This brief should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

This paper provides a chronology of the main financial events over the last 15 years, spanning three main crises. The first is the global financial crisis in 2008-09, and the second is the euro area sovereign debt crisis in 2010-12. Both events heralded significant reforms of the EU’s governance and financial architecture. On the tail of these two crises, the ongoing COVID-19 crisis that started in early 2020 enables us to assess the working of the resulting financial framework. Two aspects stand out. The first is that the coronavirus crisis was, in its origin, exogenous from previous banking sector behaviours -which was not the case during the 2008-2012 period. The second aspect stems from the combined policy responses to the pandemic, which lacked in the 2008-2012 period. Against this background, the aim of this paper is twofold. The first is to highlight the sequence of regulatory and institutional changes, with a focus on the ECB and Eurosystem, vis-à-vis the unfolding events and against the background of broader financial reforms. The second aim of this paper is to investigate whether the sequence of financial reforms has improved the sector’s ability to deal with major macro-financial shocks at the EU/euro area level, reducing the sovereign-bank doom loop. We focus primarily on developments affecting the banking sector, while noting that during the same period major developments within the EU non-bank financial sector were observed. The COVID-19 crisis has been characterized by the positive interaction of rapid fiscal and monetary responses (macro polices), and joint financial and supervisory responses. In this new policy environment the message of the paper is that the sequence of financial reforms, including the acquisition of supervisory and financial stability tasks by the ECB, have been instrumental in facilitating the effective response to the COVID-19 crisis thus far, especially compared to the previous two crises. The increased resilience and resolvability of the EU banking sector has enabled it to withstand the large and unexpected pandemic shock, while continuing to finance the real economy.

In February 2020 the SARS-CoV-2 virus started one of the most dramatic periods in the history of the EU and the euro area. The massive economic dislocations that the coronavirus (COVID-19) pandemic caused in production, trade, investment, employment and consumption were also observed in the financial systems. Systemic financial stress (as measured through diverse indicators) immediately became more acute and an incipient process of financial re-fragmentation emerged, driven, among others, by expected large fiscal burdens, a return of diverse risk premia and a concern that cross-country differences in crisis response could distort the competitive environment. The rapidity of the combined policy responses, through monetary and supervisory initiatives, and fiscal measures (national, and then European) immediately stood out.

In recent work1, we look at the ongoing COVID-19 crisis in comparison with the global financial crisis in 2008-09 and the euro area sovereign debt crisis in 2010-12. These crises generated longer financial disruptions and dislocations. In response, they were followed by financial reforms, such as the Single Rule Book, Basel III, the European System of Financial Supervision (ESFS), the Single Supervisory Mechanism (SSM) and the Single Resolution Board (SRB). Thus, the COVID-19 crisis enables us to assess whether this sequence of reforms of the financial framework has had its intended impact by reducing the sovereign-bank doom loop and improving the overall resilience and resolvability of the EU banking sector.

We ask whether the financial system has been able to withstand the ongoing large, unexpected macro-financial shock while continuing to finance the economy. The answer is affirmative, but there are nuances. There is evidence that past financial reforms have been instrumental in facilitating the combined policy responses (that were absent in the previous crises). Yet several concomitant factors also played a role, including massive government programmes geared towards alleviating the shocks hitting households and corporates and thus facilitating the credit flow during the most acute phases of the pandemic.

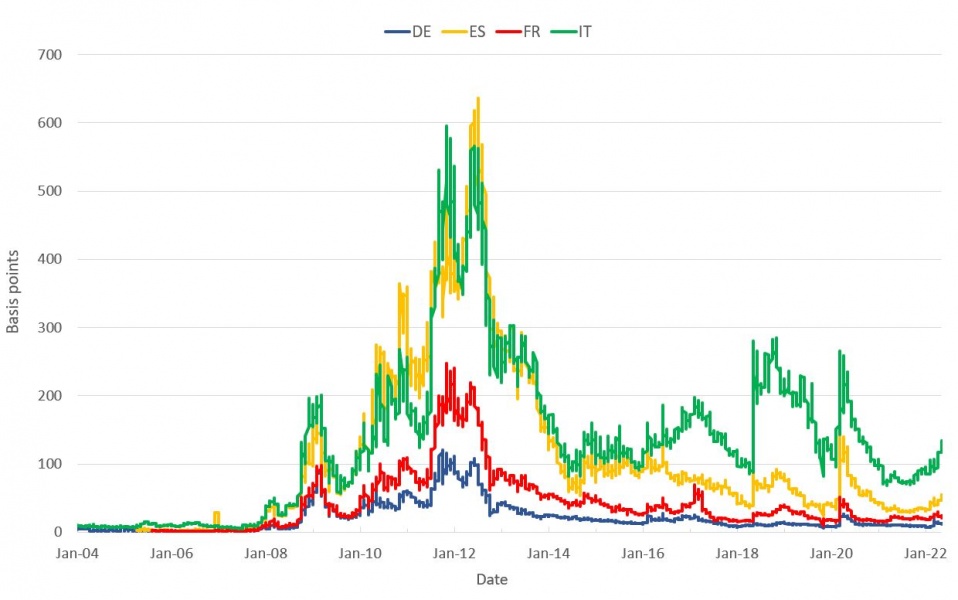

Indeed, indicators of financial distress suggest that, in spite of the unprecedented shock to the economy caused by the pandemic and associated lockdowns, markets quickly calmed down and the effects on most asset prices were somewhat muted, or at least short lived. For instance, while the CISS indicator2 (Chart 1) and the CDS spreads of euro area banks (Chart 2) sharply increased in the early stages of the COVID-19 crisis (March-April 2020), they soon returned to more normal levels. This contrasts with both more severe and more persistent stress in the euro area financial sector during the global financial crisis and throughout the euro area sovereign debt crisis. As shown in our paper, this finding is corroborated also by other financial and banking sector indicators. This suggests that the concerted mitigating actions by the fiscal, monetary and prudential authorities were highly effective.3

Chart 1: CISS indicator (daily)

Sources: ECB and ECB calculations.

Chart 2: Euro area bank CDS spreads (daily, basis points)

Sources: ECB and ECB calculations.

The COVID-19 crisis was also a litmus test of the resilience of the European banking supervision. The aim of setting up a new financial regulatory framework was to create a level playing field for banks operating in the euro area, breaking the nexus between banks and their sovereigns.

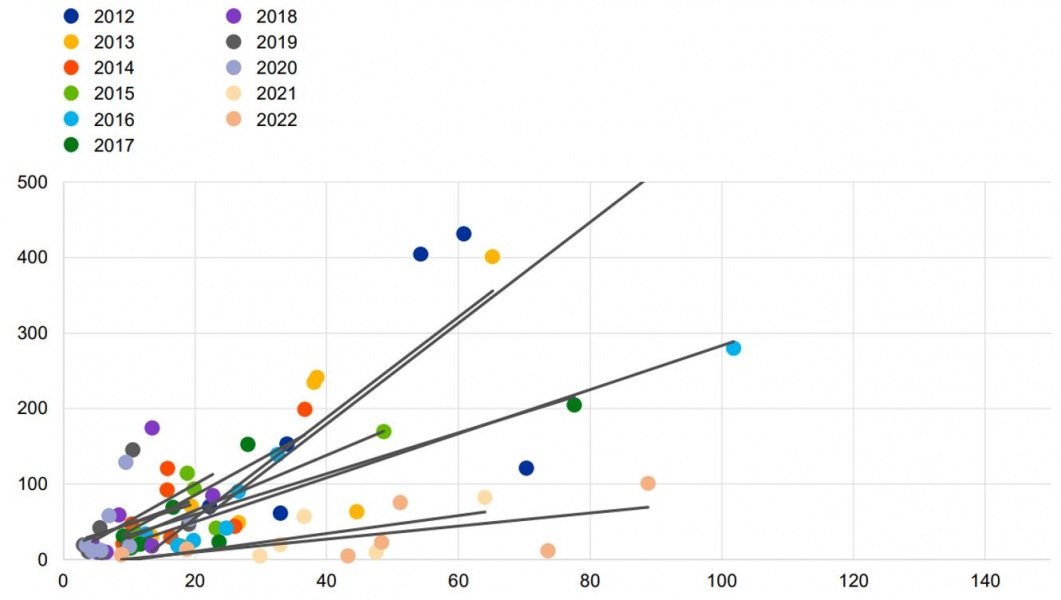

A clear indication that the EU’s new financial architecture, underpinned by the banking union in particular but also clearly by the extensive monetary policy accommodation, has helped break the link between bank funding costs and those of their sovereign is shown in Chart 3. It can be observed that the relationship between bank and sovereign CDS spreads over time has become much less pronounced since 2015. This evidence speaks in favour of an effective conduct of the ECB’s supervisory tasks and its operational independence from political pressure, which had been one of the goals and arguments for entrusting the central bank with micro-prudential supervision.

Chart 3: CDS spreads of banks and sovereigns in the SSM area – by year (x-axis: bank CDS spreads; y-axis: sovereign CDS spreads; basis points)

Sources: ECB and ECB calculations. Notes: Banks’ CDS prices are shown as value-weighted averages per country and year for the list of significant institutions directly supervised by the ECB, as published in May 2021. The dotted lines reflect the trendline for each year.

The pandemic is the first systemic crisis faced by the SSM since its inception in 2014. Before its launch, banking sector crisis management was largely confined within national borders. This time around, a coordinated euro area/SSM-wide response was possible.

The descriptive evidence in the paper suggests that the SSM navigated this first real systemic crisis, and although this does not allow firm conclusions to be drawn on causality, it does corroborate findings from other studies:

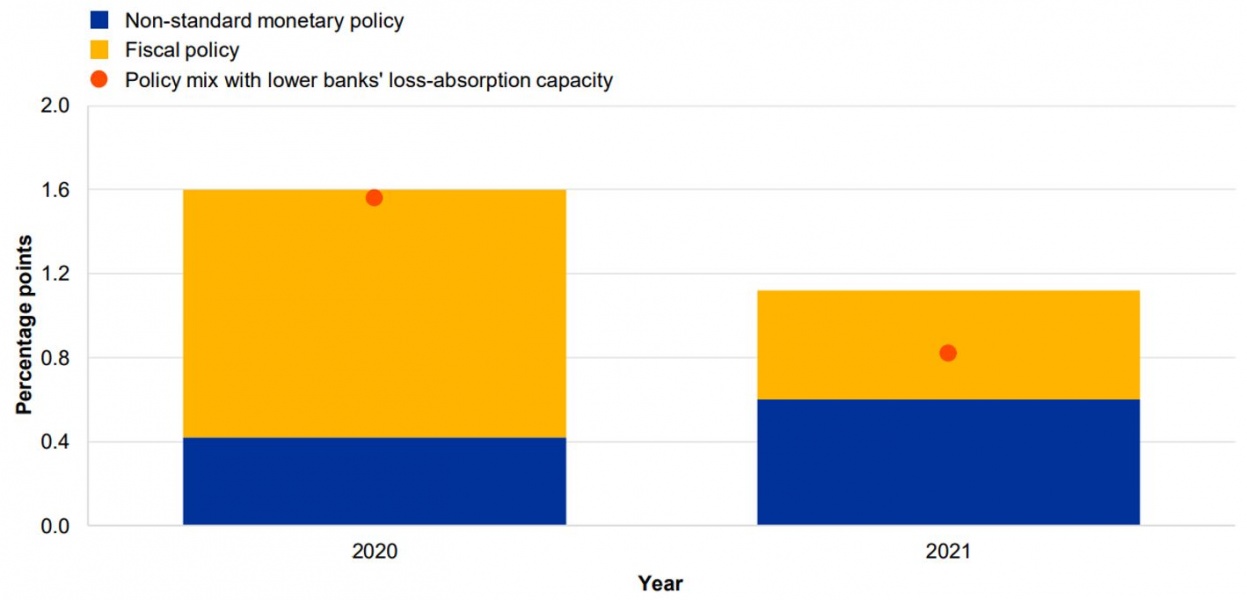

The bank capital build-up supported by regulatory reforms after the global financial crisis and SSM implementation (incl. the regular stress tests) significantly improved the resilience of most banks. If bank capital had been more constrained in the run-up to the pandemic, the impact of mitigating supervisory measures might have been more modest and less effective and the same fiscal and monetary policy impulse might have yielded a smaller expansionary effect as indicated by the red dots in Chart 4 (see also Darracq et al., 2020).

Chart 4: Model-projected real GDP growth (percentage point deviation from the baseline)

Sources: Darracq Pariès, Kok and Rancoita (2020), box in the May 2020 ECB Financial Stability Review. Simulations based on Darracq Pariès et al. (2011, DKR model). Notes: The illustrative fiscal policy response abstracts from the effect of automatic stabilisers and off-budget items such as state guarantees on loans. The policy mix simulation with lower bank loss-absorption capacity evaluates the same fiscal and non-standard monetary policy measures but assumes tighter bank capital constraints so that banks would resist any temporary decline in net interest income through less accommodative lending policies.

Overall, the COVID-19 crisis has been characterized by the positive interaction of rapid fiscal and monetary responses, as well as joint financial and supervisory responses. In this new policy environment, we argue that the sequence of institutional financial reforms, including the acquisition of supervisory and financial stability tasks by the ECB, has been instrumental – with a timely and appropriate policy mix – in providing an effective response to the COVID-19 crisis, especially compared to the previous two crises. Concerted policy responses to the pandemic helped contain the financial and real economic impact of the crisis and while monetary and fiscal policies were the first line of defence against the real economic fallout from the pandemic, the ability of the SSM to coordinate and implement a swift and meaningful policy response helped mitigate the risk of procyclical real economic amplification effects from the financial sector. This strengthened speed of reaction was also witnessed more recently in the context of the Russian invasion of Ukraine which triggered concerted supervisory responses and enhanced monitoring efforts across the SSM system (see ECB, 2022).

Altavilla, C., Boucinha, M., Peydró, J.L. and Smets, F. (2020), “Banking supervision, monetary policy and risk-taking: big data evidence from 15 credit registers”, Working Paper Series, No 2349, European Central Bank, Frankfurt am Main, February.

Ampudia, M., Beck, T., Beyer, A., Colliard, J.-E., Leonello, A., Maddaloni, A. and Marques Ibanez, D. (2019), “The architecture of supervision”, ECB Working Paper Series, No 2287.

Darracq Pariès, M., Kok, C., Rodriguez Palenzuela, D. (2011), “Macroeconomic propagation under different regulatory regimes: Evidence from a DSGE model for the euro area”, International Journal of Central Banking, Vol. 7, No 4, pp. 49-113.

Darracq Pariès, M., Kok, C. and Rancoita, E. (2020), “Macroeconomic impact of financial policy measures and synergies with other policies”, Financial Stability Review, European Central Bank, May.

European Central Bank (2022), “Supervisors’ reaction to the war in Ukraine”, ECB Supervision Newsletter.

Haselmann, R., Singla, S. and Vig, V. (2022), “Supranational Supervision”, working paper.

Hobelsberger, K., Kok, C., and Mongelli, F.P. (2022a), „A tale of three crises: synergies between ECB tasks”, ECB Occasional Paper No. 305.

Hobelsberger, K., Kok, C., and Mongelli, F.P. (2022b), „Is this time different?: synergies between ECB tasks”, in Central Banks and Supervisory Architecture: Lessons from Crises in the 21st Century (eds. Holzmann, R. and Restoy, F.), Edward Elgar Publishing.

Hoffmann, P., Kremer, M. and Zaharia. S. (2019), “Financial integration in Europe through the lens of composite indicators”, ECB Working Paper Series, No 2319.

Kok, C., Muller, C., Ongena, S. and Pancaro, C. (2021), “The disciplining effects of supervisory scrutiny in the EU-wide stress tests”, ECB Working Paper Series No 2551.

Kremer, M., Lo Duca, M. and Holló, D. (2012), “CISS – a composite indicator of systemic stress in the financial system”, ECB Working Paper Series, No 1426.

Maddaloni, A. and Scopelliti, A.D. (2019), “Rules and Discretion(s) in Prudential Regulation and Supervision: Evidence from EU Banks in the Run-Up to the Crisis”, ECB Working Paper Series, No 2284.

See Hobelsberger et al. (2022a-b).

The CISS aims to measure the current state of instability in the financial system as a whole or, equivalently, the level of “systemic stress”. See Kremer et al. (2012) and Hoffmann et al. (2019).

The CISS indicator also exhibits a spike in the aftermath of the Russian invasion of Ukraine; however, still well-below the levels of previous crisis episodes.