Labour market data can contain important information for monetary policy, but for the euro area, some of the key indicators, such as employment and hours worked, are available only at a quarterly frequency and with a considerable lag. However, the nowcasting literature has not put much focus on these variables so far. We therefore developed a suite of models to provide a timely estimate (nowcast) of euro area quarterly employment growth using a broad range of monthly indicators. The suite includes a batch of different dynamic factor model and bridge equation specifications which we evaluate in a real-time setting over a sample spanning 2013-2022. We find that our models can nowcast quarterly employment growth reasonably well against benchmarks such as a random walk or the Eurosystem/ECB staff macroeconomic projections. Although the forecasting performance deteriorates at the start of COVID-19 pandemic, the model suite outperforms the benchmarks again thereafter. The pandemic shocks also highlight the advantages of averaging over a multitude of nowcasting approaches.

Timely information on the euro area labour market developments is of key importance for monetary policy. In particular, labour market indicators can provide useful information about the state of the economy and medium-term inflationary pressures. However, key labour market statistics for the euro area, such as total employment or hours worked, are published only at a quarterly frequency and with a considerable delay. While Eurostat publishes the preliminary flash estimate of GDP 30 days after the end of the reference quarter, the first (flash) aggregate euro area estimate of quarterly total employment is released with a lag of 45 days, and the second, more detailed estimate with a delay of about 66 days. At the same time, monthly indicators that may contain useful information about quarterly employment developments are available in a more timely fashion. These monthly indicators, such as unemployment statistics, sentiment indicators or negotiated wages, can be used to predict (or nowcast) quarterly employment growth well before it is officially published.

Nowcasting has been an area of active academic research for the past 15 years (see the seminal contributions of Evans, 2005 and Giannone et al., 2008; and the literature review in e.g. Bańbura et al., 2013, and Hirschbühl et al., 2021) and many policy institutions have implemented models to assess economic activity in real time, exploiting a high-frequency data flow. The target variable of such approaches is typically quarterly GDP, while labour market variables, in particular employment growth, have received much less attention.1 A reason for this could be that many studies and applications focus on the US economy where data on employment, hours worked and hourly earnings are released at monthly frequency with short publication delays. The relative lack of interest in nowcasting quarterly labour market variables for the euro area could also have been due to an assumption that GDP growth is a sufficiently good predictor of employment growth, implying that there is no need to nowcast the latter separately. However, a systemic bias in some official employment forecasts, as well as the developments during the pandemic period – when a severe disconnect arose between GDP growth and labour market variables arose in the euro area (due to policy interventions) – suggest that employment growth is a legitimate nowcasting objective.

To nowcast employment growth and hedge against model uncertainty, in a recent paper (Bańbura et al., 2023) we developed a suite of models, encompassing a variety of bridge equations and dynamic factor models (DFMs), that are well established approaches in the nowcasting literature. The model types are similar to those used for nowcasting euro area GDP growth at the ECB (see Bańbura and Saiz, 2020) and US GDP growth at the Federal Reserve Bank of New York (see Bok et al., 2018). The framework allows exploiting information from indicators at monthly and quarterly frequency released asynchronously, that is with different publication lags. The bridge equations rely on a relatively small number on indicators, that are directly linked to the variable of interest. In case of the DFMs, the variable of interest is driven by a few latent common factors, which can parsimoniously summarise a large information set. We use different model variants within these broad classes (see Bańbura et al., 2023 for details).

In terms of data, we use a range of indicators, including national accounts data such as GDP, monthly activity and labour market indicators such as industrial production and unemployment rate, monthly indicators on nominal developments, such as negotiated wages and sentiment indicators, e.g. the components of the S&P Purchasing Manager Index or the consumer and business surveys of the European Commission. We compile a real-time database, which reflects both the time-pattern of data publications and data revisions (as opposed to pseudo real-time vintages that reflect only the former) and enable a fair comparison to the Eurosystem/ECB Staff macroeconomic projections. Our real-time database includes vintages for two dates in each month: for the 10th – when main monthly labour indicators become available; and for the 25th – around which date the Eurosystem/ECB staff macroeconomic projections are typically finalised (in the second month of each quarter). Feeding our models with these data vintages, we produce the forecast for employment growth for the upcoming two quarters to be released. We evaluate the model-based nowcast in such real-time setting over a sample spanning from 2013 to 2022, including the COVID-19 pandemic period, against a naïve (random walk) and a more ambitious, harder-to-beat benchmark: the quarterly projections produced by Eurosystem/ECB staff.2

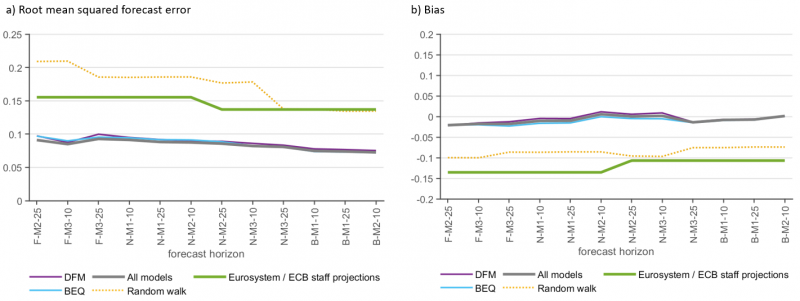

The model suite outperforms the benchmarks both in terms of accuracy (based on the root mean squared forecast error metric) and bias (mean forecast error) in the pre-pandemic (2013-2019) sample (Chart 1). This confirms the usefulness of our approach. Importantly, both the Eurosystem/ECB staff macroeconomic projections and the random walk benchmark were biased downwards, i.e. projected on average lower employment growth than the (final) outcome. In that period, euro area employment growth was found to be stronger than would have been expected for instance using the Okun-relationship (see Botelho and Dias da Silva, 2019). We find that the nowcasting suite is not affected by this, the bias (mean forecast error) is close to zero for all forecast horizons.

Chart 1: Root mean squared forecast error and bias, 2013Q1-2019Q4

Notes: The figure shows the root mean squared forecast errors and the bias (the minus average forecast error) for the bridge equation (blue) and DFM (purple) classes and for the overall average (grey), compared to the Eurosystem/ECB staff macroeconomic projections (green) and random walk forecast (yellow dotted). The x-axis shows the different forecast horizons, where F, N and B stand for forecast (prepared in the quarter preceding the reference quarter), nowcast (prepared in the reference quarter) and backcast (prepared in the quarter following the reference quarter), respectively. M1, M2 or M3 refer to the month within the quarter and 10 and 25 to the day of the month on which the forecast was obtained. The root mean squared forecast error and the bias are calculated against the last release of the data, which was downloaded on 25th January 2023.

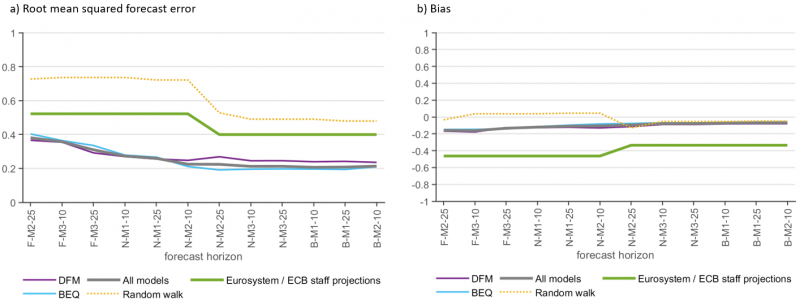

The performance of the model suite worsens temporarily during the period affected by the COVID pandemic, but improves again considerably thereafter, without any adjustment in the model setups. The performance loss is due to the pandemic and the related lockdowns which introduced unprecedented volatility in many activity and labour market variables. In addition, the large-scale use of job retention schemes in the euro area severely distorted the relationship between labour market and economic activity indicators. These factors influence the stability of the (estimated) relationships between the variables, the size of the residuals in our models and consequently the models’ forecasting performance. Several papers discuss the issues and possible remedies for nowcasting and other time series models (see e.g. Lenza and Primiceri, 2022, Antolin et al., 2021, Carriero et at., 2022, Ng, 2021, Schorfheide and Song, 2023, Bobeica and Hartwig, 2023). Not surprisingly, our model suite doesn’t predict well employment developments in the first couple of quarters affected by the pandemic shock. At the same time, the accuracy of the Eurosystem/ECB Staff macroeconomic projections worsens comparatively less for the second half of 2020, due to an approach that is less mechanical and leaves more room for expert judgment, and in particular for incorporating the effects of the job retention schemes. However, the performance of the model suite improves considerably after the start of 2021 and gains back its performance edge against both benchmarks (Chart 2).

Chart 2: Root mean squared forecast error and bias, 2021Q1-2022Q3

Notes: see Notes to Chart 1.

In normal times, the models relying on a large set of data (DFMs) and the smaller scale models (bridge equations) perform similarly. This suggests that during normal periods, unemployment statistics and sentiment indicators included in the bridge equations appear to contain most of the relevant information to nowcast employment growth.

However, the pandemic shock – during which the DFMs performed better – highlights the benefit of averaging over a multitude of approaches. While none of the models could provide meaningful nowcasts for the most heavily affected quarters during the pandemic (from 2020Q2 to 2020Q4), the performance of the bridge equations that include lagged GDP growth deteriorated most strongly (for reasons explained above). Between the two model classes, the DFM class seems to have performed relatively better during the pandemic period than the bridge equation class and thus provided some hedge against extreme volatility. Using different models and relying on model averaging thus has its largest advantage in such volatile periods. Since 2021, the disagreement of the forecasts has declined and all models performed in a relatively accurate way in the seven quarters that we evaluated (for more details, see Bańbura et al., 2023).

Antolin-Diaz, J., Drechsel, T., and Petrella, I. (2021). Advances in nowcasting economic activity: Secular trends, large shocks and new data. CEPR Discussion Papers 15926, C.E.P.R. Discussion Papers.

Bańbura, M., Giannone, D., Modugno, M., and Reichlin, L. (2013). Nowcasting and the real time data flow. In Elliott, G.and Timmerman, A., editors, Handbook of Economic Forecasting, pages195–237. North Holland.

Bańbura, M. and Saiz, L. (2020). Short-term forecasting of euro area economic activity at the ECB. ECB Economic Bulletin, Issue 2/2020, European Central Bank. ECB Working Paper Series No 281521.

Bańbura, M., Belousová, I., Bodnár, K. and Tóth, M. (2023): Nowcasting employment in the euro area, ECB Working Paper, No. 2815.

Bobeica, E. and Hartwig, B. (2023). The COVID-19 shock and challenges for inflation modelling. International Journal of Forecasting, 39(3): 519–539.

Bok, B., Caratelli, D., Giannone, D., Sbordone, A. M., and Tambalotti, A. (2018). Macroeconomic nowcasting and forecasting with big data. Annual Review of Economics, 10(1): 615–643.

Botelho, V. and Dias da Silva, A. (2019): Employment growth and GDP in the euro area, ECB Economic Bulletin, Issue 2/2019.

Carriero, A., Clark, T. E., Marcellino, M., and Mertens, E. (2022). Addressing COVID-19 Outliers in BVARs with Stochastic Volatility. The Review of Economics and Statistics, pages 1–38.

Consolo, A., Foroni, C., and Martínez-Hernández, C. (2023). A mixed frequency BVAR for the euro area labour market. Oxford Bulletin of Economics and Statistics.

Evans, M. D. D. (2005). Where are we now? real-time estimates of the macroeconomy. International Journal of Central Banking, 1(2).

Giannone, D., Reichlin, L., and Small, D. (2008). Nowcasting: The real-time informational content of macroeconomic data. Journal of Monetary Economics, 55(4):665–676.

Hirschbühl, D., Onorante, L., and Saiz, L. (2021). Using machine learning and big data to analyse the business cycle. ECB Economic Bulletin, Issue 5/2021, European Central Bank.

Karagedikli, O. and Özbilgin, M. (2019). Mixed in New Zealand: Nowcasting labour markets with MIDAS. Analytical Note Series 04, Reserve Bank of New Zealand.

Lenza, M.and Primiceri, G. E. (2022). How to estimate a vector autoregression after March 2020. Journal of Applied Econometrics, 37(4): 688–699. ECB Working Paper Series No 281523.

Ng, S. (2021). Modeling macroeconomic variations after Covid-19. NBER Working Papers 29060, National Bureau of Economic Research, Inc.

Schorfheide, F.and Song, D. (2023). Real-time forecasting with a (standard) mixed-frequency VAR during a pandemic. International Journal of Central Banking, forthcoming.

There are a few papers that have a similar objective, see for example Karagedikli and Özbilgin (2019) and Consolo et al. (2023).

The quarterly Eurosystem/ECB staff macroeconomic projections are derived as aggregations of country-level projections and include a large amount of information processed via different models and expert judgement. For this reason, they can be considered as a benchmark not easy to beat. The quarterly employment growth profiles of the Eurosystem/ECB staff projections are not available publicly.