References

Bank of England: Central bank digital currencies

https://www.bankofengland.co.uk/research/digital-currencies

last modified March 12, 2020

Bank of England: Central Bank Digital Currency: opportunities, challenges and design

https://www.bankofengland.co.uk/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design-discussion-paper

last modified March 12, 2020

Bank of Japan: Summary of the Report of the Study Group on Legal Issues regarding Central Bank Digital Currency

http://www.boj.or.jp/en/research/wps_rev/lab/lab19e03.htm/

last modified December 24, 2019

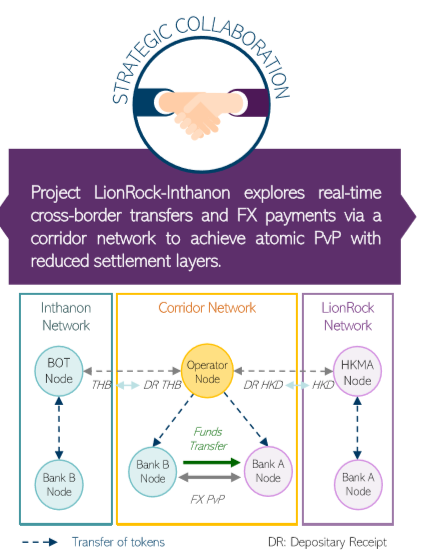

Bank of Thailand: INTHANON Phase I

https://www.bot.or.th/Thai/PaymentSystems/Documents/Inthanon_Phase1_Report.pdf

Banque de France: CENTRAL BANK DIGITAL CURRENCY EXPERIMENTS WITH THE BANQUE DE FRANCE: CALL FOR APPLICATIONS

https://www.banque-france.fr/sites/default/files/media/2020/03/30/fact_sheet_-_central_bank_digital_currency_30_march_2020.pdf

last modified March 30, 2020

BeingCrypto: Swedish Central Bank Outlines 6-Step Digital Currency Plan

https://beincrypto.com/sweden-central-bank-outlines-6-step-digital-currency-plan/

last modified November 22, 2019

Binance Research: First Look: China’s Central Bank Digital Currency

https://research.binance.com/analysis/china-cbdc

last modified August 28, 2019

BIS: The Bahamian Payment System Modernisation: Advancing Financial Inclusion Initiatives

https://www.bis.org/review/r190321a.pdf

last modified March 18, 2019

Bloomberg: Maduro Says Venezuela to Activate Crypto Payment Method ‘Soon’

https://www.bloomberg.com/news/articles/2019-09-30/maduro-says-venezuela-to-activate-crypto-payment-method-soon

last modified September 30, 2019

BNP Paribas: „The NEW Era of Currencies of China: Digital Currency Electronic Payment (DCEP), mimeo

CCN: China Clarifies Digital Currency Launch Rumors but Barely Kills the Hype

https://www.ccn.com/china-digital-currency-rumor-launch/

last modified November 13, 2019

CCN: Hong Kong, Thailand Central Banks Partner up on Digital Currency Initiative

https://www.ccn.com/thursday-hong-kong-thailand-central-banks-partner-digital-currency/

last modified May 16, 2019

Central Bank of the Bahamas: PROJECT SAND DOLLAR, A Bahamas Payments System Modernisation Initiative

https://www.centralbankbahamas.com/download/022598600.pdf

last modified December 24, 2019

Coindesk: Fed Reserve Evaluating Digital Dollar But Benefits Still Unclear, Says Chairman

https://www.coindesk.com/fed-reserve-evaluating-digital-dollar-but-benefits-still-unclear-says-chairman

last modified November 20, 2019

Coindesk: UK Central Bank Chief Sees Digital Currency Displacing US Dollar as Global Reserve

https://www.coindesk.com/bank-of-england-governor-calls-for-digital-currency-replacement-to-the-dollar

last modified August 23, 2019

Cointelegraph: IMF Chief Christine Lagarde: We Should Be Open to Cryptocurrencies

https://cointelegraph.com/news/imf-chief-christine-lagarde-encourages-open-cryptocurrency-regulation

last modified September 4, 2019

Crowdfund Insider: Bank of Korea Official: No Need for a Central Bank Digital Currency in Developed World

https://www.crowdfundinsider.com/2019/10/153590-bank-of-korea-official-no-need-for-a-central-bank-digital-currency-in-developed-world/

last modified October 31, 2019

Crypto World Journal: Blockchain Technology to Be Used by Hong Kong and Thailand to Deploy Tokens for Cross-Border Trade

https://www.cryptoworldjournal.com/blockchain-technology-to-be-used-by-hong-kong-and-thailand-to-deploy-tokens-for-cross-border-trade/

last modified December 12, 2019

European Central Bank: Exploring anonymity in central bank digital currencies

https://www.ecb.europa.eu/paym/intro/publications/pdf/ecb.mipinfocus191217.en.pdf

last modified December 2019

Finextra: ECB Exec: Libra has been a “wake up call” for central bankers

https://www.finextra.com/newsarticle/34424/ecb-exec-libra-has-been-a-wake-up-call-for-central-bankers

last modified September 18, 2019

Fortune: Why China’s Digital Currency Is a ‘Wake-Up Call’ for the U.S.

https://fortune.com/2019/11/01/china-digital-currency-libra-wakeup-call-us/

last modified November 1, 2019

Hong Kong Monetary Authority: Fintech collaboration between Hong Kong Monetary Authority and Bank of Thailand https://www.info.gov.hk/gia/general/201905/14/P2019051400361.htm

last modified May 14, 2019

Monetary Authority of Singapore: Project Ubin: Central Bank Digital Money using Distributed Ledger Technology

https://www.mas.gov.sg/schemes-and-initiatives/Project-Ubin

last modified November 20, 2019

Monetary Authority of Singapore: Project Ubin: SGD on Distributed Ledger

https://www.mas.gov.sg/-/media/MAS/ProjectUbin/Project-Ubin–SGD-on-Distributed-Ledger.pdf

last modified 2017

OECD: China’s Belt and Road Initiative in the Global Trade, Investment and Finance Landscape

https://www.oecd.org/finance/Chinas-Belt-and-Road-Initiative-in-the-global-trade-investment-and-finance-landscape.pdf

last modified 2018

1DECP: DCEP: China’s own digital currency

http://www.1dcep.org/?p=363&lang=en

last modified October 31, 2019

Reuters: ECB should be ’ahead of the curve’ on digital currency: Lagarde

https://www.reuters.com/article/us-ecb-policy-cryptocurrency/ecb-should-be-ahead-of-the-curve-on-digital-currency-lagarde-idUSKBN1YG1SD

last modified December 12, 2019

R3: CAD-coin versus Fedcoin

https://www.r3.com/wp-content/uploads/2017/06/cadcoin-versus-fedcoin_R3.pdf

last modified November 15, 2016

SCMP: Hong Kong, Thailand to roll out two-tier tokens in digital currency prototype to speed up cross-border trade settlement

https://www.scmp.com/business/banking-finance/article/3040582/hong-kong-thailand-roll-out-two-tier-tokens-digital

last modified December 4, 2019

Sveriges Riksbank: E-krona

https://www.riksbank.se/en-gb/payments–cash/e-krona/

last modified December 13, 2019

Sveriges Riksbank: E-krona project, report 2

https://www.riksbank.se/en-gb/payments–cash/e-krona/e-krona-reports/e-krona-project-report-2/

last modified October 2018

The Block: Report: Bank of France to test digital currency in 2020

https://www.theblockcrypto.com/linked/49253/report-bank-of-france-to-test-digital-currency-in-2020

last modified December 4, 2019

The Cryptonomist: China: the launch of the digital currency in 2020

https://en.cryptonomist.ch/2019/11/11/china-launch-of-digital-currency-in-2020/

last modified November 11, 2019

The Federal Reserve: Digital Currencies, Stablecoins, and the Evolving Payments Landscape

https://www.federalreserve.gov/newsevents/speech/brainard20191016a.htm

last modified October 16, 2019

Tokenpost: Bank of Thailand’s DLT-focused Procject Inthanon advances to Phase III

https://tokenpost.com/Bank-of-Thailands-Project-Inthanon-advances-to-Phase-III-2700

last modified July 19, 2019

Worldbank: Distributed Ledger Technology (DLT) and Blockchain

http://documents.worldbank.org/curated/en/177911513714062215/pdf/122140-WP-PUBLIC-Distributed-Ledger-Technology-and-Blockchain-Fintech-Notes.pdf

last modified 2017