The question of if and how monetary policy should take financial stability considerations into account has once again become topical in light of the unprecedented monetary tightening in 2022 and 2023 following years of accommodating policy. We present a coherent empirical framework based on quantile regressions which can be employed by policy makers to assess the macro-financial interlinkages and the potential financial stability trade-offs faced by monetary policy. Using the estimated model, we conduct a scenario analysis and find ex post evidence of the intertemporal financial stability trade-off of monetary policy: Limiting the build-up of financial vulnerabilities today through tighter policy, while potentially sacrificing price or output stability, can contribute to lower financial stability risks and consequently increase macroeconomic stability in the medium-term. This finding supports the notion that the impact of monetary policy on not only the most likely macroeconomic outcome, but also the tail risks, including those stemming from financial conditions, should be taken into account when deciding on the appropriate policy stance.

Since the global financial crisis (GFC) of 2008-09, the debate on how monetary policy should take financial stability considerations into account has gained momentum, sparking several pertinent questions. For instance, could the GFC have been avoided if monetary policy had pre-emptively countered the credit boom, or did the loose monetary policy stance for most of the post-crisis period have the unintended consequence of increasing financial vulnerabilities, or should central banks tighten monetary policy rapidly or gradually in response to the recent surge in inflation, with different speeds of tightening potentially implying different risks to financial stability?

Drawing from our recent paper (Chavleishvili et al. (2023)), this article outlines a coherent empirical framework that monetary policymakers can use to address the questions above, where relevant. The framework builds on a structural quantile vector autoregression (QVAR) model – recently introduced by Chavleishvili and Manganelli (2023) – to estimate the dynamic interactions between inflation, economic activity, monetary policy rates and financial stability conditions in the euro area, the latter being captured by two summary indicators measuring financial imbalances and system-wide financial stress, respectively. Estimating the VAR by quantile regression enables us to uncover state-dependent nonlinearities by letting the joint conditional distributions flexibly change location, scale and shape. Such nonlinearities appear particularly relevant for the macro-financial linkages, such as those highlighted in the seminal “growth-at-risk” papers by Adrian et al. (2019) and Adrian et al. (2022), which find an asymmetric, much stronger response of downside risks to growth from increased financial distress, implying that the economic costs of financial crises can be much higher than previously thought. Our framework thus allows policymakers to evaluate policy options not only in terms of the most likely outcomes of their key target variables, but also in terms of the associated tail risks of particularly undesirable states (e.g. systemic crises). Hence, the empirical framework we use lends itself to adopting a risk management approach to deal with financial stability considerations in monetary policy.

Policy measures have since the GFC been introduced to reduce the risk of systemic crises, and while there is general agreement on the need for preventive macroprudential policy, the jury is still out on the role of monetary policy in taming the financial cycle.1 Using the QVAR, we assess financial stability implications, and their ultimate effects on the risks for growth and inflation, of different systematic monetary policies through tailored scenario analysis. This article focuses on a scenario that addresses, with the benefit of hindsight, the intertemporal financial stability trade-off, or “credit-bites-back” case (Kashyap and Stein (2023)), associated with the financial boom-bust cycle that eventually erupted in the GFC. In particular, we quantify the intertemporal macroeconomic costs and benefits of a counterfactual “leaning against the wind” policy, in which monetary policy is pre-emptively more restrictive in the years leading up to the crisis, lowering output and inflation in the short term, but reduces the severity of a potential crisis in the medium term. Consequently, financial stability considerations are elevated from pure “side effects” of monetary policy, to a direct channel with first-order effects on inflation and growth.

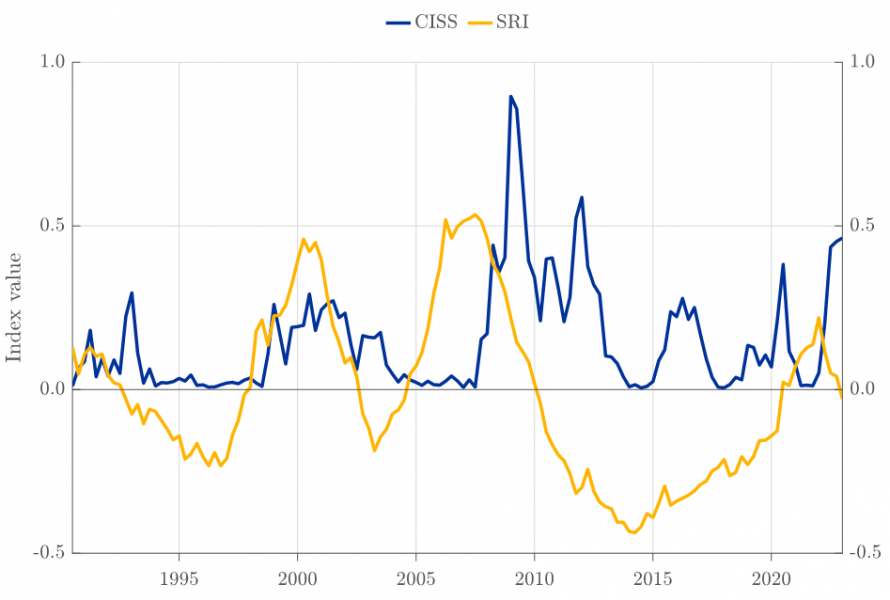

Essential to our framework is partitioning financial stability conditions along two dimensions: the ECB’s systemic risk indicator (SRI) reflects the financial cycle and thus gauges system-wide financial imbalances (see Lang et al. (2019)), while the composite indicator of systemic stress (CISS) quantifies the level of systemic stress in the financial system (see Holló et al. (2012) and Chavleishvili and Kremer (2023)).2 The concepts of overall financial imbalances and systemic stress are intimately related: the first relates to systemic risk ex ante (i.e., the risk of a future financial crisis) and the second to systemic risk ex post (i.e., the severity of a realised financial crisis). A scenario of a typical financial boom-bust cycle would then be characterised by an elevated level of the SRI followed by a steep rise in the CISS as the bubble bursts, the GFC being the most prominent example (see Figure 1).3

Figure 1: Composite Indicator of Systemic Stress (CISS) and the Systemic Risk Indicator (SRI) for the euro area, 1990Q2:2022Q4

Source: European Central Bank. Note: See Chavleishvili and Kremer (2023) and Lang et al. (2019) for a detailed description of the CISS and SRI, respectively.

To quantify the intertemporal financial stability trade-off with our QVAR model, we now ask the question: How would potential outcomes have changed in the years surrounding the GFC if euro area monetary policy had leaned against the wind, i.e., increased rates in response to escalating financial imbalances and lowered them in response to the surge in financial distress?

Starting the scenarios in 2004Q4, our baseline scenario mimics the actual period around the GFC, that is, a rapid build-up in vulnerabilities, captured by the SRI, followed by surges in systemic stress, captured by the CISS, in 2008. We do this by choosing an appropriate set of ‘quantile restrictions’ on the CISS and the SRI, which lets us push those variables along a certain path while still leaving them susceptible to changes in the other model variables, e.g., interest rates.4 In addition, baseline policy rates are assumed to follow their historical values over the period. In our counterfactual scenario, policy rates increase an additional 25 basis points compared to the baseline for four consecutive quarters starting in 2004Q4 in response to the acceleration of the SRI and decrease an additional 25 basis points for four consecutive quarters starting in 2008Q1 when the financial turmoil escalated.

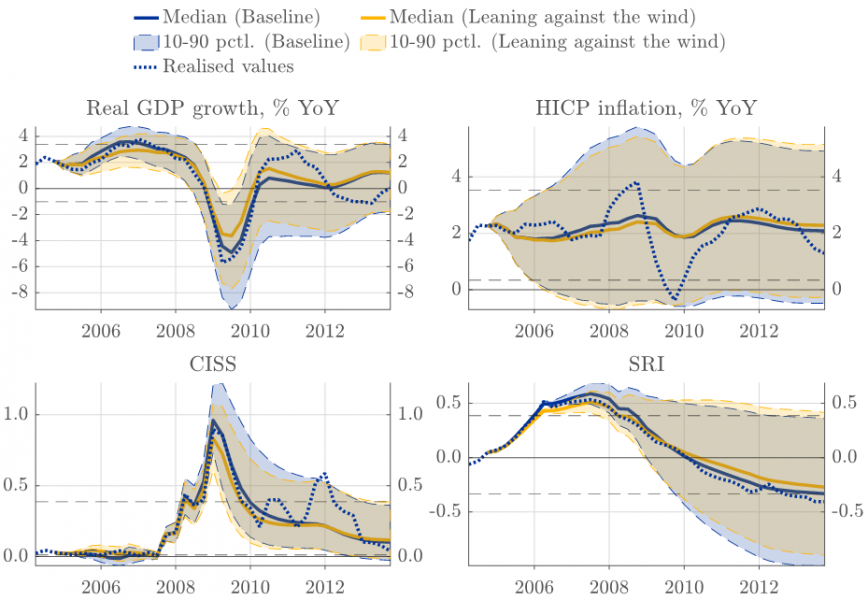

Figure 2 plots the 10th and 90th percentiles (shaded areas) of the conditional distributions of the CISS, the SRI, inflation and real GDP growth along with the conditional median in the baseline (Blue) and counterfactual (Yellow) scenarios. Realised values over the projection horizon are also included as points of reference. Importantly, the 10th to 90th percentile ranges reflect the width of the forecast distributions and should not be confused with confidence bands from standard statistical analysis.

Figure 2: Conditional quantile forecasts of the real and financial variables in the baseline and counterfactual scenarios

Source: European Central Bank and author’s calculations. Note: Scenarios are implemented through forward simulations as suggested in Chavleishvili and Manganelli (2023). We run 1 million simulations to sufficiently explore the probability space of the respective distributions. Horizontal dashed lines indicate the 10th and 90th unconditional quantiles.

Looking at the conditional forecast distribution of the SRI, tighter monetary policy successfully manages to curb some, though not all, of the build-up in financial vulnerabilities, causing the SRI to plateau at a lower level compared to the baseline. Turning to the CISS, the counterfactual policy has noticeably lowered upside risks to systemic stress during the crisis, as indicated by the difference between the top of the blue and yellow shaded areas, respectively. As such, leaning against the wind has reduced the probability of realising exceptionally adverse levels of systemic stress.

The counterfactual policy is less apparent in the inflation distribution, although there is an initial downward shift. In contrast, the effects on the growth distribution are rather pronounced, shifting noticeably downward during the boom, representing the main costs of the leaning policy, and markedly upward during the crisis period, most strongly in its lower tail.5 The outsized improvement in downside risks to growth constitute the major benefits of the leaning policy, highlighting the important result that the ultimate real costs of the financial crisis have been lowered through the impact of monetary policy on upside risks of systemic stress.

As such, we find evidence supporting the presence of the intertemporal financial stability trade-off for monetary policy in certain circumstances. Whether policy makers would ultimately decide to pursue some form of leaning against the wind depends on, among other things, their preferences for intertemporal gains and losses in macroeconomic stability, the shape and location of the projected distributions, as well as the perceived importance of inflation vis-à-vis output stability.6 It should be stressed, however, that our cost-benefit analysis for the GFC period is conducted ex post. Specifically, we take the financial crisis as given, while in a real-time, ex ante context, most relevant to policy makers, a crisis only occurs with a certain probability and a counterfactual analysis would necessarily be evaluated over a range of plausible probability-weighted scenarios, both with and without a crisis. If the probability of a financial crisis is judged to be low, then leaning against the wind may prove too costly in expectation, despite providing a net benefit in the event of a crisis.

The role played by monetary policy in shaping the balance of macroeconomic risks through the outlook for financial stability may require careful consideration by policymakers when deciding on the future policy path. Indeed, following the recent inflationary bout in major economies and the transition from a regime of historically low interest rates to one of accelerated interest rate hikes by the respective central banks, the interaction between monetary policy and financial stability has received renewed attention, both with respect to the immediate effects of decisive monetary tightening, but also the medium-term consequences of persistently easy policy.

In this note we presented one way to empirically gauge the macro-financial interlinkages with monetary policy and assess the net macroeconomic benefits of different policy paths using the QVAR for the euro area, specifically highlighting how monetary policy may potentially improve outcomes during a crisis by pre-emptively acting against the build-up of financial imbalances, thereby lowering the medium-term upside risks to systemic stress and, by extension, the downside risks to growth. Overall, the findings in Chavleishvili et al. (2023) suggest the following answer to the question posed in our title: No, monetary policy cannot ignore financial stability risks. This is true in the sense that an appropriate cost-benefit analysis should always be conducted. However, whether financial stability conditions ultimately factor into the actual stance of monetary policy and become a binding constraint depends on the outcome of the cost-benefit analysis.

Adrian, T., Boyarchenko, N. and Giannone, D. (2019). Vulnerable growth. American Economic Review, 109(4): 1263–89.

Adrian, T., Grinberg, F., Liang, N., Malik, S. and Yu, J. (2022). The term structure of growth-at-risk. American Economic Journal: Macroeconomics, 14(3): 283–323.

Bernanke, B. S. (2015). Federal Reserve policy in an international context. Paper presented at the 16th Jacques Polak Annual Research Conference hosted by the International Monetary Fund, Washington, D.C., November 5–6, 2015.

Chavleishvili, S., Kremer, M. and Lund-Thomsen, F. (2023). Quantifying financial stability trade-offs for monetary policy: a quantile VAR approach. ECB Working Paper, 2833.

Chavleishvili, S. and Kremer, M. (2023). Measuring systemic financial stress and its risks for growth. ECB Working Paper, 2842.

Chavleishvili, S. and Manganelli, S. (2023). Forecasting and stress testing with quantile vector autoregression. Journal of Applied Econometrics, forthcoming.

Holló, D., Kremer, M. and Lo Duca, M. (2012). CISS – A composite indicator of systemic stress in the financial system. ECB Working Paper, 1426.

Kashyap, A. K. and Stein, J. C. (2023). Monetary policy when the central bank shapes financial-market sentiment. Journal of Economic Perspectives, 37(1): 53–76.

Lang, J. H., Izzo, C., Fahr, S. and Ruzicka, J. (2019). Anticipating the bust: a new cyclical systemic risk indicator to assess the likelihood and severity of financial crises. ECB Occasional Paper, 219.

While macroprudential, rather than monetary, policy is often regarded as the first line of defence against financial instability (Bernanke (2015)), it can suffer from long implementation lags and limited scope, leaving room for monetary policy to take financial stability considerations into account as well.

The SRI is a weighted-average of the components: two-year change in the bank credit-to-GDP ratio; two-year growth rate of real total credit; two-year change in the debt-service-ratio; three-year change in the residential-real-estate price-to-income ratio; three-year growth rate of real equity prices; current account-to-GDP ratio.

Importantly, however, a systemic stress episode need not always adhere to this pattern and can arise from non-imbalance related factors as seen, for instance, during the COVID19 turmoil in March 2020.

The baseline additionally employs a limited number of quantile restrictions on real GDP growth, although this does not affect the qualitative results of the exercise.

While statistical significance varies across quantiles, highlighted results are broadly significant at the 10% level.

Using a conventional central bank loss function, sensitive to symmetric deviations from a 2% inflation target and negative growth, Chavleishvili et al. (2023) find that leaning against the wind would’ve been a net benefit, ex post, compared to the baseline. The result also holds when only additional pre-emptive tightening, but not additional rate decreases, is considered, albeit at a smaller scale. In both cases, the net benefit is primarily driven by the improvement in downside risks to growth outweighing short term deviations in inflation from its target.