Banks’ domestic sovereign exposures in the euro area ballooned during the financial and European debt crises but have markedly declined since then. Still, with 5% of total assets and 76% of capital, they remain considerable and a risk on bank balance sheets, especially in light of the general exemption from capital requirements and concentration limits. Risk parameters differ between national banking markets, and the home bias remains high, at around 80%, as banks hardly diversify into other euro-area debt. The cross-country differences make it difficult for policymakers to agree on a fully mutualized European Deposit Insurance Scheme and thus complete the Banking Union.

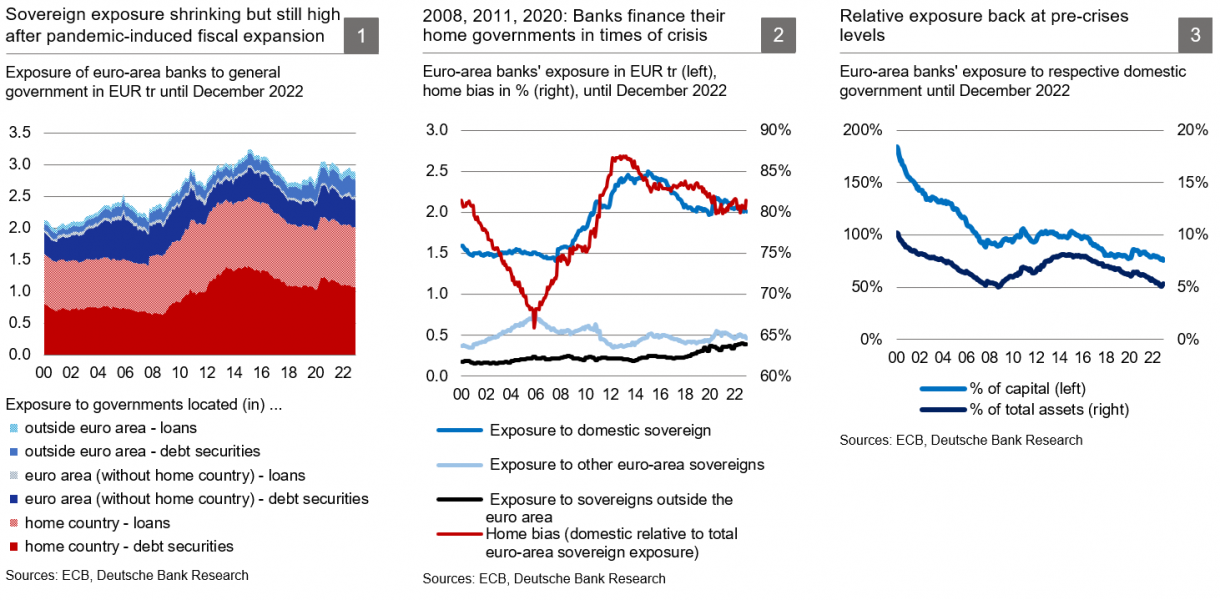

Rising energy price inflation has led many governments to adopt far-reaching measures over the past year to help households and companies shoulder the higher bills. So far, actual outlays in the euro area have been moderate, also helped by the recent strong gas price decline. But, given that many relief measures will only be paid out in the course of this year, public expenditures could rise more pronouncedly. How will they be financed? Especially since the ECB has stopped being a net buyer of government bonds. So far, by and large, this has not come through the balance sheets of euro-area banks. By contrast, banks considerably increased their funding to home governments during previous crises.

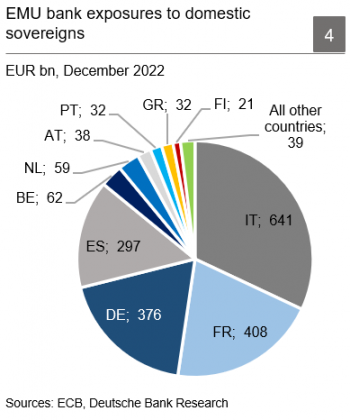

Indeed, banks’ funding of their domestic sovereigns ballooned during the financial and European debt crises. Since then, though, euro-area banks have slowly but markedly reduced their exposure. Also, they have moderately decreased their holdings of other euro-area government debt. By contrast, they have expanded into non-EMU, i.e. “foreign” debt. The trend of declining domestic exposure was temporarily reversed when banks absorbed a substantial share of debt issued by national governments in early 2020 to finance pandemic-related expenditures. Although the absolute level of home sovereign bonds and loans is still elevated compared to total assets and capital, they have fallen to the pre-crisis ratios of 2008 and below (Chart 3). From a financial stability perspective, this is good news, but with 5% of total assets and 76% of capital, exposure remains considerable and a risk on bank balance sheets, especially considering the general exemption from capital requirements and concentration limits.

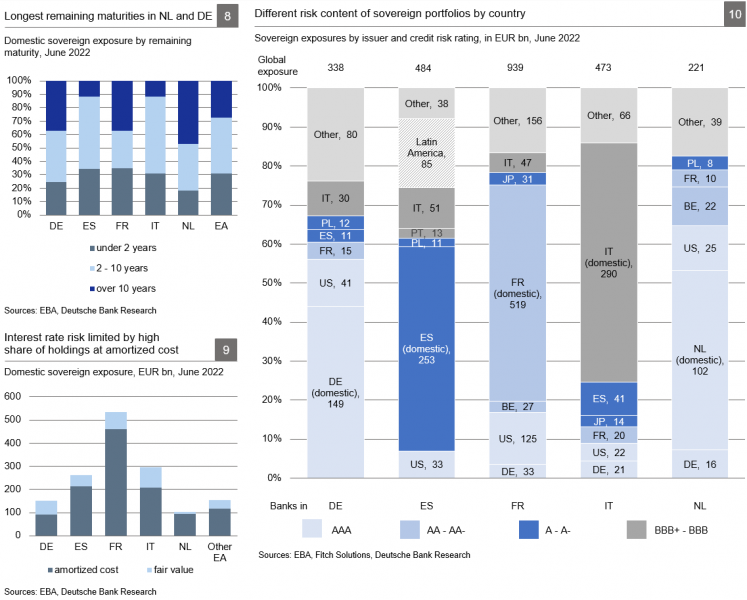

While the euro-area banking sector as a whole has been shrinking the domestic sovereign portfolio, there are considerable differences between countries. Among the five largest markets (totalling 80% of banking assets), German banks have reduced their home sovereign exposure the most, in absolute terms, since 2015 (by EUR 199 bn). They are followed by Dutch, Spanish and Italian banks (whose exposures are all down by EUR 30-45 bn), whereas French banks have actually increased their holdings slightly.

In relative terms, a few ratios are particularly important:

The risk profiles of the domestic sovereign exposures also differ, particularly with regard to remaining maturities, as shown by the latest EBA Transparency Exercise.1 Almost half of Dutch banks’ holdings are long term, i.e. have a maturity of over 10 years, compared to about one-third for French and German banks. In Italy and Spain, such claims account for only 12% of the portfolio. When it comes to interest rate risk, accounting determines if a bank’s bottom line will be hit straight on: sovereign exposures are either valued at amortized cost or at fair value, depending on what for and how long the bank intends to stick to that position. Dutch banks are the most protected against losses from rising interest rates. They hold only 6% of their sovereign debt2 at fair value. For French and Spanish banks, this share is also low at 14% and 18%, respectively. Italian banks value 30% at fair value and German banks 39%. Spanish and Italian banks have considerably lowered their fair-value exposure since 2019, before the pandemic, and they now hold a higher share at amortized cost, reducing the risk of devaluations in the case of falling prices. However, larger holdings at amortized cost can lead to higher unrealized mark-to-market losses on debt securities when interest rates rise, which can trigger investor concern if such portfolios suddenly need to be sold, as happened recently with some regional banks in the US.

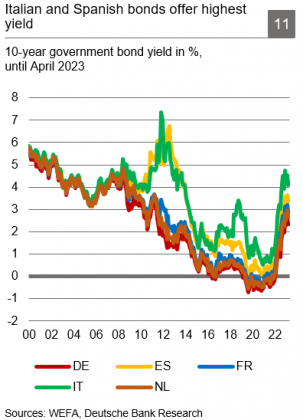

Credit risk ratings3 for sovereign debtors range from AAA (Netherlands, Germany), AA (France) and A- (Spain) to BBB (Italy). This implies different risk-return levels for banks. Since 1999, the European Monetary Union has allowed them to diversify into other euro-area sovereign paper without incurring foreign exchange risk or the obligation to risk-weigh the exposure. But banks across Europe have preserved their preference for home government debt and the associated risk-return profile. Moreover, the holdings of other sovereign debt seem to reflect to a considerable extent the location of banks’ non-domestic subsidiaries rather than pure investment decisions.

There is more than one reason for the persisting home bias. i) Probably, loans are part of the answer. Bank loans, which account for almost half of domestic exposure, are mainly used by local and state authorities and are often granted by banks with a local presence. ii) Domestic banks might be the government’s preferred market makers. iii) Moral suasion and closer personal connections between public and financial decisionmakers could play a role. iv) In some countries, higher yields simply make national debt more attractive.

The direct financial link between banks and governments creates a strong interdependence. This so-called sovereign-bank nexus is tightened further by the concurrent dependence of both sectors on the wellbeing of the general economy. Although there is a benign side to this nexus as domestic banks can provide governments with quick access to funding like at the onset of the coronavirus pandemic, it can also turn out to be a doom loop as experienced during the European debt crisis. On the one hand, sovereign downgrades and rising borrowing costs caused losses in banks’ bond portfolios. On the other hand, weak banks needed government support which let public finances deteriorate. Finally, this required several European rescue programmes.

While most measures to prevent financial stress from spreading from banks to public finances were implemented years ago – the Single Rule Book, the Single Supervisory Mechanism and the Single Resolution Mechanism – the last building block of the EU “Banking Union” is still missing: the proposed European Deposit Insurance Scheme (EDIS). The initiative has been stuck in political deadlock, although “a fully-fledged EDIS remains the most comprehensive way to address the component of the bank-sovereign nexus that is channelled through reliance on national DGS schemes [deposit guarantee schemes], which are underpinned by explicit or implicit sovereign guarantees.”4 Some EMU countries wanted to implement EDIS quickly, whereas others pointed at different risk levels in the individual banking markets and called for reducing risks before mutualizing deposit insurance across the euro area. In this context, the focus has been on non-performing loans for a long time. But NPLs have declined considerably over the past decade, and national ratios have started to converge.5

Risks arising from bank exposures to their domestic sovereigns, though, are still an issue waiting for a political agreement. Sizable cross-country differences remain as regards amount, structure and riskiness, as shown above. This leaves policymakers with no easy solutions when finishing the Banking Union. The hope has not materialized that if banks share the same rules, supervision, and currency, they will decouple from domestic sovereigns by diversifying their euro-area debt. Chances are indeed that the home bias will rise again with higher public expenditures this year.

EBA (2022), 2022 EU-wide transparency exercise, December 9. It reports risk-related data for a sample of large European banks representing about 80% of the market. However, the coverage of different national markets varies, e.g. it is ca. 98% in France, but only 44% in Germany. Results are based on cross-border consolidated group balance sheets and use banks’ supervisory reports. By contrast, previously discussed balance sheet data published by the ECB is based on standard statistical reporting and includes all banks. For more details, please refer to Mai, Heike (2021). What to do with home sovereign exposure?, March 22, p. 5 & 10-11.

Debt refers to both bonds and loans.

Proprietary material of Fitch Solutions.

Makhlouf, Gabriel (2023). Has Europe moved beyond financial fragility?, Opening remarks at a public event at the Hertie School, Berlin, February 14.

On April 18, 2023, the European Commission proposed a reform of the Crisis Management and Deposit Insurance framework (CMDI) to better protect depositors and align national practices. While EDIS is different, on that occasion, the Commission argued again for its introduction.

ECB Banking Supervision, supervisory banking statistics.