing specific technical implementations. The decisions often involve trade-offs. Our data allow us to inform this discussion with a perspective from potential users. When confronted with a simplified choice of two options discussed in the literature, users strongly prefer an access model that resembles a bank account rather than a digital token (i.e., a digital equivalent of a bearer instrument that can get lost). This holds across all consumer types – even cryptoasset owners. The data suggest that risk aversion might be a key driver of this preference, which could have been amplified by the chosen question wording emphasizing the risk of losses. Despite the strength of this result, it should be considered tentative and the sensitivity to framing effects should be evaluated in future surveys before deriving design decisions

The question whether a digital euro should be equipped with offline functionality is debated among policy makers. While sometimes justified with better resilience, an offline functionality could also give the digital euro a comparative advantage to most existing forms of electronic payments. The main lesson we can learn from the survey responses is that such a feature is regarded important by the user group we describe as tech-savvy. Cash-affine users, however, express less need for this feature.

When it comes to the opportunity to use the digital euro for direct payments between persons (P2P), it is overall regarded as less important compared to the offline functionality. Among the three consumer types studied, cryptoasset owners are most supportive for a P2P functionality of a digital euro. In summary, although offline and P2P functions could make the digital euro more cash-like, offering these features would not be sufficient to convince cash-intensive users to adopt it.

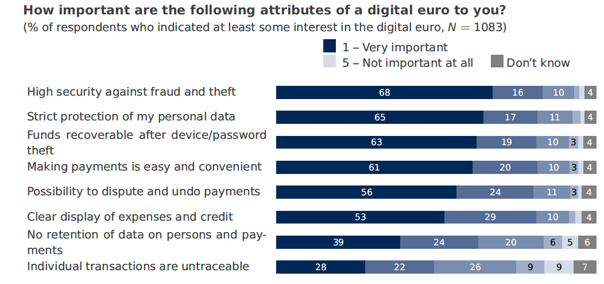

We asked potential users about specific security and privacy concerns (Figure 3). Overall, our respondents seem to attribute more importance to security than to transaction data privacy. This is in some contrast to the findings of the ECB consultation (ECB 2021) but concords with the results in Kantar Public (2022). Note that we stressed in our questionnaire that physical cash will remain available. This could imply that respondents see no need for CBDC to provide privacy in payments.

Figure 3: Reported importance of attributes of a digital euro

While our specific results provide some first guidance for CBDC design, we acknowledge a number of limitations that may impede their validity. First, our survey demanded a lot of imagination from interviewees as we were asking questions on a hypothetical technology of which many respondents knew nothing about. Second and relatedly, the data quality hinges on the instrument design, specifically the wording of questions. For many concepts, we could not draw on established constructs and scales. While we tried to evade all avoidable pitfalls with extensive pretests and are generally confident in the results given their coherence and plausibility, some potential framing effects cannot be fully ruled out. Finally, Austria is a small country with comparatively high cash use. Not all results from Austrian consumers might generalize to more cashless societies or the euro area as a whole.

Despite the methodological challenges, we think that representative surveys among the general public can be very instructive for a more user-centric design approach – not least to assess potential demand for CBDC and to identify early adopters. To be useful, the scope of the data collection should be extended beyond Austria, either to the euro area as a whole or to a selected set of countries with distinct payment conventions. While the current survey instrument can serve as a model, more work is needed, in particular for understanding the robustness of our results with regard to framing effects.

Even if our conclusions are tentative, we believe that CBDC designers should at least be aware how new, how unknown, and how exotic their considerations are to the general public. The development and design of a retail CBDC will need an intensive interaction and dialogue with prospective users. This involves monitoring the effectiveness of communication activities as well as collecting information about prevailing concerns with repeated empirical studies using methods that are robust to selection bias.