References

Andersson, M., K. Musuch, and M. Schiffbauer. 2009. Determinants of inflation and price level differentials across the Euro area countries. ECB Working Paper No. 1129.

Archanskaia, E., N. Plamen, W. Simons, A. Turrini and L. Vogel. 2023. “Corporate vulnerability and the energy crisis”, Quarterly Report of the Euro Area (QREA) Volume 22, Issue 2.

Baba, C, R Duval, T Lan and P Topalova. 2023. The 2020-2022 Inflation Surge Across Europe: A Phillips-Curve-Based Dissection. IMF WP/23/30.

Beck, G. W., K. Hubrich, and M. Marcellino. 2009. Regional inflation dynamics within and across euro area countries and a comparison with the United States. Economic Policy, 24(57), 142-184.

BIS 2022. Inflation: a look under the hood. Annual Economic Report June.

Binici, M., S, Centorrino, S. Cevik, and G. Gwon. 2022. Here Comes the Change: The Role of Global and Domestic Factors in Post-Pandemic Inflation in Europe. IMF Working Papers, 2022(241).

Borio, C and A. Filardo. 2007. Globalisation and inflation: New Cross Country Evidence on the Global Determinants of Global Inflation. BIS Working Paper No. 227.

Borio, C., M Lombardi, J Yetman and E Zakrajšek. 2023. The two-regime view of inflation. BIS WP133.

Buelens, C. 2023a. Googling “Inflation”: What does Internet Search Behaviour Reveal about Household (In)Attention to Inflation and Monetary Policy?, EU Commission Discussion Paper 183.

Buelens, C. 2023b, The great dispersion: euro area inflation differentials in the aftermath of the pandemic and the war, QREA Volume 22, Issue 2.

Cascaldi-Garcia, D., O. Musa, and S. Zina. 2023. Drivers of Post-pandemic Inflation in Selected Advanced Economies and Implications for the Outlook. FEDS Notes. Washington.

Checherita-Westphal, C, N. Leiner-Killinger, T. Schildmann. 2023. Euro area inflation differentials: the role of fiscal policies revisited, ECB WP No 2774 / February 2023.

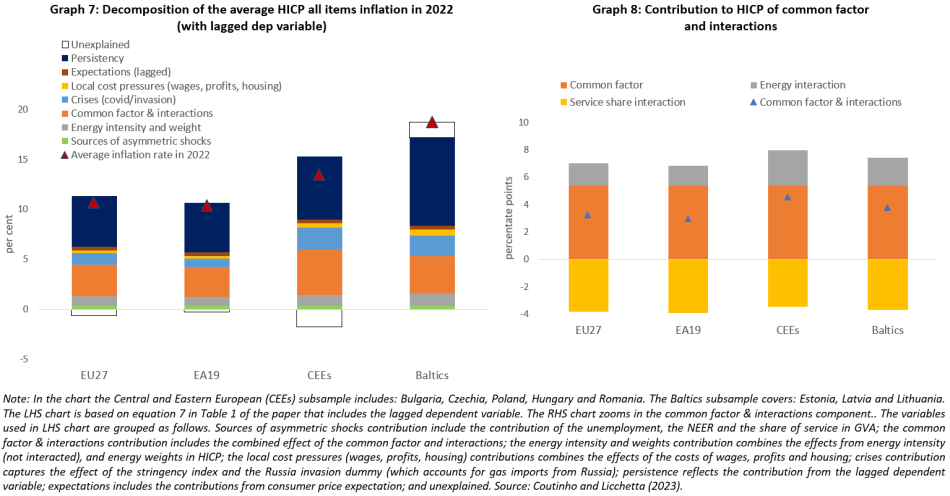

Coutinho, L, and M. Licchetta, Inflation Differentials in the Euro Area at the Time of High Energy Prices, European Economy Discussion Papers 197.

Dao, MD, A Dizioli, C Jackson, PO Gourinchas and D. Leigh. 2023. Unconventional Fiscal Policy in Times of High Inflation. IMF WP 23/178.

Duarte, M and AL Wolman. 2008. Regional inflation in a currency union: fiscal policy vs. fundamentals. Journal of International Economics 74(2): 384–401.

European Commission. 2022. European Economic Forecast – Autumn 2022, European Commission.

Hernnäs H., Å. Johannesson-Lindén, R. Kasdorp and M. Spooner. 2023. “Pass-through in EU electricity and gas markets, Quarterly Report of the Euro Area (QREA) Volume 22, Issue 2.

Honohan, P., and Lane, P. R. 2003. Divergent inflation rates in EMU. Economic Policy, 18(37), 357-394.

IMF. 2023. World Economic Outlook, April.

Tertre, M G. 2023. Structural changes in energy markets and price implications: effects of the recent energy crisis and perspectives of the green transition, paper presented at the ECB Central Banking Forum, 27 June.