Limiting global warming to well below 2°C may pose threats to macroeconomic and financial stability. In an estimated Euro Area New Keynesian model with financial frictions and climate policy, we study the possible perils of a low-carbon transition and evaluate the role of monetary policy and financial regulation. We show that, even for very ambitious climate targets, transition costs are moderate along a timely and gradual mitigation pathway. Inflation volatility strongly increases for disorderly climate policy, demanding a strong monetary response by central banks. In reaction to an adverse financial shock originating in the fossil sector, a green quantitative easing policy can provide an effective stimulus to the economy, but its stabilizing properties do not significantly differ from those of market neutral asset purchase programs. A financial regulation, encouraging the decarbonization of the banks’ balance sheets via ad hoc capital requirements, can significantly reduce the severity of a financial crisis, but prolongs the recovery phase. Our results suggest that the involvement of central banks in climate actions must be carefully designed to be in compliance with their mandate and to avoid unintended trade-offs.

Meeting climate targets requires ambitious climate policies and deep structural transformations of our economies. Any further delay in taking comprehensive and internationally coordinated climate actions will lead to the need for radical future interventions, increasing the macroeconomic costs of the low-carbon transition, as agents will have no time to adapt smoothly to the new policy framework and the new business environment. In addition, the broad spectrum of transition risks, involving both sudden and delayed climate actions, as well as disruptive innovations in the low-carbon sector and sudden changes in market sentiments or in preferences (the so called “Greta Thunberg effect”), could give rise to a sudden devaluation of carbon-related assets, jeopardizing financial stability (NGFS, 2021). Central banks, in line with their mandates and their responsibility for financial regulation and supervision, have started analyzing the potential implications of the green transition for the conduct of monetary policy and the stability of the financial sector.

Our paper (Diluiso et al. 2021) aims at understanding under which circumstances and to what extent ambitious climate actions could be a source of macro-financial instability and what are the implications for price stability and for the conduct of conventional monetary policy in the Euro Area. In addition, the paper studies the potential of green central banks’ instruments in coping with the negative effects triggered by an abrupt devaluation of fossil financial assets, by looking at the stabilizing properties of green quantitative easing programs and differentiated capital requirements (i.e. green-supporting or fossil-penalizing capital requirements). As a laboratory for our analysis, we use a New Keynesian model with financial frictions and three sectors: a good-producing sector and two heterogeneous energy-producing sectors (low-carbon energy and fossil energy).

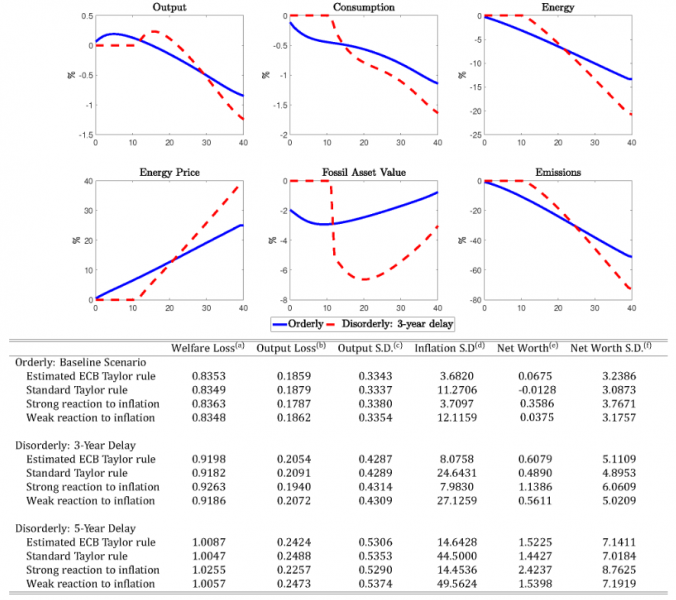

Depending on the nature and speed of the transition policy, climate risks may affect price stability in different ways. In our analysis, we construct two main scenarios: an orderly transition scenario and a disorderly transition scenario. In the orderly scenario a gradually increasing carbon tax is introduced so as to induce a 24% reduction of cumulative emissions over a decade, consistently with the mitigation target envisaged by the European Commission for the period 2020–2030 with the aim of achieving carbon neutrality by 2050 (see EEA, 2021). In the disorderly transition scenarios, instead, we assume that the introduction of the carbon tax is delayed and unanticipated, requiring faster and more disruptive emissions reductions to reach the same mitigation goal of the orderly scenario.

We observe strong effects on the energy market in response to climate policy in both scenarios: the increase in low-carbon energy is not sufficient to overcome the expenditure effects induced by the tax and the total energy demand declines, while the energy price sharply increases. Firms anticipate the future raise in the carbon tax and expand their production in the first periods of the mitigation plan, before starting reducing it as the tax becomes more stringent. Financial markets react to the policy and we observe a decline of the value of fossil energy assets.

Figure 1: Mitigation Scenarios and Monetary Policy

Despite some contractionary effects, overall, an orderly and credible transition is not a source of concern for macro-financial stability. Transition costs are limited along a mitigation pathway, where a growing carbon tax is phased in progressively according to an announced time path. Giving the markets the time to adjust to the mitigation plan is decisive to limit economic costs and to favor a smooth structural change towards a greener economy. In this context, an ambitious climate action has hardly a bearing on price stability, especially when the central bank is strongly committed to keep inflation in check.

By contrast, a delayed climate policy results in higher output and welfare losses and poses a trouble for monetary policy, by raising inflation volatility. Our results show that in a disorderly scenario, negative effects are amplified since agents have less time to react to the policy and to efficiently distribute costs over time. Climate actions, in this context, are much more challenging for price stability than for welfare. Yet, along the transition, a monetary policy targeting inflation more aggressively is able to limit output losses, while securing price stability.

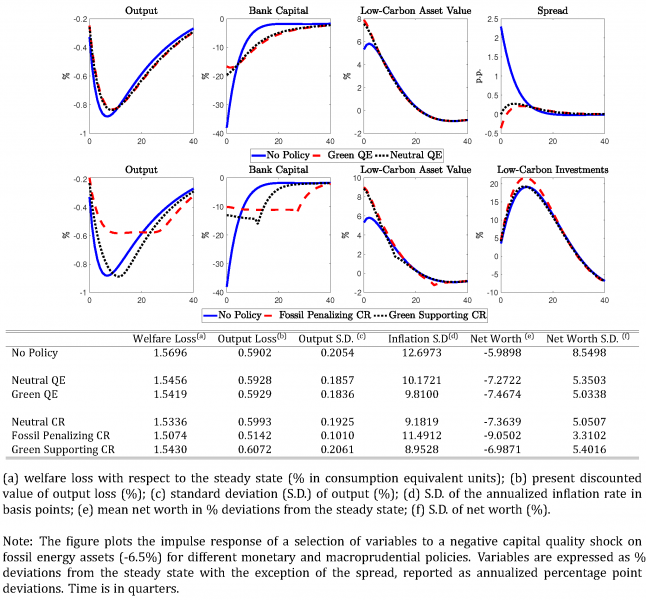

Whether green central banks’ policies are consistent with core central banks’ mandates is a matter of controversy. While green instruments that compensate for low carbon prices represent a direct policy intervention that is beyond central banks’ mandate, the case is less clear for green policy instruments aimed at stabilizing the economy and making the financial system more resilient to shocks. To analyze this issue, we build a scenario entailing a financial shock consisting in a sudden and persistent devaluation of assets in the fossil energy sector and study how different green central banks’ policies can cope with it.

Green quantitative easing, under which the central bank buys exclusively low-carbon energy assets, can stabilize financial markets and mitigate the fall in aggregate demand in the wake of the shock. The asset purchase program relaxes lending conditions, fostering private investment: the spread decreases and the value of assets in the low-carbon sector rises by more compared to the no policy scenario, while the value of assets in other sectors decreases by less. The interplay of these effects sustains bank capital, dampening its decline. Nevertheless, the stabilizing properties of a green quantitative easing are similar to those of market neutral asset purchases, since non-neutral programs reduce yield spreads both for eligible and non-eligible bonds, increasing investments across the overall market. However, according to our results, green quantitative easing programs perform slightly better in reducing output losses and volatility, due to the higher riskiness of low-carbon assets: given the higher initial spread on these assets, the overall absorption of this risk from the banks’ balance sheet by means of the credit policy is slightly higher.

It is worth saying that, considering the, at least currently, modest size of the low-carbon energy sector, stabilizing the economy exclusively through a green quantitative easing would hardly be feasible in case of a major financial distress.

When considering differentiated capital requirements in place when the shock arrives, we find that fossil penalizing capital requirements (increasing the stringency of the regulation for fossil assets), rather than green supporting schemes (relaxing the regulation for low-carbon assets), suggest being a promising stabilization tool. A green supporting scheme does not incentivize the portfolio reallocation toward low-carbon assets and barely prevents the fall in output. The stabilizing effects of a fossil penalizing regulation are stronger as it directly targets assets subject to transition risks. In this case, investments and portfolio reallocation towards other assets’ categories partially dampens the decrease of aggregate demand and production.

As a side effect, we find that fixed capital requirements, in both schemes, reduce the negative impact of a financial shock, but prolong the recovery phase by preventing banks from expanding credit again after a recession.

While both types of capital requirements are welfare improving, green biased schemes lead to higher output losses and volatility, suggesting that, in the case of a substantial relaxation of the credit conditions for low-carbon assets, this regulation may lead to welfare losses. So long as green assets are rated as riskier, less stringent capital requirements for this asset class could undermine macroeconomic stability. On the other hand, inflation volatility is always lower in the regulated regimes, suggesting that a carefully designed macroprudential regulation may be introduced in compliance with the objective of price stability.

Figure 2: Financial Shock, Quantitative Easing (QE), and Capital Requirements (CR)

Diluiso, F., Annicchiarico, B., Kalkuhl, M. and Minx, J.C. (2021). Climate actions and macro-financial stability: The role of central banks. Journal of Environmental Economics and Management, 110, 102548.

EEA, 2021. Greenhouse gas emission targets, trends, and member states MMR projections in the EU, 1990–2050.

NGFS, 2021. NGFS Climate Scenarios for Central Banks and Supervisors. June, NFGS.