Understanding whether companies can adapt to a changing climate is crucial to grasp the lasting economic effects of climate change. This article offers evidence from Italy, illustrating how higher temperatures influence the aggregate dynamics of the corporate sector. Hotter temperatures reduce the number of new businesses entering the market and increase that of businesses shutting down, with firms’ relocation to cooler areas not emerging as a relevant phenomenon. Balance sheet data reveals that temperature effects are profoundly heterogeneous across firms: large, young companies adjust to a hotter weather best, increasing their profits, while old, small ones struggle and persistently suffer from hot temperatures.

At the root of these mechanisms lie the effects of temperatures on human health and economic behavior. During heatwaves, firms’ revenues might decline due to higher absenteeism of workers for health issues, to a fall in productivity in heat-exposed roles or to an increase in production costs. Over longer spans, some companies might successfully adapt – e.g., by means of technological advancements – and thrive in a hotter climate while others might not be able to face this challenge and be, therefore, more likely to exit the market.

Despite their potential to influence market structure, these possibly diverging trajectories have garnered limited scholarly attention. In our recent study (Cascarano et al. 2022), this matter is revisited, examining the long-term repercussions of temperatures on the Italian corporate sector. Two analyses are conducted. First, by employing comprehensive administrative data encompassing the universe of Italian firms, we show how very hot temperatures affect local firm demography – encompassing entry, exit, and relocation – across distinct Italian local labor markets (areas characterized by homogeneous work commuting patterns). Second, we leverage on firm-level balance sheet data to provide some insights into how temperatures could affect the performance of firms exposed to temperature shocks over years.

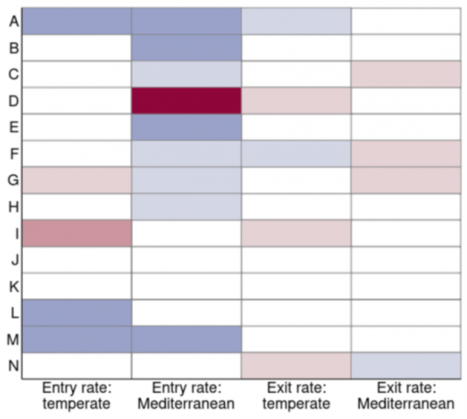

The firm demography analysis draws on the Infocamere dataset, featuring administrative data for an average of over 2 million firms per year (excluding single-person entities) from 2005 to 2019. We investigate how hot temperatures influence the determinants of the growth rate of active firms in local labor markets, namely the entry of new enterprises, the cessation of existing firms, and the relocations of businesses within Italy or abroad. To accurately proxy for heatwaves, we adopt a widely-accepted metric involving the count of days in which maximum temperatures exceed 30°C within a given year, with data sourced from the JRC MARS Meteorological Database. We differentiate the impact of temperatures across two climatic zones: the warmer Mediterranean areas, that predominantly include Italy’s coastal areas, and the cooler temperate regions and, within them, across productive sectors. Recognizing the gradual pace of market dynamics, we conduct our analysis by assessing cumulative temperature effects over three-year temporal intervals.

Figure 1 depicts the results, with red (blue) cells indicating positive (negative) temperature effects, and white cells marking non-significant effects. In the medium term, exceptionally high temperatures induce a decrease in the entry rate of firms and, to a lesser extent a decrease in exit rates within local labor markets. The majority of these effects show up in the Mediterranean region, extending beyond the agricultural sector, whose effects are widespread across the country. The only sector benefiting from elevated temperatures in this zone is the electricity sector, potentially due to augmented demand for air conditioning. Relocation of firms towards more favorable climatic zones plays a marginal role, with temperature impacts proving negligible or insignificant in most instances. Additionally, the absence of a clear sector-level negative correlation of the impacts between Mediterranean and temperate zones implies that other forms of mobility – such as ceasing activity in one place and contextually re-opening in another – are secondary at best in the Italian case.

Figure 1: Effect of extreme temperatures on entry and exit rates across sectors and geographic areas over a 3-year horizon

Notes: red (blue) cells represents positive (negative) effects, with darker cells indicating larger effects in absolute value. Empty cells indicate non-significant estimates at the 95% significance level. The color of the cells is based on the cumulative effect, on entry and exit rates, of a 1% increase in the number of extreme heat days in three consecutive 3-year periods within the local labor market in which each firm resides. Coefficients range from -1.5 percentage points (dark blue) to 1.6 (dark red). The columns of the matrix are labeled by the dependent variable of the regression and the climate zone to which the coefficient estimate is referred. The rows of the matrix indicate the sector according to the Nace Rev. 2 classification: A. Agriculture, Forestry and Fishing; B. Mining and Quarrying; C. Manufacturing; D. Electricity, Gas, Steam and Air Conditioning Supply; E. Water Supply, Sewerage, Waste Management and Remediation Activities; F. Construction; G. Wholesale and Retail Trade, Repair of Motor Vehicles and Motorcycles; H. Transportation and Storage; I. Accommodation and Food Service Activities; J. Information and Communication; K. Financial and Insurance Activities; L. Real Estate Activities; M. Professional, Scientific and Technical Activities; N. Administrative and Support Service Activities.

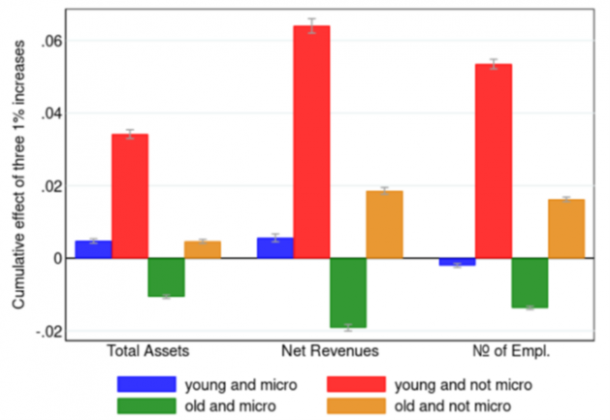

The results, depicted in Figure 2, offer compelling insights. Over the medium term, young, not-micro firms exhibit positive temperature effects, suggesting that healthy, fast-growing firms can adapt to climate change, enhancing profitability. A positive effect, albeit smaller in size, also holds for other sufficiently large firms, even among the older ones. Instead, old, micro firms experience the opposite effects, i.e. a contraction across all the three explored dimensions, underscoring their challenges in adapting by undertaking green or climate adaptation investments (Accetturo et al. 2022).

Figure 2: The effect of extreme temperature events on firm activity, by size and age

In conclusion, these findings suggest that high temperatures are already impacting the corporate sector in terms of both size and composition, with global warming making such threat the more and more material. Elevated temperatures could magnify existing growth disparities between small and large firms, prompting a reshaping of the business sector’s value-added creation dynamics. This dynamic might have important consequences for aggregate productivity growth.

Accetturo, A., G. Barboni, M. Cascarano, E. Garcia-Appendini and M. Tomasi (2022), “Credit supply and green investments”, Available at SSRN 4093925.

Addoum, J.M., D.T. Ng and A. Ortiz-Bobea (2020), “Temperature Shocks and Establishment Sales”, The Review of Financial Studies 33(3): 1331–1366.

Albert, C., P. Bustos and J. Ponticelli (2021), “The Effects of Climate Change on Labor and Capital Reallocation”, NBER Working Paper No. w28995.

Blanchard, O. and J. Tirole (2022), “Major future economic challenges”, VoxEU.org, 21 March.

Cruz, J.L., and E. Rossi-Hansberg (2021), “The economic geography of global warming”, NBER Working Paper No. w28466.

Peri, G. and F. Robert-Nicoud (2021), “On the economic geography of climate change”, VoxEU.org, 11 October.

Cascarano, M., F. Natoli and A. Petrella (2022), “Entry, exit and market structure in a changing climate”, Bank of Italy Working Papers No. 1418.

Pankratz, N. and C. Schiller (2021), “Climate Change and Adaptation in Global Supply-Chain Networks”, in Proceedings of Paris December 2019 Finance Meeting EUROFIDAI-ESSEC, European Corporate Governance Institute–Finance Working Paper.

Somanathan, E., R. Somanathan, A. Sudarshan and M. Tewari (2021), “The Impact of Temperature on Productivity and Labor Supply: Evidence from Indian Manufacturing”, Journal of Political Economy 129(6):1797–1827.

Weder di Mauro, B. (ed.) (2021), Combatting Climate Change: A CEPR Collection, CEPR Press.