References

Bank of Albania (2023), https://www.bankofalbania.org.

Borio, C., L. Gambacorta and B. Hofmann (2015), “The Influence of Monetary Policy on Bank Profitability”, Bank of International Settlements Working Papers No. 514, BIS, Basel.

Dietrich, A and G Wanzenried (2011), “Determinants of bank profitability before and during the crisis: evidence from Switzerland”, Journal of International Financial Markets, Institutions and Money, vol 21, issue 3, pp 307–27.

Rostagno, M., Altavilla, C., Carboni, C., Lemke, W., Motto, R., Saint-Guilhem, A. and Yiangou, J. (2019), “A tale of two decades: the ECB’s monetary policy at 20”, Working Paper Series, No 2346, ECB.

Wang, O. (2020), “Banks, Low Interest Rates, and Monetary Policy Transmission”, Working Paper Series. European Central Bank.

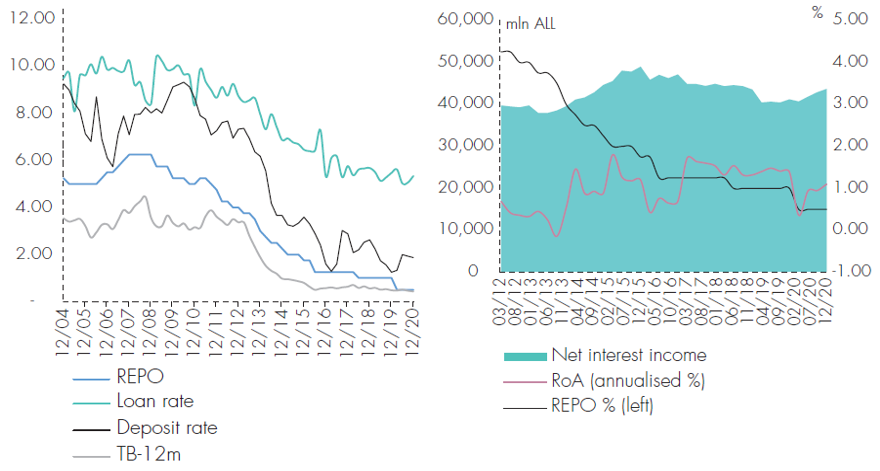

Source: BoA and authors’ calculations.

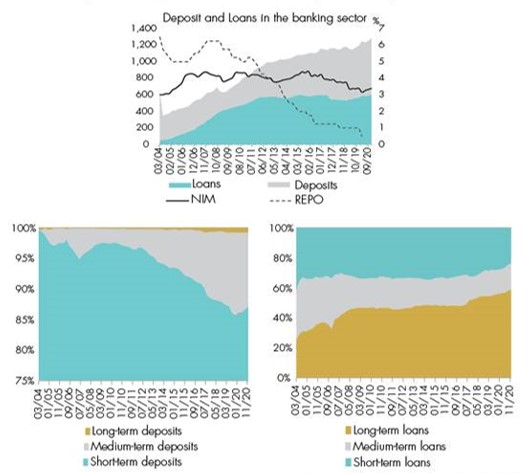

Source: BoA and authors’ calculations. Source: BoA and authors’ calculations.

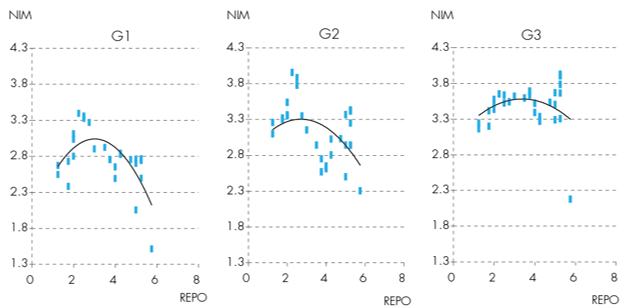

Source: BoA and authors’ calculations. Source: BoA and authors’ calculations.

Source: BoA and authors’ calculations.