References

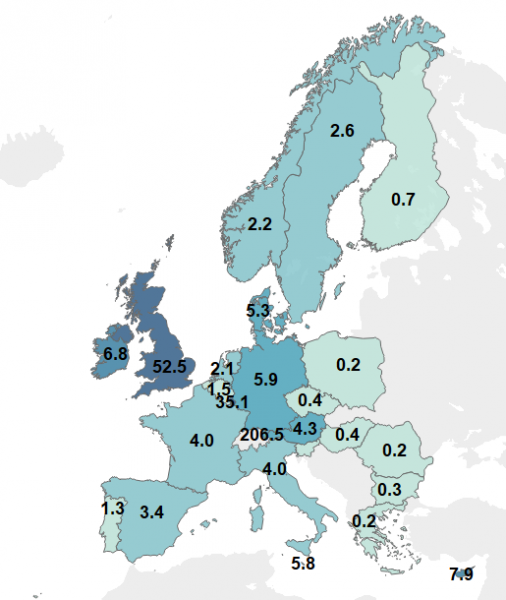

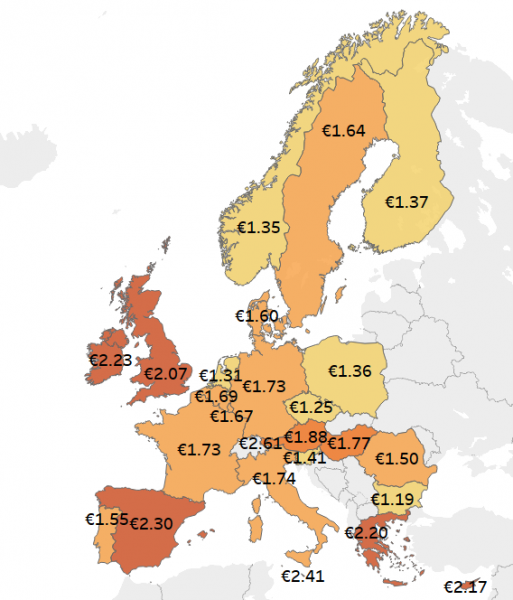

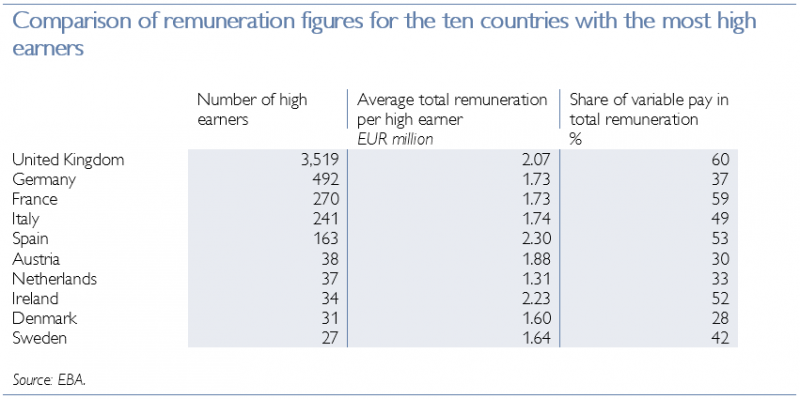

European Banking Authority. 2021. High Earners Reports – data from 2010 to 2019. Available at: https://www.eba.europa.eu/regulation-and-policy/remuneration.

European Banking Authority. 2021. EBA publishes its Report on management and supervision of ESG risks for credit institutions and investment firms. Available at: https://www.eba.europa.eu/eba-publishes-its-report-management-and-supervision-esg-risks-credit-institutions-and-investment.

Sigler, K. J. 2011. CEO compensation and company performance. In: Business and Economics Journal 31(1). 1–8.

Zoghlami, F. 2021. Does CEO compensation matter in boosting firm performance? Evidence from listed French firms. In: Managerial and Decision Economics 42(1). 143–155.

ANNEX

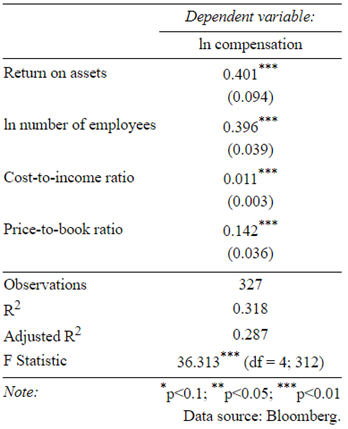

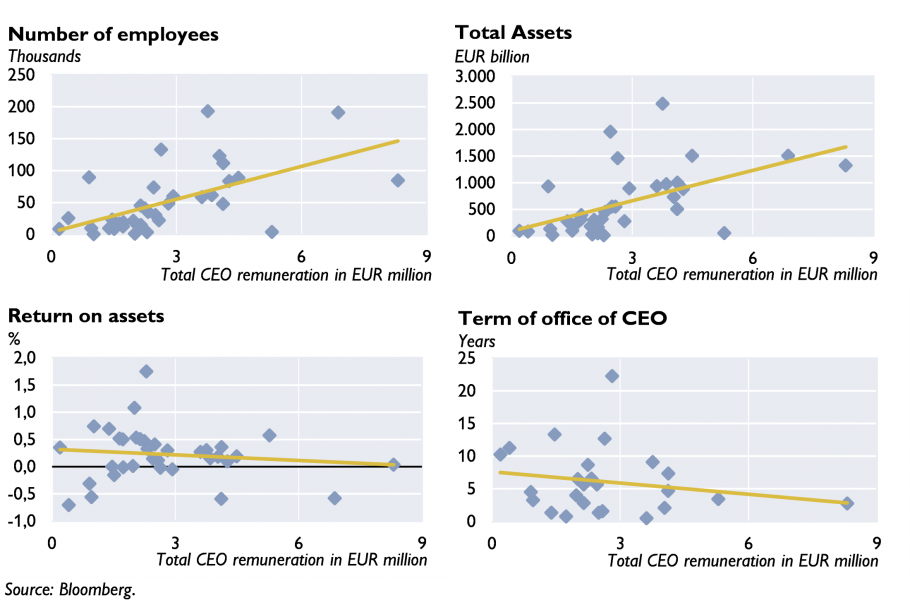

Table 3: Regression results for total CEO remuneration across STOXX Europe 600 banks for the period from 2010 to 20206