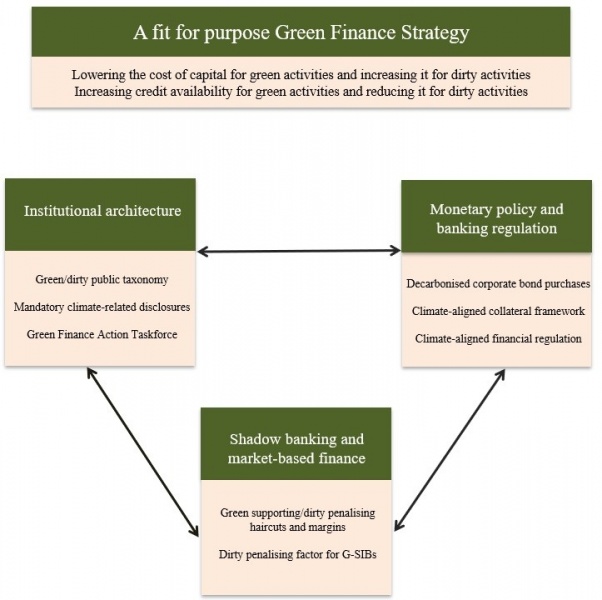

The transition to a low-carbon economy consistent with the 2015 Paris Climate Agreement represents the greatest challenge of our time. It requires structurally re-aligning our financial sector with the challenges and risks posed by climate change. The deregulated and market-oriented approach to greening finance taken by the current UK government will not go far enough. A fit for purpose Green Finance Strategy is needed to address the market failures and systemic financial risks posed by climate change and the transition to a low-carbon economy. This entails getting the UK’s institutional architecture right by developing a green and dirty public taxonomy, making climate-related disclosures mandatory based on such a public taxonomy, and setting up a Green Finance Action Taskforce composed of state actors to oversee the greening of the financial system. It further entails greening monetary policy and banking regulation, by decarbonising corporate bond purchases and the Bank of England’s collateral framework, and aligning risk-weighted capital adequacy rules with the greenness/dirtiness of the assets that banks hold. It would finally entail the decarbonisation of shadow banking and market based-finance. This can be achieved by establishing green-supporting/dirty-penalising haircuts and margins, and implementing a dirty penalising factor for Global Systemically Important Banks (G-SIBs). Fiscal, industrial and environmental regulation policies have a stronger and more substantial role to play in achieving the low-carbon transition quickly. But the urgency of the climate crisis requires that all policy tools are used for the purpose of avoiding a climate breakdown. Our proposals ensure that the UK financial system will support climate economic policies, instead of undermining them.

The UK economy needs to be decarbonised rapidly. This decarbonisation requires the use of a wide range of policies, including green fiscal policies, green industrial policies and environmental regulation policies. However, decarbonisation might not be rapid enough without the green transformation of the UK financial system. The Green Finance Strategy announced by the UK government in July 2019, and further elaborated in November 2020, does not go far enough: it offers a deregulated decarbonisation approach that prioritises the development of green asset classes to increase the competitiveness of the UK financial sector, lacks penalties for dirty activities and is over-reliant on transparency and disclosures.1 A rapid low-carbon transition will not take place via such a market-oriented approach because of a series of market failures that include incompatible time horizons between private finance and the climate crisis, corporate market power that opposes fundamental changes in climate finance and subjective private classifications of green assets that are susceptible to greenwashing.

Figure 1: A fit for purpose Green Finance Strategy: outline of recommendations

Source: Constructed by the authors

A fit for purpose Green Finance Strategy should be more ambitious and should address these market failures using a holistic and more interventionist approach. Such a strategy needs to include (i) the development of a climate-aligned institutional architecture that relies on a public taxonomy of green and dirty activities, (ii) the greening of monetary policy and commercial banks’ balance sheets and (iii) the decarbonisation of shadow banking and market based-finance (see Figure 1).2 We first explain the reasons why the UK financial system should be decarbonised and we then analyse the components of our proposed fit for purpose Green Finance Strategy.

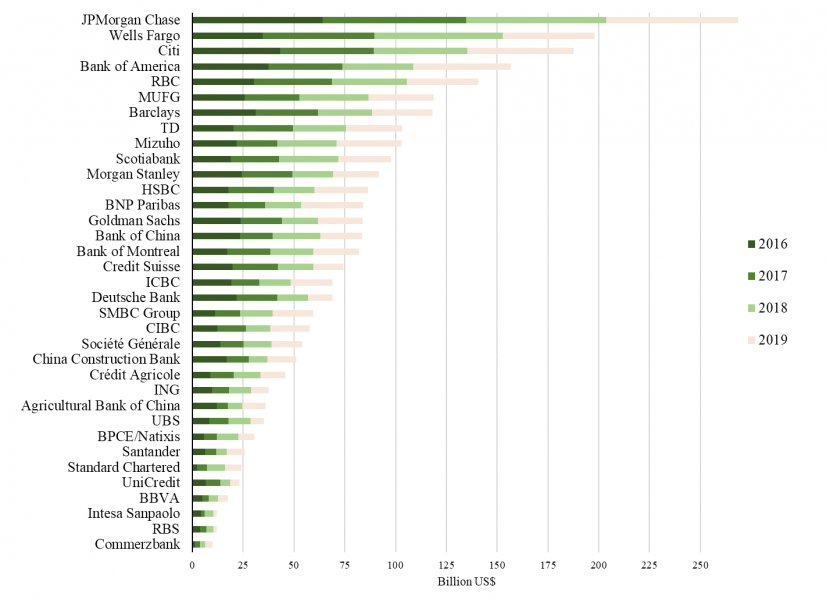

The UK private financial institutions provide a significant amount of financing to carbon-intensive companies. Some of the large UK banks are amongst the top banks worldwide that contribute substantially to the financing of fossil fuel companies (see Figure 2). For example, Barclays and HSBC provided close to $200bn financing to fossil fuels over the period 2016-2019.3

Figure 2: Bank financing of fossil fuels, billion US$, 2016-2019

Source: Rainforest Action Network (RAN), https://www.ran.org/

Note: Fossil fuels include tar sands oil, Arctic oil and gas, fracked oil and gas, liquefied natural gas, ultra coal power and coal mining.

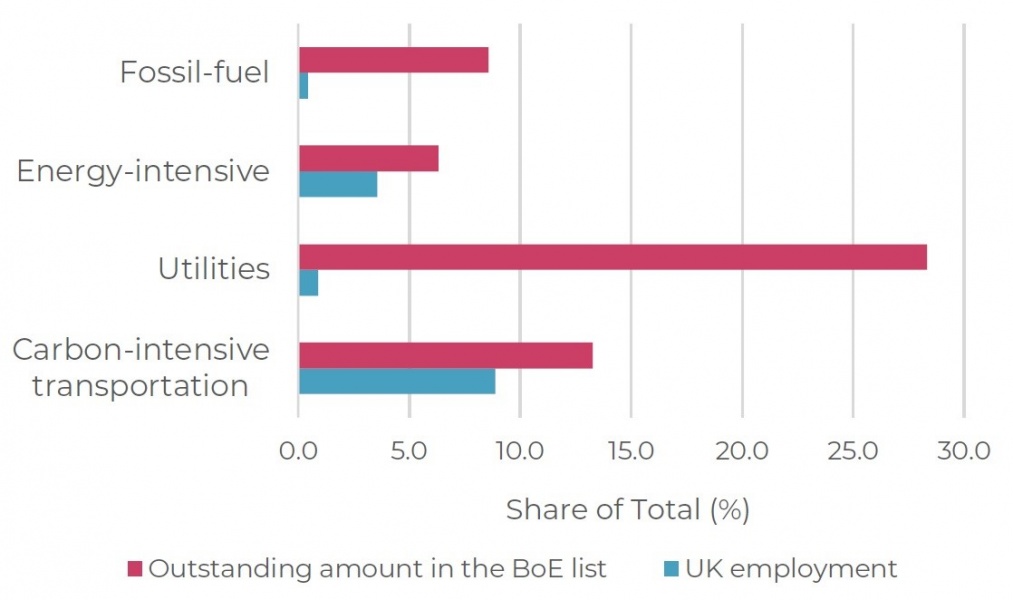

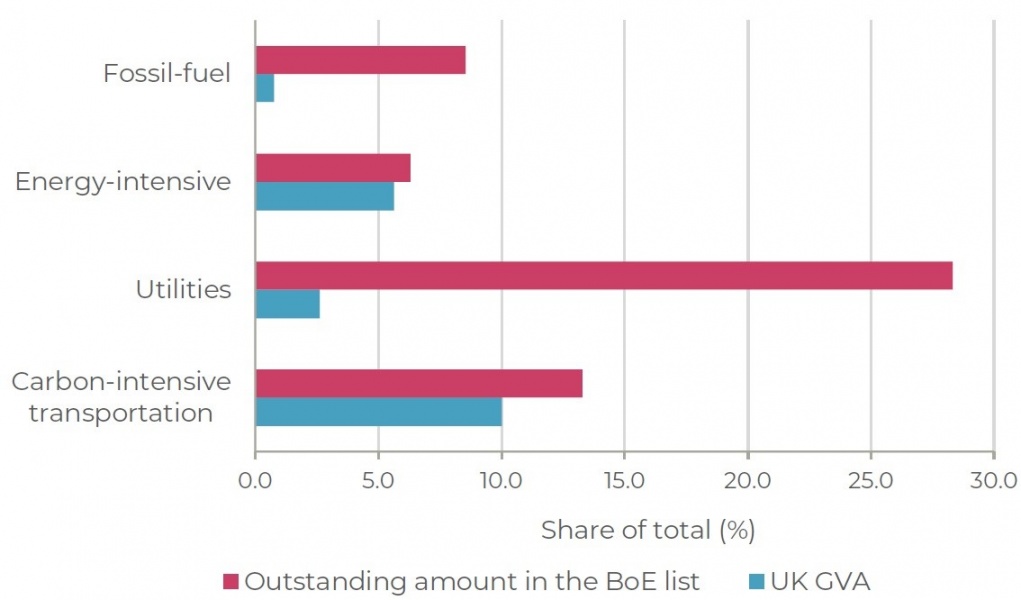

The Bank of England (BoE) also contributes to the generation of greenhouse gas (GHG) emissions through its monetary policy. It has been shown, for example, that the corporate Quantitative Easing (QE) programme that the BoE has implemented since 2016 suffers from a significant carbon bias.4 According to a recent empirical study, 57% of the value of the bonds that are purchasable by the Bank are from the most carbon intensive sectors that only represent 13.8% of overall UK employment and contribute 19% to Gross Value Added (GVA) − a metric used to measure the economic contribution of different sectors (see Figure 3).5

Figure 3: Carbon-intensive sectors in Bank of England (BoE) list of eligible bonds, UK employment and Gross Value Added (GVA)

|

|

Source: Dafermos, Y., Gabor, D., Nikolaidi, M. and van Lerven, F. (2020). “Decarbonising the Bank of England’s pandemic QE: ‘Perfectly sensible’’’, New Economics Foundation, August 2020.

Apart from supporting carbon-intensive activities, the UK financial system is also exposed to climate-related financial risks. There are broadly two types of climate risks that pose threats to financial stability:6

3.1 Developing a green/dirty public taxonomy

A crucial first step for greening private finance is to distinguish between green and dirty economic activities and, consequently, the financial instruments/products linked with these activities. Private taxonomies and metrics such as the Environmental, Social and Governance (ESG) ratings suffer from significant inconsistencies and underlying conflicts of interest, opening the door to greenwashing.7

Instead, a fit for purpose green finance strategy requires a public taxonomy that eschews the lobbying influence of private finance and corporations. The UK government has already announced that it will develop a green taxonomy based on the scientific metrics in the EU taxonomy8, developed by the Technical Expert Group (TEG) on Sustainable Finance9. Importantly, it will further establish a UK Green Technical Advisory Group ‘to ensure they [the EU Taxonomy metrics] are right for the UK market’10. We suggest that the UK government develops its public taxonomy by building on, and addressing the shortcomings in, the EU Taxonomy. The EU Taxonomy identifies a list of economic activities that contribute substantially to six environmental objectives: (1) climate change mitigation; (2) climate change adaptation; (3) sustainable use and protection of sustainable water and marine sources; (4) transition to a circular economy; (5) pollution prevention and control; (6) protection of and restoration of biodiversity and ecosystems. A company activity is Taxonomy-eligible if it belongs to the European Union (EU) Taxonomy list and at the same time (i) does no significant harm to the other five activities of the list; (ii) meets minimum safety standards (related, for instance, to human and labour rights); and (iii) is consistent with specific performance thresholds (such as carbon intensity thresholds), referred to as ‘technical screening criteria’.

However, the EU Taxonomy suffers from limitations that the UK Taxonomy should address. First, the EU Taxonomy does not identify environmentally harmful, or ‘dirty’, activities.11 As a result, it cannot be used to place direct pressure on those companies that undertake such activities and need to be decarbonised rapidly. Second, in the case of climate mitigation activities, the EU Taxonomy adopts a very broad definition of what is ‘green’ by considering as potentially Taxonomy-eligible a large number of activities that currently produce a significant amount of emissions, but are conceived to have the potential to contribute indirectly to the transition to a low-carbon economy (like manufacturing activities and car transport). This opens up the possibility of greenwashing. Third, the EU Taxonomy has adopted a binary approach: an activity can be Taxonomy-eligible or not. This means that activities with very different contributions to the reduction of greenhouse gas emissions are perceived as identical in the taxonomy. It would be more productive to identify activities with different degrees of greenness and dirtiness.

The UK Government could develop a green/dirty taxonomy that does not suffer from these limitations.12 First, in the UK Taxonomy green activities should be defined in a way that minimises the risk of greenwashing. For instance, the list of climate mitigation activities should include only those activities that are already low-carbon or enable low-carbon investments. This would set a stricter threshold on what is green and what is not, compared to what is the case in the EU Taxonomy. Second, the taxonomy should define degrees of greenness. A way of doing so would be to rely on the amount of emissions that are avoided through the corresponding activity: the higher the amount of avoided emissions, the higher the degree of greenness. Undoubtedly, this approach faces data challenges. But data availability on this issue is continually improving and identifying degrees of greenness would allow policy makers to support more actively those activities that can have a higher contribution to the transition to a net zero emissions economy. Third, the non-green activities should be assigned a degree of dirtiness, by relying, for instance, on some metrics like those used for the EU Taxonomy performance thresholds. Policy makers could use the degree of dirtiness in order to penalise more those activities that have a more adverse environmental impact.13

3.2 Mandatory climate-related financial disclosures

The disclosure of climate-related information should be mandatory for all institutions that engage in financial activities. Financial and non-financial corporations should disclose the degree of greenness and dirtiness of their financial assets, using the UK Public Taxonomy.

This can be accompanied by disclosures that are aligned with the recommendations of the Task Force on Climate-related Disclosures (TCFD).14 However, TCFD disclosures cannot replace disclosures about the greenness and dirtiness of their assets. The TCFD recommendations refer to information about the governance and strategies around climate-related risks and opportunities, as well as to risk management processes, metrics and targets. Disclosing information on these issues is useful, but does not ensure the availability of clear information on how green and dirty the activities and financial assets of corporations are. TCFD also gives too much flexibility to corporations on how to report information on climate-related risks and opportunities. This makes it difficult to make consistent comparisons between companies and can delay more decisive climate actions. The UK government has recently committed to make TCFD disclosures mandatory by 2025.15 Although this is welcome step, it cannot replace the more urgent need for UK Taxonomy-aligned disclosures.

3.3 Setting up the Green Finance Action Taskforce (GFAT)

The UK’s macro-institutional framework was not originally designed, and is therefore ill equipped, to deal with climate change. To address this institutional mismatch, we propose the establishment of the Green Finance Action Taskforce (GFAT). The GFAT will closely oversee progress in greening private finance, including the development of the Public Taxonomy, will monitor the green finance gap, will take actions to tackle transition risks and will respond to obstacles that stand in the way of reorienting private finance towards green activities. The GFAT will also ensure the coordination of green finance policies with other climate policies (fiscal, industrial and regulatory) such that the reduction of emissions will be maximised and the economic disruptions caused by decarbonisation will be minimal.16

The Bank of England has taken action that is conducive to making the UK financial system more climate-aligned. For example, in June 2020 it published a report on its own climate-related financial disclosures with the purpose of creating a benchmark that can encourage the adoption of TCFD disclosures by the private sector.17 It has also planned to conduct climate stress tests in 2021, which is an important step for making the UK financial system more climate-aligned.18

However, the Bank of England can contribute to the decarbonisation of the UK economy and financial system much more directly by adjusting its monetary and prudential policies.19 The implementation of such policies does not necessarily require the change of the Bank’s mandate. Any reduction in carbon emissions that can be caused by the policies of the Bank will be conducive to the reduction of the physical risks of climate change that threaten financial stability. Therefore, a broader interpretation of its existing mandate about financial stability would potentially suffice to justify the active use of central bank tools for the decarbonisation of the UK economy. However, the UK government could also consider to explicitly include environmental sustainability in the mandate of the Bank of England. This would permit a more pro-active use of central bank tools for facilitating the transition to a low-carbon economy and would fully align the operations of the Bank with the Paris Climate Agreement (which the Bank is party to).

4.1 Decarbonising monetary policy

One important central bank tool is the Corporate Bond Purchase Scheme (CBPS), which has recently been expanded because of the COVID-19 crisis. Corporate bond purchases are intended to increase demand for bonds and therefore reduce their yields. This in turn is intended to lower the cost of borrowing, encouraging an increase in investment and spending to help bring inflation to target.

The Bank’s corporate bond purchases, however, are heavily biased towards the most carbon-intensive sectors, whilst not reflecting climate-related financial risks (see Section 2). Because the Bank’s purchase lowers bond yields of those companies that are eligible under the scheme a likely unintended repercussion of corporate QE is to lower cost of borrowing and encourage more debt issued by the most carbon-intensive firms relative to low-carbon firms. In effect, the most carbon-intensive companies are potentially indirectly subsidised by the Bank.

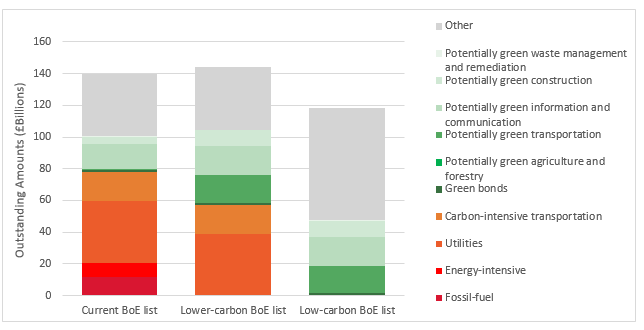

To help the Bank align its purchases with national and international climate objectives and support a green recovery, Dafermos et al. (2020) offer a 2 pronged framework that would reduce the carbon impact of the CBPS (see Figure 4). In the first ‘Lower-carbon BoE list’ scenario, the dirtiest bonds, such as those issued by fossil-fuel sectors, are excluded from the list of bonds that are eligible for purchases. These are replaced with bonds that can be conducive to a greener economy while still meeting the Bank’s key eligibility criteria. In the second, ‘Low-carbon BoE list’ scenario, the vast majority of bonds issued by all carbon-intensive sectors are removed, adding bonds issued by sectors that are not carbon-intensive (see ‘other’ in Figure 4), which also meet the eligibility criteria. Both scenarios keep the volume of purchasable bonds at roughly the same level as in the Bank’s original CBPS list, indicating that concerns about a potential lower aggregate stock of purchasable bonds are easily dismissed as grounds for not implementing these options. In addition, recognising that current carbon-intensive corporates will need financing to decarbonise their activities in line with a green transition, both frameworks retain the green bonds issued by carbon-intensive sectors.

Figure 4: Bank of England (BoE) list vs lower-carbon scenarios

Source: Dafermos, Y., Gabor, D., Nikolaidi, M. and van Lerven, F. (2020). “Decarbonising the Bank of England’s pandemic QE: ‘Perfectly sensible’’’, New Economics Foundation, August 2020.

Another monetary policy tool that could be decarbonised is the Bank’s collateral framework, which is at the core of its liquidity operations and reverberates throughout the financial sector. The Bank requires collateral from commercial banks in exchange for issuing reserves that banks use to clear payments. Consequently, the assets which are eligible as collateral at the Bank of England inevitably become more valuable to the commercial banking sector (and financial sector more widely), incentivising demand for them. The resulting growth in demand for these eligible assets can increase their price and lower their yield.20

The eligibility criteria have mainly to do with the credit quality and maturity of the assets. Since credit rating agencies do not include climate risks in their assessments, climate risks are not priced in when eligibility is decided. In effect, like corporate QE, the Bank’s collateral framework structurally biases market prices and the allocation of capital towards carbon-intensive companies.

To avoid biasing the allocation of capital towards carbon-intensive activities (i.e. creating better financing conditions for these activities), the Bank should climate align its collateral framework by introducing climate-related criteria for collateral. It could exclude ‘super-dirty’ loans or securities, and differentiate haircuts on green/dirty assets21, in a dynamic fashion and in consultation with the GFAT.

By decarbonising its collateral framework and corporate QE programmes the Bank of England would boost green investment and would make less favourable the credit conditions for dirty investment. This would not only be beneficial for the level of carbon emissions, but it could also contribute to the reduction of physical climate risks, especially if other central banks around the globe follow the Bank of England and implement similar policies.22 Although the environmental effects by themselves might not be quantitatively strong, they should still be considered essential and complementary for the decarbonisation of the UK economy.

4.2 Climate-aligned banking regulation

Risk-weighted capital adequacy rules are a significant component of Basel III (and of Capital Requirements Directive (CRD) IV). These rules require that financial institutions hold a minimum amount of capital relative to risk-weighted assets. Required capital can act as a cushion to absorb losses when loans go bad. Risk weights can influence banks’ profit margins for particular lending activities: a higher risk weight tends to make loans more expensive (as more capital is required to grant a loan), while a lower risk weight can make credit expansion cheaper (as less capital is required to grant a loan). So risk weights could affect the willingness of financial institutions to lend. They might also affect the cost of borrowing.

Conventional risk weights neglect climate issues. We thus propose that risk weights be adjusted to take into account the greenness/dirtiness of the assets that banks hold, based on the UK green/dirty Taxonomy. The climate-based risk weighting could take two forms.23 The first form is what is commonly known as the ‘dirty penalising factor’, which implies an increase in the risk weights of carbon-intensive assets. This intervention would make carbon-intensive lending more expensive relative to low-carbon activities since banks would need to hold more capital against environmentally damaging loans. In this respect, bank lending for carbon intensive activities would be directly dis-incentivised, whilst implicitly encouraging bank lending for low-carbon activities.

The second option, a ‘green supporting factor’, entails a reduction in the risk weight assigned to green assets. Such a reduction would encourage banks to provide more environmentally friendly loans to the economy since banks would have to hold less capital against these loans. It could also lead banks to reduce interest rates on green loans relative to interest rates on conventional loans.

In the academic literature there is no consensus on the precise effects of capital requirements and risk weights on lending and the cost of borrowing. For instance, it is not clear if the Small and Medium Enterprises (SME) supporting factor that was introduced at the European level in 2014 was effective in stimulating credit. On the one hand, a study by the European Banking Authority (EBA)24 argues that it was not, but, on the other hand, two more recent empirical studies show that credit was stimulated, at least for medium-sized enterprises25. There is also evidence that capital requirements affect lending, but is not clear if this effect is quantitatively strong.26

A further issue for consideration is that a green supporting factor could undermine financial stability by, first, reducing the capital that banks hold against assets and, second, supporting green credit of high risk. However, since decarbonisation might also reduce financial risks, these potentially adverse effects should be compared with the positive financial effects of the decarbonisation that would be caused by the green supporting factor. In addition, if the introduction of a green supporting factor is combined with a dirty penalising factor, capital requirements are more likely to increase, at least in the short run.

The introduction of the dirty penalising factor also faces some challenges. If it is implemented abruptly, it could reduce economic activity since dirty assets constitute a large part of our carbon-based economy. This, however, could be partially tackled by increasing the dirty risk weights gradually.

5.1 Green supporting/dirty penalising haircuts and margins

Financial institutions participate daily in securities financing transactions (STFs), such as repo agreements and securities lending. In these transactions, securities are used as collateral. The haircut on this collateral (the difference between the market value of an asset and the value ascribed to the asset for collateral purposes) determines the amount of financing that is available for (shadow) banks to finance new assets or lend against those assets. The higher the haircuts, the higher the implicit cost of financing securities and derivatives positions and the lower the build-up of leverage. Similarly, when financial institutions participate in derivatives transactions, the margin (i.e. the amount of collateral that investors should hold in a margin account) determines how much they can invest for a given level of equity. To address the systemic risks that arise from too low haircuts and margins during periods of high financial fragility, a case has been made for macroprudential margin and haircut requirements.27

However, the proposals for macroprudential haircuts and margins ignore the climate effects of shadow banking: while collateral lubricates market-based finance, margins and haircuts are currently set independently of the environmental impact of the underlying collateral. This mobilises credit to activities with detrimental environmental impacts, and creates mark-to-market exposures, via collateral chains, to the sudden, climate-related transition shocks that can affect the price and liquidity of those collateral securities.

To support the transition to a low-carbon economy, margins and haircuts could be calibrated on the basis of the greenness and the dirtiness of the assets deployed as collateral. Dirty penalising haircuts and margins would make dirty assets less desirable in financial markets, having indirect effects on the cost of borrowing of those firms that issue these securities. On the other hand, green supporting haircuts and margins could improve the financing conditions for green projects.

The design and implementation of climate-aligned haircuts and margins could rely on the framework that the Financial Stability Board (FSB) has provided for counter-cyclical haircuts and margins for securities financing transactions.28 This would apply, as the FSB originally envisaged, to all securities financing transactions, indifferent of whether these involve banks, shadow banks, or a combination of the two. In so doing, the scope for banks to engage in dirty regulatory arbitrage is reduced considerably.

The GFAT could play a leading role in advocating for the FSB to move towards this direction. The Bank of England could also support such a development by greening its collateral framework, as proposed in Section 4.1: a climate-aligned collateral framework could be deployed as a basis for the FSB’s climate-aligned calibrations of haircuts and margins.

However, the adjustment of haircuts might not be enough. The FSB could prohibit the use of excessively ‘dirty’ securities as collateral in STFs and derivatives transactions. Such prohibitions could be phased in, similar to the dirty penalising factor in banking regulation, allowing time for investors to adjust to that without causing significant transition risks.

To reduce the potential for regulatory arbitrage via passive investment abroad, the GFAT could contemplate a Financial Transaction Tax (FTT) on ‘dirty’ Exchange-Traded Funds (ETFs), i.e. of ETFs that track equities or fixed income instruments linked with activities that exhibit a high degree of dirtiness. The design of the Green Financial Transaction Tax (GFTT) could draw on the framework developed for the European FTT.29

5.2 Dirty penalising factor for G-SIBs

An additional proposal is the introduction of a dirty penalising factor for Global Systemically Important banks (G-SIBs). According to Basel III, G-SIBS (which are identified based on a number of criteria, such as size, complexity and interconnectedness) need to hold additional common equity Tier 1 capital. This buffer can range between 0% and 3.5%.30

The dirtiness of the assets in which G-SIBs invest could be taken into account when the buffer is determined. This could take the form of additional requirements on top of the existing ones. Alternatively, the dirtiness of the assets could be considered as one of the criteria that should be taken into account when the buffer is determined, without changing the upper limit of 3.5%. The rationale of introducing a dirty penalising factor could be based either on risk considerations (since dirty assets face higher climate transition risks) or more directly on the need for G-SIBs to play a more active role in the process of decarbonisation. Given the prominent role of G-SIBs in the City of London, the introduction of such a dirty penalising factor could initiate a major shift towards less carbon-intensive investments in the UK financial system.

Therefore, the UK regulators could encourage the introduction of these additional requirements in Basel III. It should be pointed out that if this recommendation is implemented in combination with the dirty penalising factors suggested in Section 4.2, some G-SIBs may be penalised twice for their exposure to dirty assets. Although this might reinforce the transition effects, it will be beneficial for the decarbonisation of shadow banking activities, since many G-SIBs engage substantially in such activities.

Central banking and financial supervision and regulation are hardly the only game in town when it comes to tackling the environmental breakdown. Fiscal, industrial and environmental regulation policies have a stronger and more substantial role to play in achieving the low-carbon transition quickly. Yet, the Bank of England – alongside supporting government and financial regulatory authorities – do have a critical role to play in structurally realigning our financial sector with the challenges and risks posed by the climate crisis. Indeed, the urgency of the climate crisis requires that all policy tools are used for the purpose of avoiding a climate breakdown.

The implementation of our proposal could make the UK financial system compatible with the climate emergency. However, it is important for these proposals to be implemented taking into account the history of the UK capitalism. Through its past emissions, the UK has contributed significantly (along with other countries of the Global North) to global warming that is affecting the countries of the Global South disproportionately. The UK government should explicitly recognise that and should take initiatives that would ensure that the Global South will be able to achieve climate mitigation and adaptation, free of neo-colonial approaches. Climate reparations,31 other climate-related transfers and debt relief programmes32 need to be part of such initiatives.

HM Treasury and Department for Business, Energy & Industrial Strategy (2019). ‘Green finance strategy’, 2019; HM Treasury (2020). ‘Chancellor sets out ambition for future of UK financial services’, November.

Our proposals draw on Gabor, D., Dafermos, Y., Nikolaidi, M., Rice, P., van Lerven, F., Kerslake, R., Pettifor A., and Jacobs, M. (2019). ‘Finance and climate change: a progressive green finance strategy for the UK’, Report of the independent panel commissioned by Shadow Chancellor of the Exchequer John McDonnell MP. In some paragraphs full sentences have been taken from this report.

See also Nikolaidi, M. (2019). ‘Greening the UK financial system’, CommonWealth, July.

Matikainen, S., Campiglio, E. and Zenghelis, D. (2017). ‘The climate impact of quantitative easing’, Policy Paper, Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science.

Dafermos, Y., Gabor, D., Nikolaidi, M. and van Lerven, F. (2020). ‘Decarbonising the Bank of England’s pandemic QE: ‘Perfectly sensible’’, New Economics Foundation, August.

See, for example, Campiglio, E., Dafermos, Y., Monnin, P., Ryan-Collins, J., Schotten, G. and Tanaka, M. (2018). ‘Climate change challenges for central banks and financial regulators’, Nature Climate Change, 8 (6), 462-468.

See Gabor, D., Dafermos, Y., Nikolaidi, M., Rice, P., van Lerven, F., Kerslake, R., Pettifor A., and Jacobs, M. (2019). ‘Finance and climate change: a progressive green finance strategy for the UK’, Report of the independent panel commissioned by Shadow Chancellor of the Exchequer John McDonnell MP. See also Berg, F., Koelbel, J.F. and Rigobon, R. (2019). ‘Aggregate confusion: the divergence of ESG ratings’, MIT Sloan Scholl of Management.

See HM Treasury (2020). ‘Chancellor sets out ambition for future of UK financial services’, November.

See EU Technical Expert Group on Sustainable Finance (2020). ‘Financing a sustainable European economy: Taxonomy technical report’, March.

See HM Treasury (2020). ‘Chancellor sets out ambition for future of UK financial services’, November.

Many corporations have lobbied against a taxonomy of dirty activities. See e.g. Schreiber, P., Pinson, L. and Ileri, E.C. (2020). ‘In the shadows: who is opposing the EU Taxonomy for polluting activities’, Reclaim Finance, December.

For the need to develop a dirty taxonomy, see also Vaze, P., Meng, A. and Giuliani, D. (2019). ‘Greening the financial system: tilting the playing field. The role of central banks’, Climate Bonds Initiative, October.

See also Gabor, D. (2020). ‘Three ideas for a progressive sustainable finance agenda’, Foundation for European Progressive Studies, June.

See TCFD (2020). ‘Task force on Climate-related Financial Disclosures Status Report: 2020 Status Report’, October.

See HM Treasury (2020). ‘Chancellor sets out ambition for future of UK financial services’, November.

The GFAT should include representatives from the Bank of England, the HM Treasury, the UK Technical Expert Group (TEG) on Green Finance and regulatory bodies mandated to oversee the functioning of non-bank financial institutions, including the Financial Conduct Authority and the Pensions Regulator. It should coordinate closely with the Committee on Climate Change (CCC), and should engage in regular consultations with civil society organisations and private sector bodies for constructive feedback. The GFAT will therefore have a much broader and more permanent role compared to the Green Finance Taskforce that was established by the UK government in 2017.

Bank of England (2020). ‘The Bank of England’s climate-related financial disclosure’, June.

Baily, A. (2020). ‘The time to push ahead on tackling climate change’, November.

For a recent discussion of central bank tools that can support the low-carbon transition, see Dikau, S., Robins, N. and Volz, U. (2020). ‘A toolbox for sustainable crisis response measures for central banks and supervisors’, INSPIRE briefing paper, November.

Moreover, the Bank of England applies haircuts to the collateral it takes in exchange for reserves, and adjusts these haircuts depending on the risk profile of the asset; a higher (lower) haircut reduces (increases) the available central bank liquidity per eligible asset used as collateral. These haircuts also have an impact on the haircuts used by central counterparties and market participants in repurchase agreement (repo) contracts; see e.g. BIS (2015). ‘Central bank operating frameworks and collateral markets’, CGFS Papers No 53.

For the definition of haircuts, see Section 5.

Dafermos, Y., Nikolaidi, M. and Galanis, G. (2018). ‘Can green Quantitative Easing (QE) reduce global warming?’, Foundation for European Progressive Studies, July.

Dafermos, Y and Nikolaidi, M. (2020). ‘How can green differentiated capital requirements affect climate risks? A dynamic macrofinancial analysis’, available at SSRN.

EBA. (2016). ‘EBA Report on SMEs and SME Supporting Factor’, European Banking Authority, EBA/OP/2016/04.

Mayordomo, S. and Rodrí guez-Moreno, M. (2018). ‘Did the bank capital relief induced by the Supporting Factor enhance SME lending?’, Journal of Financial Intermediation, 36, 45-57; Dietsch, M., Fraisse, H., Le , M., Lecarpentier, S. (2019). ‘Lower bank capital requirements as a policy tool to support credit to SMEs: evidence from a policy experiment’, EconomiX No. 2019-12, University of Paris Nanterre.

Gambacorta, L. and Shin, H.S. (2018). ‘Why bank capital matters for monetary policy’, Journal of Financial Intermediation, 35, 17-29; Gropp, R., Mosk, T., Ongena, S. and Wix, C. (2018). ‘Banks response to higher capital requirements: evidence from a quasi-natural experiment’, The Review of Financial Studies, 32 (1), 266-299.

ECB (2016). ‘A case for macroprudential margins and haircuts’, Financial Stability Report, Special features, May.

FSB (2014). ‘Strengthening oversight and regulation of shadow banking regulatory framework for haircuts on non-centrally cleared securities financing transactions ’, Financial Stability Board, October.

See the European Commission proposals for a Financial Transactions Tax. See also Bharadia, K. and Boughey, L. (2019). ‘Reinforcing resilience: Making the UK a citadel of long-term finance’, Intelligence Capital, September.

For the recent required levels of additional capital buffer for G-SIBs, see FSB (2020). ‘2020 list of global systemically important banks (G-SIBs)’, Financial Stability Board, November.

See Perry, K. (2020). ‘Realising climate reparations: towards a global climate stabilization fund and resilience fund programme for loss and damage in marginalised and former colonised societies’, available at SSRN.

See, for example, Volz, U., Akhtar, S., Gallagher, K.P., Griffith-Jones, S., Haas, J., and Kraemer, M. (2020). ‘Debt relief for a green and inclusive recovery: a proposal’, Berlin, London, and Boston, MA: Heinrich-Böll-Stiftung; SOAS, University of London; and Boston University.