Fiscal policy plays a prominent role in climate change mitigation and adaptation. An adequate combination of revenue and expenditure policies is crucial to achieve the European Union (EU) net greenhouse gas (GHG) emission reduction targets. We provide an overview of the main fiscal instruments in place in European Union Member States to tackle climate change as well as the key fiscal challenges for a comprehensive European climate change strategy, focusing on the carbon pricing gap and the green investment gap.

Climate change is one of the most pressing challenges for humanity and requires countries to swiftly reduce (GHG) emissions. Currently, all EU countries use a combination of revenue and expenditure policies to mitigate the effects of climate change. On the revenue side, the European Union Emissions Trading System (EU ETS) plays a prominent role. On the expenditure side, most of the policies involve investing in clean energy sources and improving energy efficiency, largely reflecting EU policies. Besides fiscal policy, governments can use command-and-control regulation, such as setting environmental standards, to support emissions reduction. However, so far, the use of fiscal instruments has been insufficient to meet current climate-related goals. The EU has pledged to reach (net) carbon neutrality by 2050. This will necessitate additional policy efforts, many of which will have a fiscal angle.

Drawn from our recent paper (Avgousti et al., 2023), we stress the important role of fiscal policy in achieving the EU’s climate targets. We take stock of the fiscal repercussions of climate change by focusing on the impact of extreme weather events on the fiscal balance in EU Member States. We also look at the interaction of climate change and climate change policy with debt sustainability, whose impact is subject to great uncertainty. We discuss the current fiscal instruments in EU Member States and the gaps in investment needs and carbon pricing that need to be bridged in order to meet climate change goals.

Climate change will generate both direct and indirect negative macroeconomic and fiscal effects. However, estimates of the climate change impact on output are very uncertain, depend heavily on the underlying assumptions and the modelling of feedback loops and are largely heterogeneous not only across and within countries, but also across sectors. Extreme weather events, whose probability is likely to increase over time due to climate change, may place a burden on public finances. Their budgetary impact can be direct – higher public expenditure associated with relief measures, repairs and maintenance of infrastructure but also prevention measures (e.g. building of dykes) – as well as indirect, namely through an eroding revenue base as a result of output loss or higher public expenditure on social payments owing to lower incomes. Empirical studies on the fiscal costs of natural disasters are scarce but point to a rather limited budgetary effect (e.g. Melecky and Raddatz, 2015; Lis and Nickel 2010).1

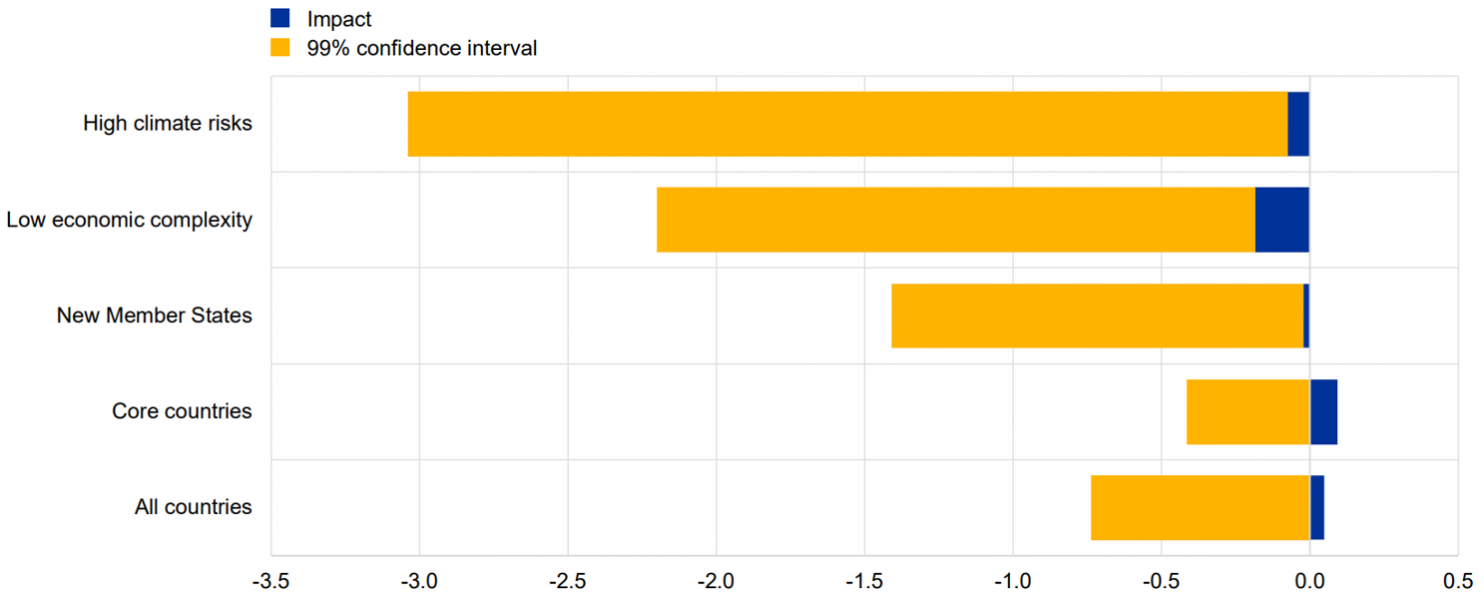

We explore the impact of extreme weather events on fiscal balances by considering an unbalanced panel of 26 EU Member States during the period 1980-2021.2 The dependent variable is the general government primary fiscal balance to GDP ratio.3 Our proxy for the extreme weather event shock is the first principal component of the (standardised) series: the number of extreme weather events, the number of casualties, the total number of affected individuals and the estimated damages (as a percentage of GDP and in per capita terms). Our estimates suggest that there is no economically significant relationship between extreme weather events and the fiscal balance when considering all countries and all shocks in the sample (Chart 1). The magnitude of the estimated coefficient for the effects of extreme weather events on the fiscal balance is rather small, more so, in the largest and richest economies. Nonetheless, the fiscal impact of natural hazards becomes substantially higher when considering only the largest weather events (i.e. at least two standard deviations above the mean). The central estimate points to a deterioration in the fiscal balance of 0.7% of GDP, which increases to 1.4% for new Member States. The estimated fiscal impact can be even larger when considering countries that are less economically diversified than the sample average or that rank higher in terms of exposure to climate risks, calling for continued action to enhance their climate readiness and resilience.

Chart 1: Impact of extreme weather events on fiscal balances (percentages of GDP)

Source: Own calculations.

Notes: The shock is the principal component derived from the number of extreme weather events, casualties, affected individuals and the estimated damages expressed in euro, as a percentage of GDP and in per capita terms, as reported by EM-DAT. Results for the baseline case are in blue, while those for large shocks only (i.e. two standard deviations) are in yellow. New Member States include Bulgaria, the Czech Republic, Estonia, Croatia, Latvia, Lithuania, Hungary, Poland, Romania, Slovenia and Slovakia. Core countries include Belgium, Germany, Ireland, Greece, Spain, France, Italy, Luxembourg, the Netherlands, Austria and Portugal. The Economic Complexity Index (ECI) is based on Hidalgo and Hausmann (2009). The 2021 Global Climate Risk Index is from Eickstein et al. (2021).

EU countries rely on a variety of policy tools to encourage economic agents to reduce GHG emissions. On the fiscal policy front, the measures currently in place in EU Member States encompass the EU ETS, national emissions trading schemes, carbon taxes and other environmental tax policies, public expenditure measures and regulatory interventions (command-and-control policies). Overall, estimates for GHG emissions by 2030 suggest that substantial policy efforts will be required to reduce GHG emissions by at least 55% with respect to 1990 levels in 2030 and to reach (net) carbon neutrality by 2050.

Expenditure measures adopted to combat climate change are manifold but heterogeneous across EU countries. These include transfers to households and subsidies to firms to incentivise emission reductions and lower energy intensity, public expenditure to protect the environment, and public R&D spending to promote cleaner technologies and climate change mitigation. Most measures have been in place for several years and often reflect EU initiatives, such as those related to energy efficiency and a greater share of renewable energy. Overall, general government expenditure for environmental protection in the EU reached 0.8% of GDP in 2019, ranging from 0.2% in Finland to 1.4% in Malta, Greece and the Netherlands. Investment constitutes around a fifth of environmental protection expenditures, with EU Member States spending on average 0.15% of GDP in 2019. Investment grants related to environmental protection and R&D expenditure remain very low in the EU.

Furthermore, some environmentally harmful policies are still in place and their removal would be beneficial for the environment and the fiscal budget. Such policies mainly comprise transfers and tax abatements (such as tax exemptions or tax credits) to households and energy-intensive industries to mitigate higher energy costs, which were mostly designed for motives such as distributional aspects and competitiveness or to provide fiscal stimulus in an economic crisis. Even if our study relates to before the current energy crisis, these harmful subsidies are likely to have regained importance in the current crisis.

On the revenue side, all EU countries have environmental taxes in place, though with relatively small revenues, representing only 5.9% of EU countries’ total tax revenues in 2019 (2.4% of EU GDP). Energy taxes, which encompass carbon taxes and excise taxes on energy products, have been one of the main instruments used to fight climate change and pollution and reduce energy use in the EU, followed by transport and pollution taxes. On average, energy taxes account for around three-quarters of environmental tax revenues in EU countries. The literature has identified carbon pricing policies (carbon taxes and emissions trading systems) as an effective incentive-based fiscal policy measure for climate change mitigation (see, for example, Krupnick and Parry, 2012).

Almost half of the CO2 emissions in the EU have been subject to the EU ETS. Government revenues from the auction of emission allowances under the EU ETS as a share of GDP vary across EU countries, and among others depend on the provisions for free allocation of permits. In some EU Member States (e.g. Germany, Greece, Hungary, Latvia and Portugal), government revenues raised from the EU ETS are earmarked as subsidies to incentivise emission reduction and support renewable energy sources and energy efficiency in residential buildings. After the surge in energy prices in 2022, some EU countries (e.g. Italy, Greece and Poland), allocated (increases in) EU ETS revenues to cushion the impact of higher energy prices on households and companies. For the part of emissions not covered by the EU ETS only a few EU Member States have an explicit carbon tax in place and with low rates and a varying share of emissions coverage.

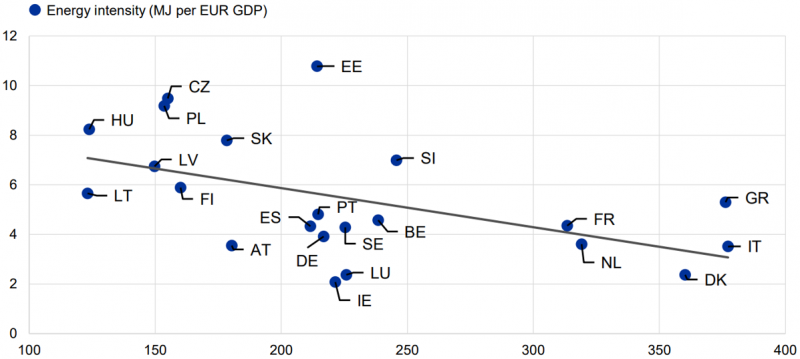

Another important aspect for climate change mitigation relates to the level of and change in energy efficiency and how this determines the change in energy intensity across countries. To this end, it is useful to look at the implicit tax rate on energy, which sets energy tax revenues in relation to energy consumption, and to compare it with an overall measure of energy intensity per country. Chart 2 reveals a negative correlation between the implicit tax rate on energy and energy intensity in the EU. Countries with higher implicit taxes on energy show a lower energy intensity of GDP, notwithstanding sectoral differences across countries.4 This is particularly the case for Denmark, pointing to higher energy efficiency. On the other side, the Czech Republic, Estonia, Hungary and Poland have low implicit tax rates and a rather high level of energy intensity. Nevertheless, rising energy taxes can have an adverse effect on international competitiveness if not compensated by higher energy efficiency, at least in the short term.

As regards the regulatory policies, these mostly relate to energy efficiency and renewable energy sources. As most of these policies reflect regulations initiated at EU level, it may appear surprising to see large cross-country differences. Yet, in 2019, for example, Belgium and France had (with almost 100 regulations) ten times more regulations in place than the Netherlands, Greece or Hungary.

Chart 2: Energy intensity and implicit tax on energy (MJ per EUR GDP; EUR per tonne of oil equivalent, 2019)

Sources: Eurostat, OECD and own calculations.

Notes: The implicit tax rate on energy is the energy tax revenues in relation to the corresponding energy consumption, expressed in oil equivalent. Energy intensity is taken from the OECD and is measured as units of energy (in millions of joules) per unit of GDP (in euro).

Estimates quantifying the additional green investment needed to reach the 2030 EU climate target vary widely. According to the European Commission (2020a and 2021a), the additional green (public and private) investment needed at EU level by 2030 amount to around €520 billion per year (3.7% of 2019 GDP). Most of the green investment gaps are in the transport and residential sectors. The investment needs identified in the renewable energy sector (power grid and plants) are considerably lower, which may reflect the strong surge in the share of renewable energy consumption over the past two decades. However, green investment needs differ not only across sectors but also across countries. Based on countries’ national energy and climate plans (NECPs) for the period 2021-30, the largest investment gaps are identified in Portugal, Romania and Bulgaria (amounting to around 7% of GDP per year), while in Denmark, Finland and Sweden the annual investment needs are well below 1% of GDP. Although a large share of the green investment will need to be borne by the private sector, the public sector can contribute either directly, through public investment, or indirectly, for example through co-financing, private-public partnerships or State guarantees. The (unweighted) share of green public investment at EU level is expected to amount to 45% of total green investment, with large differences among countries (EIB, 2021b). If taken at face value and based on the Commission estimates adjusted for the revised 2030 emission target, this would imply almost 1.8% of EU GDP (€235 billion) in annual additional green public expenditure in 2021-30. The Recovery and resilience Facility, the cornerstone of NGEU will help finance some of the additional green investment needs, while efforts to set up dedicated instruments to finance green investment relate to both the development of sustainable finance standards (including the EU Taxonomy) and the issuance of green bonds.

A second fiscal challenge relates to the high carbon pricing gap in EU countries, pointing to only a low fraction of emissions being taxed. Carbon prices, both in the form of taxes and trading schemes, were relatively low in the EU in 2018. The average explicit carbon tax across all sectors of the economy – weighted by the sectors’ share of total emissions – varied across EU countries from €0.1/tCO2 in Estonia and Spain to around €20/tCO2 in Finland and France, and €25/tCO2 in Sweden. Since then, EU ETS emission permit prices have increased and an extension of EU ETS is foreseen in the EU’s Fit-for-55 policy package to achieve the EU emission reduction targets, which implies a reduction in the sizeable carbon pricing gaps across EU countries and less fragmented and uneven carbon taxation across sectors.

Governments have a key role to play in climate change mitigation. In the EU, additional measures are needed to achieve the EU’s new target of carbon neutrality by 2050, enlarging the scope and nature of fiscal measures to reduce GHG emissions. Although many policy instruments are already in place, efforts are rather heterogeneous across EU countries, while mitigation policies need to be more effective and broad-based across the EU economy. In addition, green public investment will have to increase over the coming decades and act as a catalyst for private investment. A comprehensive investment strategy would help promote the economic transformation needed to reduce GHG emissions. European initiatives, such as NGEU, and green financing may also facilitate this green transformation.

Finally, when designing climate change policies, two issues that significantly affect the policy mix need to be borne in mind. First, the impact of taxes and other instruments on wealth distribution, as some of these may have more of an impact on poorer households increasing inequality, and second, the loss of competitiveness when carbon taxation is not multilaterally imposed. On the distributional consequences of carbon pricing, in Avgousti et al. (2023), we develop a detailed analysis of the impact of a carbon tax on inequality in Italy and show how a transfer of part of the revenue to low income households would reduce inequality. Assuming a quintile-specific government transfer, low income households could afford to even increase their consumption of goods despite the adverse impact of the carbon tax. In this regard, governments should include a compensation mechanism for those with fewer resources. Second, climate change is a global challenge that requires stronger international collaboration to achieve a worldwide reduction in GHG emissions. A global carbon tax would not only be essential to reduce carbon emissions to net zero but would also help to minimise economic distortions and reduce international trade tensions.

Avgousti, A., F. Caprioli, G. Caracciolo, M. Cochard, P. Dallari, M. Delgado-Téllez, J. Domingues, M. Ferdinandusse, D. Filip, C. Nerlich, D. Prammer, K. Schmidt and A. Theofilakou, “The climate change challenge and fiscal instruments and policies in the EU”, Occasional Paper Series, No 315, ECB, Frankfurt am Main, April.

European Commission (2020a), “Kick-starting the journey towards a climate-neutral Europe by 2050”, EU Climate Action Progress Report, November.

European Commission (2021a), “Impact assessment report”, Commission Staff Working Document, No 621, July.

European Investment Bank (2021b), “Building a smart and green Europe in the COVID-19 era”, Investment Report 2020/2021.

Krupnick, A. and Parry, I. (2012), “What Is the Best Policy Instrument for Reducing CO2 Emissions?”, in Parry, I., de Mooij, R. and Keen, M. (eds.), Fiscal Policy to Mitigate Climate Change: A Guide for Policymakers, International Monetary Fund.

Melecky, M. and Raddatz, C. (2005), “Fiscal Responses after Catastrophes and the Enabling Role of Financial Development”, The World Bank Economic Review, Vol. 29, Issue 1, pp.129-149.

Lis, E. and Nickel, C. (2010), “The impact of extreme weather events on budget balances”, International Tax and Public Finance, Vol. 17, pp. 378-399.

The fiscal costs of physical risks can differ compared with the costs of transition risks depending on the adaptation (e.g. coastal protection) and mitigation capacity of each economy. Yet, the overall cost may be higher, as some of the costs might fall on the private sector via insurance.

Data on extreme weather events are taken from the Emergency Events Database (EM-DAT).

We include controls for the economic cycle, the lagged fiscal balance, the level of debt to GDP, long-term interest rates, as well as country-specific and time-specific effects.

The implicit tax rate reflects to some extent the production structure of the economy, namely it is more difficult for countries that rely on energy-intensive industries to impose higher energy taxes.