We present a new approach to analyse the interconnectedness between a macro-level network and a local-level network. Our methodology is developed on the Diebold and Yilmaz connectedness measure and it considers the presence of entities within a global network which can influence other entities within their own local network but are not relevant enough to influence the entities which do not belong to the same local network. This methodology is then applied to the Maltese domestic investment funds sector and we find that a high-level correlation between the domestic funds can transmit higher spillovers to the local stock exchange index and to the government bond secondary market prices. Moreover, a high correlation among the Maltese domestic investment funds can increase their vulnerability to shocks stemming from financial indices, and therefore, investment funds may potentially become a shock transmission channel.

The analysis of interconnectedness and contagion became an established topic of studies in the academic field by the end of the 1990s. The global financial crisis and the renewed focus on systemic risk and financial stability exposed the weaknesses of the existing methodologies, thus requiring new and more sophisticated methodologies to analyse and assess properly the interlinkages between financial institutions. Two main approaches emerged in the recent years. The first approach follows the seminal work of Allen and Gale (2000) and is based on the identification of the direct linkages between institutions using granular data such as direct exposures through deposits, borrowings and investments in equity shares (Espinosa-Vega and Sole (2010); Covi, Gorpe and Kok (2019); Abad, et al. (2017)). The second approach is based on the use of market data to identify indirect linkages between entities mostly through statistical methodologies, such as vector autoregressive (VAR) models (Diebold and Yilmaz (2009), Billio et al. (2012)).

This brief summarises our paper “A Multi-level Network Approach to Spillovers Analysis: An Application to the Maltese Domestic Investment Funds Sector” (Meglioli & Gauci, 2021). In this study we build on the Diebold and Yilmaz methodology and present a new approach to analyse multi-level networks. In particular, our methodology considers financial entities which, despite belonging to the same global financial network, may form part of different sub-networks in terms of relevance or geographical area. The main novelty of our methodology is that it considers the presence of a ‘macro-level’ network and a ‘local-level’ network. The ‘macro-level’ network is composed of various large indices whose developments influence the whole global network. The ‘local-level’ network is composed of entities whose developments can impact the other entities in the same local network but are not important enough to influence the whole global network.

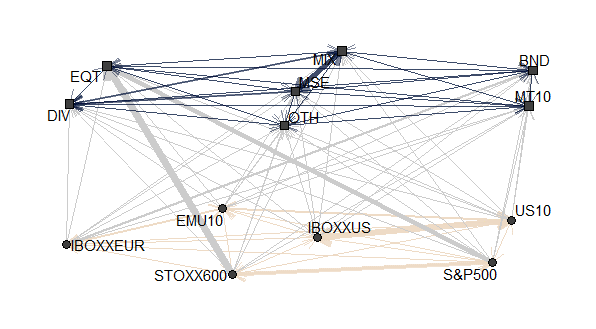

We build a global network composed of a macro network and a local Maltese network to analyse the interconnectedness of the Maltese funds which are considered to have the largest local footprint (“domestic investment funds”). The macro network is comprised of six indices which represent developments in the equity and bond markets in Europe and the US. The local Maltese network consists of the Maltese Equity Total Return Index, the Malta Government Bond 10 Year Yield and five time-series representing the different types of domestic investment funds, namely bond funds, diversified funds, equity funds, mixed funds and other funds. The weekly logged returns of the variables in the global network are taken for the period 1st January 2010 – 3rd January 2020 and the respective realised volatility is computed for each series. Finally, the log of these realised volatilities is considered in order to approximate normality for each of the observations (Andersen, et al., 2003). The resulting fitted static global network is represented in Figure 1.

Figure 1: Multi-level Network

The local network is presented at the top of the figure (blue edges), the macro network at the bottom of the figure (sand edges) and the spillovers from the macro to the local network are illustrated by the grey edges. The bolder the edges are, the higher the spillovers and interconnectedness.

Equity funds appear to be the strategy most vulnerable to external spillovers, in particular to spillovers coming from variables in the macro-level network. Interestingly, for the MSE Equity Total Return Index (MSE), the spillovers received are almost all from within the local network. The main source of external spillover for this variable are the mixed funds (MIX) which represent also the main spillover transmitters within the local network.

Once the global network has been defined, we study the financial stability implications of herding behaviour between Maltese domestic investment funds. The Maltese domestic investment funds industry is potentially susceptible to herding behaviour. One of the main reasons is that a handful of asset management companies are managing all the domestic funds. Therefore, it is likely that during a period of distress, a fund manager would take similar investment decisions across the different fund strategies that it manages. Moreover, due to most of the Maltese domestic investment funds being retail and the limited number of Maltese households, it is likely that managers will try to meet the investment preferences of the same pool of investors, thus adopting the same investment behaviour.

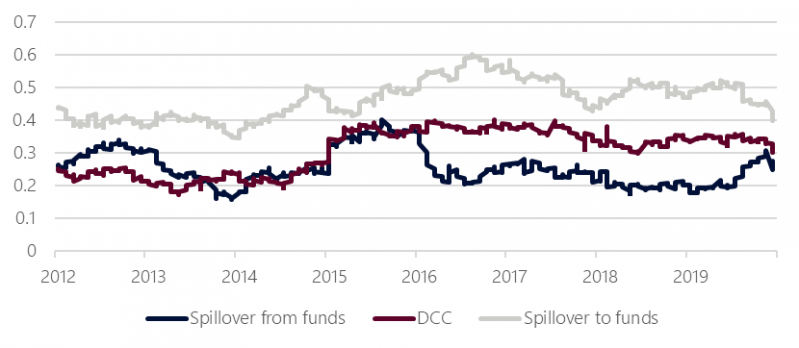

The herding behaviour is proxied by averaging all the pairwise correlations among funds at each point in time. The financial stability implications are analysed by testing the following two hypotheses:

H1: a stronger herding behaviour in the fund industry results in the Maltese equity index and long-term Government yields being more vulnerable to shocks in the funds.

H2: a stronger herding behaviour in the funds industry results in Maltese funds being more vulnerable to external shocks.

Figure 2: Average DCC and spillovers

Adopting two autoregressive distributed lag models (ARDL), we study the short and long-run relationship in the evolution of the herding behaviour and the spillovers in the fund industry. We find that, while a change in the correlation among funds does not have any immediate effect on the spillovers transmission dynamics, a prolonged high correlation among funds could result in a higher amount of spillovers transmitted and received by investment funds. This confirms both the H1 and H2 hypotheses, meaning that when the herding behaviour in the domestic fund industry is stronger, the local financial market is more vulnerable to shocks in the domestic funds, as well as the domestic funds become more vulnerable to shocks in the financial markets.

Abad, J. et al., 2017. Mapping the interconnectedness between EU banks and shadow banking entities. National Bureau of Economic Research.

Allen, F. & Gale, D., 2000. Financial contagion. Journal of political economy, 108(1), pp. 1-33.

Andersen, T. G., Bollerslev, T., Diebold, F. X. & Labys, P., 2003. Modeling and forecasting realized volatility. Econometrics, pp. 579-625.

Billio, M., Getmansky, M., Lo, A. W. & Pelizzon, L., 2012. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics, 104(3), pp. 535-559.

Covi, G., Gorpe, M. Z. & Kok, C., 2019. CoMap: Mapping Contagion in the Euro Area Banking Sector. ECB Working Paper Series, Volume 2224.

Diebold, F. X. & Yilmaz, K., 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal, Volume 119, pp. 158-171.

Espinosa-Vega, M. A. & Sole , J. A., 2010. Cross-Border Financial Surveillance: A Network Perspective. IMF Working Papers.

Meglioli, F. & Gauci, S., 2021. A Multi-level Network Approach to Spillovers Analysis: An Application to the Maltese Domestic Investment Funds Sector. Research Papers in Economics.