This policy brief is based on Central Bank of Ireland Research Technical Paper Vol. 2023, No. 5. These views are those of the authors and do not necessarily reflect the views of the Central Bank of Ireland, the European Central Bank, or of the Organisation for Economic Cooperation and Development (OECD).

Policymakers around the world are encouraging the local production of key inputs to reduce risks from excessive dependencies on foreign suppliers. In a recently published paper, we analyse the macroeconomic effects of supply chain reorientation through localisation policies. We proxy non-tariff measures, such as the stricter enforcement of regulatory standards, which reduce import quantity but do not directly alter costs and prices. Focusing on the euro area, we find that localisation policies are inflationary, imply transition costs and generally have a negative long-run effect on aggregate domestic output. The size (and sign) of the long-run impact depends on whether these policies are implemented unilaterally or induce a retaliation from trade partners, and also the extent to which they reduce domestic competition and productivity. We provide some recommendations for policymakers considering implementing a localisation agenda.

The COVID-19 pandemic and heightened geopolitical tensions from events such as Brexit, US/China trade tensions and the Russian invasion of Ukraine, have increased concerns over the smooth functioning and security of global supply chains. European policymakers, like many others around the world, have introduced legislation to spur the local production of key manufacturing inputs and reduce “excessive dependencies” on external suppliers. These initiatives seek to help Europe achieve Open Strategic Autonomy, one of the key policy objectives of the von der Leyen European Commission.

Despite the potential importance of this issue, our understanding of the macroeconomic effects of supply chain changes resulting from localisation policies is still developing. In Clancy et al. (2024), we simulate a (partial) reshoring of production back to Europe in a global dynamic general equilibrium framework. Our model covers three regions: the euro area (EA), the United States (US) and the rest of the world (RW). These economies are linked through bilateral trade and participation in international financial markets, with region-specific calibration.

We analyse the reshoring of production by (permanently) replacing a proportion of imported inputs used in the creation of export goods with locally produced inputs. Our modelling approach is a proxy for non-tariff measures, such as the stricter enforcement of regulatory standards, which reduce import quantity but do not directly alter costs and prices. A further value added of our framework is that we can analyse the medium-term adjustment process following a decision to reshore. These effects are crucial from a policy perspective, yet are often not analysed in international trade models that only analyse the long-run effects.

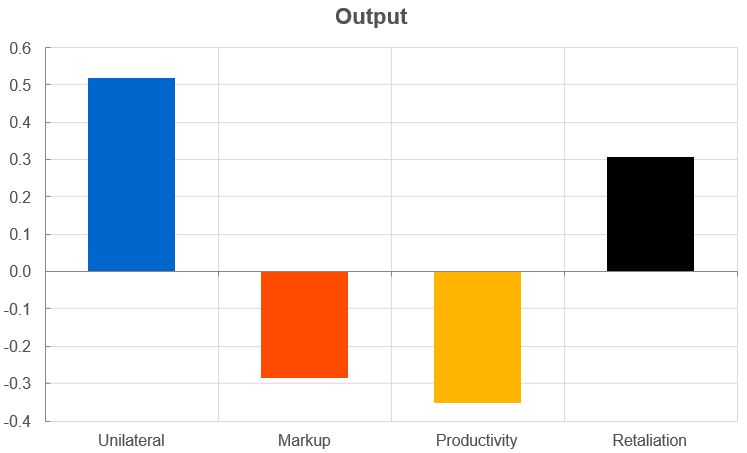

We start by analysing the effects of the EA unilaterally reshoring part of its production. In a basic scenario, there is no impact from reshoring on local competition and productivity and no retaliation by trade partners. All shocks in our analysis are permanent, occur gradually and are almost fully absorbed after 10 years. Reshoring production corresponding to 1% of aggregate output increases euro area output by around 0.5% in the long run (first column of Figure 1). Since reshoring effectively shortens the supply chain, the sum of markups along the chain falls. These cost savings facilitate the expansion in demand in all three regions and are key to our finding of increased aggregate output in this basic scenario.

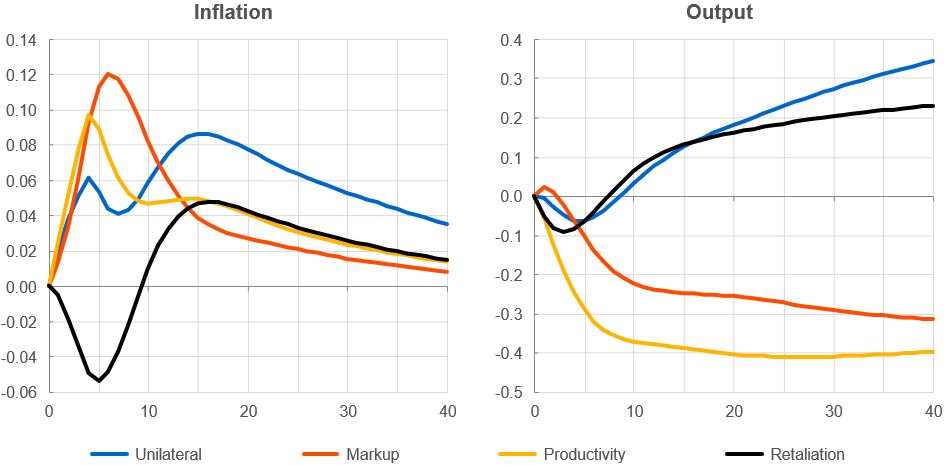

During the adjustment period (blue lines, Figure 2), we find that aggregate economic output is lower and inflation is higher initially. Increased costs and prices result in a (real effective) exchange rate appreciation that worsens external competitiveness and leads to a shift in resources from tradable to non-tradable production. Gradually, as lower import prices feed into lower export prices (through the import content of exports), the effect of the appreciation is fully offset and demand for EA exports rises. This, and the increase in domestic demand for tradable goods (from the decision to reshore), results in a need for greater tradable production and the transition towards the new steady state is set in motion.

However, there are several reasons why reshoring might be less benign for local economic activity. Next, we analyse three such scenarios and find that the size (and sign) of the impact of reshoring on aggregate output depends on the extent to which it results in (i) a (permanent) rise in local firm price markups (from decreased competition), (ii) a fall in local firm productivity (from the use of lower-quality local inputs), and (iii) a retaliation by trade partners.

Figure 1: Long-term effects of reshoring on euro area (% deviation from initial steady state)

Figure 2: Adjustment process in euro area during reshoring (pp and % deviation from initial steady state)

Notes: Figures 1 and 2 show the effect on the euro area (EA) of a permanent increase in EA preferences for domestically produced inputs for export goods (i.e. a partial reshoring of production). We analyse four scenarios: (i) a basic scenario of ‘unilateral’ reshoring, blue; (ii) unilateral plus reduced local competition (‘markup’), red; (iii) unilateral plus reduced local ‘productivity’, yellow; and (iv) a ‘retaliation’ by trade partners, black. The bars in Figure 1 represent the percentage difference between the initial and new steady state level of output. The lines in Figure 2 represent transition dynamics between the initial and new steady state. We scale the shock such that the import content of exports-to-output ratio decreases by 1 percentage point in the long run, with almost all of this adjustment complete after 10 years. Output is in percentage deviations from the initial steady state and (consumer price) inflation is in percentage point deviations.

By signalling a clear increase in preference for local intermediate inputs, localisation policies could (unintentionally) increase the market power of domestic firms in supported sectors and allow them to increase their price markups. We therefore amend our simplified basic scenario to include an additional (permanent) shock to EA tradable-good firms’ market power. In the absence of conclusive evidence of what the size of this increase in market power would likely be, we scale this shock to induce a 0.5 percentage-point increase in tradable-good price markups (from 30% to 30.5%). Given the uncertainty as regards the size of this effect, we emphasise that this is a scenario and is largely for illustrative purposes.

This scenario results in a negative long-run effect on euro area output, as losses from lower competition more than offset gains from bringing production back home (second column of Figure 1). Compared to the basic scenario, the greater market power of tradable firms also allows them to increase their prices by far more. In terms of the adjustment process (red lines, Figure 2), the rise in inflation is much larger than in the basic scenario.

Reshoring could potentially weaken transmission channels through which openness positively affects growth, such as knowledge spillovers, resulting in the use of lower quality locally produced inputs. We therefore amend our simplified unilateral reshoring scenario to include an additional (permanent) shock to tradable-good firms’ productivity. Again, in the absence of definitive evidence of how big this shock might be, we induce a 0.5% decrease in tradable-good productivity for illustrative purposes.

The long-run effect on euro area output is again negative in this scenario (third column of Figure 1). The less efficient use of factor inputs means that the marginal cost of producing tradable goods increases substantially. The adjustment of output is relatively fast (yellow lines, Figure 2). The initial increase in inflation is larger than in the basic scenario, but somewhat weaker compared to the markup scenario.

Our analysis has thus far focused on the case of the euro area unilaterally reshoring production. In reality, such developments would almost certainly induce a retaliation from trade partners. We therefore analyse a symmetric retaliation (i.e. we ensure reshoring of the same quantity of imports in all three regions). As before, these changes occur gradually and take roughly 10 years.1 We display the long-term results in the fourth column of Figure 1.

We find that retaliation reduces the positive long-run effect on the EA output in the basic scenario. As regards the adjustment process (black line, Figure 2), the initial output drop is somewhat larger compared to the basic unilateral scenario. However, the effect on inflation is initially negative before turning positive in the longer run. This temporary disinflationary effect is due to the simultaneous fall in output in all regions on impact.

The Open Strategic Autonomy agenda is rooted in concerns over and beyond economics. However, European policymakers should consider the economic trade-offs related to the implementation of localisation policies and understand the main transmission channels through which these policies affect the economy.

First, to counter the inflationary pressures of reshoring, it is essential to minimise the crowding out of resources (i.e. capital and labour) that pushes up costs and prices in our simulations. This finding calls for limiting the scope of reshoring, such as by focusing on vital goods that are most susceptible to supply chain disruptions. Second, policymakers should avoid excessively weakening Europe’s long-established state aid rules and competition laws, as reduced foreign competition will ultimately undermine the local economy. It could also lead to demands for support in other industries, which are not the focus on reshoring initiatives. Finally, policymakers should focus localisation policies on goods where there is already an existing comparative advantage in production (or, at least, where the distance from the technological frontier is not too large). Either that, or the economic costs are considered a worthwhile trade-off for an increase in security of supply.

Clancy, D., D. Smith and V. Valenta (2024), “The macroeconomic effects of global supply chain reorientation”, International Journal of Central Banking, 20(2): 151-192.

We abstract from analysing potential knock-on effects on local competition and productivity in this scenario, as this would require us making assumptions regarding differential impacts of decreased competition and productivity across the three regions. Even if technically feasible, the imposition of multiple simultaneous region-specific shocks would raise important concerns over interpretation.