Homeownership rates for younger households have been decreasing over time in the United States, the United Kingdom, and several major euro area economies such as Italy and Spain. Understanding the reasons behind these developments is key to study future developments of housing markets and housing prices, the evolution of the income and wealth distributions, and the design of policies. In this policy note I show that increases in labour income inequality and uncertainty are key drivers of the reduction in homeownership rates. Confronted with high house prices and a risky income, many households cannot or do not want to make a big, illiquid, and risky investment like buying a house. However, this also implies that they accumulate less wealth, and might be less able to insure themselves against future shocks.

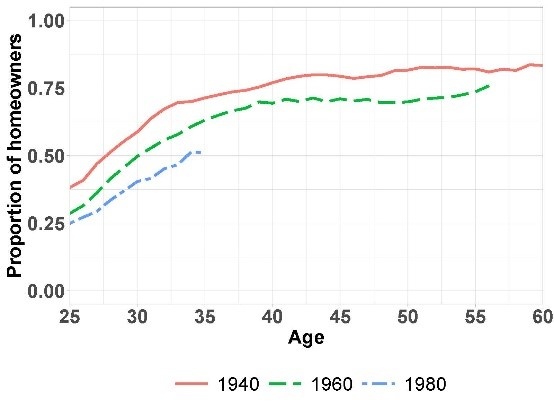

Figure 1. Homeownership rates by age and generation, US data (PSID).

Figure 1 shows the evolution of homeownership rates by age and cohort of birth in the United States. The data shows that 75% of the households whose heads were born in the 1940s were living in their own homes by age 35 (that is, in the late 1970s). This figure was ten percentage points lower for those born in the 1960s, and twenty percentage points lower (55%) within the early ‘Millennials’ born in the 1980s. These distributional changes have occurred in a context in which, remarkably, aggregate homeownership rates have remained relatively stable.

Their primary residence is, for most households, both the largest asset they hold and the majority of their wealth. Thus, changes in homeownership rates have the potential to affect the way they accumulate wealth during their lifetimes.

However, the data also shows that younger households are more likely to participate in the stock market, mostly through indirect means, such as retirement accounts or mutual funds. However, these extra savings in the form of financial wealth do not seem to compensate the missing housing wealth, which implies that the median young household is saving less than the median young household did 20 years ago.

But which are the drivers of these changes? Is it that the economic environment in which these new generations have been born has changed, or is it that they just do not want to buy houses anymore? To gain insights about these questions, it is important to look at developments in the labour market, asset markets, and credit and financial markets.

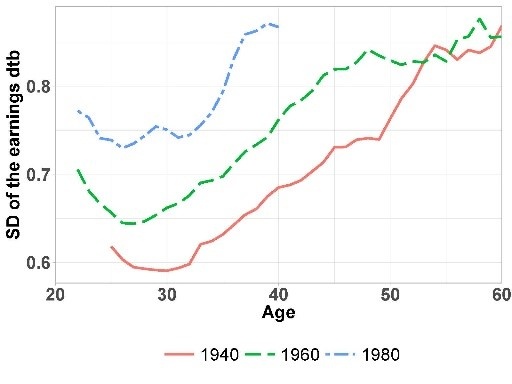

Young households in the United States face a very different labour market than older generations when they were their age. Jobs are more unstable than they used to be, with career-long positions becoming less and less prevalent, and earnings inequality has increased (Figure 2) (Acemoglu and Autor, 2011; Goldin and Katz, 2009). While the labour incomes of high earners have increased substantially over time in real terms, income-poorer individuals have seen their earnings stagnate or decrease.

Figure 2. Measures of earnings inequality (left, standard deviation of the labour market income distribution) and of earnings uncertainty (right, standard deviation of labour market income changes), by age and cohort of birth, US data (PSID).

|

|

The price of the average house with respect to median income has been increasing over time, with very salient cyclical fluctuations. Instead, it doesn’t seem that there have been secular changes in stock market returns.

Credit conditions, and in particular those related with the availability of mortgages, have fluctuated over time. In particular, borrower-based credit constraints such as loan-to-value and loan-to-income restrictions on mortgages became looser in the lead-up to the financial crisis and more stringent afterwards.

The fluctuations over time of credit conditions, house prices, and the business cycle affect different generations differently. For instance, a generation that faces low house prices during their prime homebuying years is more likely to be composed of more homeowners. Even if the original cause is cyclical, the effects can usually be persistent in the long run, given that most households that become homeowners continue to be so throughout most of their lives.

To understand the relative contribution of all of these secular changes to homeownership rates, I build a model of homeownership and portfolio choice over the lifecycle, which features income heterogeneity and risk, business cycle labour market dynamics, and aggregate risk in asset returns (Paz-Pardo, 2021). The purpose of the exercise is twofold. First, the model can generate implied preference parameters (such as tastes for homeownership), which cannot be easily observed in the data, in order to understand whether younger generations just want to buy less houses. Second, I use the model to generate counterfactual scenarios in which I make changes to the aforementioned factors (asset prices, earnings dynamics…) one at a time, so that I can measure their relative contribution to homeownership rates.

The model implies that household preferences with respect to homeownership have not changed substantially over time. Thus, it does not attribute the change in homeownership rates to younger generations not wanting to buy houses anymore because they prefer other consumption goods. Instead, it suggests that it was the different economic environments faced by these different generations that were responsible for their lower homeownership.

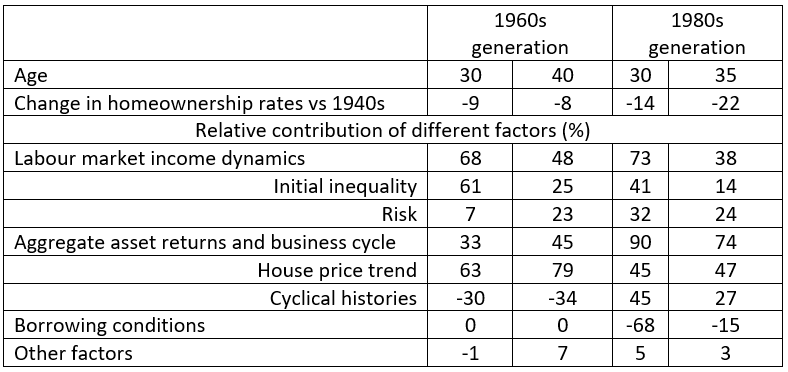

Table 1. Relative contributions to changes in homeownership rates, comparing 1960s and 1980s generations to 1940s generation (baseline)

As Table 1 shows, changes in earnings dynamics explain around half of the decrease in homeownership rates for younger generations. The table compares the homeownership rates of the 1960s and 1980s generations with respect to those in the 1940s, and then decomposes the changes between the different factors that affected these generations. For instance, for the 1960s generation 61% of the reduction in homeownership at age 30 (9 percentage points) is related with higher initial earnings inequality. With labour market income being more unequally distributed, relatively income-poorer households find it harder to buy a house. To explain why that happens, it is key to bear in mind that housing, apart from being illiquid and accruing substantial transaction costs, has a minimum size: there are almost no houses in the market below a minimum price, quality or size threshold. Households whose income and savings are not enough to qualify for a mortgage for that amount are left out of the housing market, even if they wanted to buy.

For the 1980s generation, the role of earnings volatility is also important, as it explains 32% of the drop at age 30. With more unstable income, households are wary of making a large expenditure like a house and assuming a large amount of gross debt; as a result, they stay renters for longer. This insight is in line with other studies for the U.S. such as Fisher and Gervais (2011).

Naturally, the fact that houses have become more expensive over time is also an important explanatory factor of the reduction in homeownership. However, the particular histories faced by each generation also matter. The generation born in the 1960s entered the housing market in a time in which house prices were cyclically low, which partially compensated for the other negative forces that impacted homeownership (thus, the cyclical effect had a positive effect in homeownership of -30% of -9, that is, +3 percentage points). For the generation born in the 1980s, the opposite was true: they started to buy houses at a time where their price was cyclically high, which further discouraged them (45% of the drop at age 30).

However, the particularly lenient financial conditions of the pre-crisis period partially counteracted this effect, as the following rows show. The model suggests that, in the absence of easier borrowing conditions, the homeownership rates for this generation would have been even lower. The model abstracts, though, from potential general equilibrium considerations (absent easier financial conditions, house prices might have been lower).

Households don’t only buy houses as an investment. On the one hand, households might value the housing services of an owner-occupied unit above those of a rented unit, because they can make changes to it, do not need to interact with a landlord, or because they merely enjoy property. On the other hand, owning housing can act as an insurance device against rental price risk. Additionally, homebuying is the only time in which most households incur in substantial leverage: they frequently have only 20% starting equity on their house, which implies that they can accumulate wealth very fast if house prices are on average increasing, as they have been over the past decades.

Figure 3. Wealth accumulation by wealth percentile, 1960s and 1980s generations, US (SCF data). Units are multiples of average income in the economy.

Thus, if younger households are not buying houses anymore because it is harder to get a mortgage, or because they find it harder to bear the risk, it is likely that they will not make up for the missing housing wealth by accumulating an equivalent amount of financial wealth, even in a context in which their labour market income is very unstable. This squares with the predictions of the model, and also with what we observe in the data. As a consequence, the reduction in homeownership rates negatively impacts wealth accumulation for households below median income, which puts upward pressure on wealth inequality and can potentially make it difficult for households to insure themselves later on in life, or have sufficient wealth saved for retirement.

Besides, if households receive direct utility from owning housing, their welfare will be affected by the reduction in homeownership rates. Indeed, homeownership and housing affordability is frequently the focus of expert analysis, political campaigns, or grassroots movements in both the United States and Europe. The change in homeownership rates can also have other political implications, as research has shown that homeowners tend to be more engaged with their local environment, with local politics, and to become more socially attached in general (Rohe, Van Zandt, McCarthy, 2002).

Acemoglu, D., & Autor, D. (2011). Skills, tasks and technologies: Implications for employment and earnings. In Handbook of labor economics (Vol. 4, pp. 1043-1171). Elsevier.

Fisher, J. D., & Gervais, M. (2011). Why has home ownership fallen among the young? International Economic Review, 52(3), 883-912.

Goldin, C. D., & Katz, L. F. (2009). The race between education and technology. Harvard University Press.

Paz-Pardo, Gonzalo (2021). Homeownership and portfolio choice over the generations. ECB working paper No. 2522. Available at https://www.ecb.europa.eu/pub/pdf/scpwps/ecb.wp2522~7ad2cdbbb5.en.pdf

Rohe, W. M., Van Zandt, S., & McCarthy, G. (2002). Home ownership and access to opportunity. Housing Studies, 17(1), 51-61.