The views expressed in this column present the authors’ personal opinions and do not necessarily reflect the views of the European Central Bank, de Nederlandsche Bank, or the Eurosystem. This contribution has also been published as a Vox.eu column.

Many central banks have strengthened their communications with the public recently, to strengthen accountability and to create trust, but also to guide inflation expectations. Based on a review of the relevant literature, we argue that communicating effectively with the general public is fraught with difficulties, but carries at least some promise.

Following the great inflation of the 1970s, central banks in many countries were made independent from their governments, a development that is currently not entirely uncontested (Issing 2018). Central bank independence carries with it an obligation to be accountable, both to the legislature and to the general public. This need for accountability has been exacerbated by—among other things—the (often controversial) public debate about the role of central banks in the financial crisis and in the COVID-19 recession, changes in central bank mandates, and new and more complex monetary policy tools. Realising this, many central banks have substantially strengthened their efforts to communicate with the general public. These efforts are mostly new since, traditionally, central banks have targeted their communications at financial markets (Istrefi et al. 2022).

But effective communication requires both a sender and a receiver, and most of the public has both limited knowledge and a low desire to be informed about central bank issues (van der Cruijsen et al. 2015). Central bank efforts to communicate with the general public often do not reach the intended recipients. People are often not aware of where inflation is, have biased inflation expectations (Weber 2022), do not know the central bank’s inflation target (Coibion et al. 2019), and display limited understanding of monetary policy strategies (Coibion et al. 2020). In line with this, former ECB policymakers see substantial room for improvement in communication with the general public (Ehrmann et al. 2022).

As central bank efforts to communicate with the general public have escalated, so also has the related scholarly literature on the topic. Around 15 years ago, we observed that “nearly all the research to date has focused on central bank communication with financial markets. It is time to pay more attention to communication with the general public.” (Blinder et al. (2008).) This picture has changed drastically since then, leading us to review and synthesise this new literature in Blinder et al. (2022). This review is organised around a series of questions.

Central banks increasingly motivate their communications with the general public as a way to enhance public trust. The literature shows that low trust can have harmful repercussions for the central bank—by weakening the transmission of monetary policy, but also in the political sphere by attracting more political commentaries and ultimately threatening independence. However, while trust matters, it is not straightforward for central bankers to foster trust in their institutions. For example, it cannot be taken for granted that more transparency and more communication enhance trust. Measuring trust remains difficult. And trust is to some extent determined by factors that are only partially under central banks’ control—such as trust in institutions more generally, broader economic performance, or problems in the banking sector. All this leads us to conclude that gaining trust, though vital, is hard. However, increasing trust does pay off: the inflation expectations of people who have more trust in the central bank are closer to the central bank’s target than those of people who have less trust.

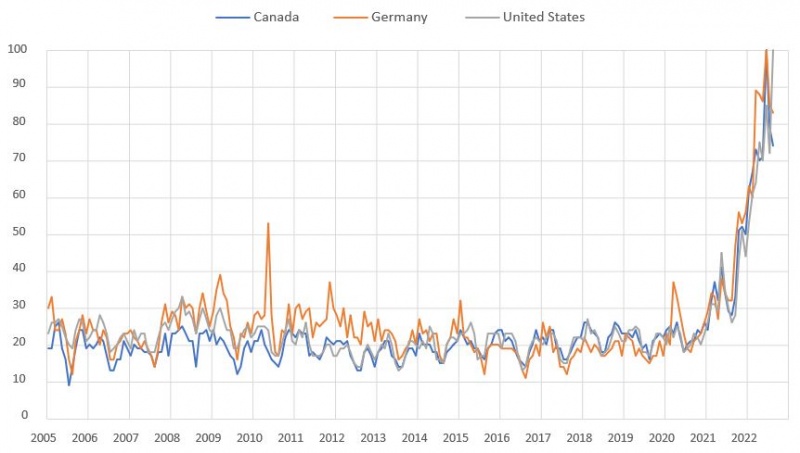

Central banks communicate with the public through various channels, such as outreach on web sites, financial and economic education, presence on social media, and the organisation of listening events. But do these efforts actually reach the public? Households and nonfinancial businesses might choose to be rationally inattentive, especially if they have experienced long histories of low and stable inflation. In that sense, successful monetary policy breeds inattention. Figure 1 shows that there was indeed little public interest in inflation for many years while inflation was persistently below central banks’ targets. But inflation received immediate attention as soon as it went above the central banks’ targets for some time. Today, central banks are well advised to reach out to the public and explain that they are in charge of controlling inflation, at what levels they see inflation stabilising, and what it takes to get there.

Figure 1: Searches for inflation on Google

Sources: Google trends. The chart reports the number of searches on Google for the term Inflation, originating in the different countries. The data for each country are normalized to 100 at the country-specific peak. Sample period: January 2005 – August 2022.

But getting through to people is not straightforward. It requires the help of media, especially television and newspapers (which are still the main channels through which people receive information about monetary policy), because the central bank can only partially influence the tone and the extent of the reporting. Also, the banks must use simpler language than the highly complex communications with expert audiences that they are accustomed to (Bulíř et al., 2013). While doing so puts central banks outside their comfort zone, there is promising evidence that efforts to speak in clearer prose might pay off.

Our take is therefore that the wider public is potentially reachable by central banks—but not easily. More effective outreach requires that central banks make it less costly to acquire the relevant information. It also helps if the public understands the benefits of being informed about central banking issues. Periods of heightened attention to central banks, such as the recent increase in inflation, require more communication by central banks, anyway. But they also provide useful opportunities to reach out while people are listening.

For communication to have impacts, central bank signals must not only be received, they also need to be understood by the recipients. The empirical evidence shows that there is a long way to go here. Public knowledge about key aspects of monetary policy (such as its objective or the level of the inflation target) is fragmentary at best, especially among less educated, low-income, or younger citizens. One could argue that some groups are simply unreachable, and therefore efforts should be concentrated on those that already have a basic understanding. But an alternative conclusion is that a lot can be gained by tailoring communications to the groups with the lowest levels of knowledge, in the hope of raising their understanding a bit.

Central banks may also communicate with the public to enhance the effectiveness of monetary policy. Up to now, almost all central bank communication efforts for that purpose have been targeted at the traditional audiences—financial markets and other experts. But better communication with the broad public could also make monetary policy more effective by, for example, influencing the inflation expectations of households, wage earners, and businesses.

Regarding inflation expectations, central banks might want to pursue two objectives: to anchor long-term expected inflation near the inflation target and to influence short-term expected inflation over the monetary policy cycle, i.e., lowering it when tightening and increasing it when easing. The first objective is more straightforward, but even here, central banks have a long way to go. Consumer expectations are known to be biased upward and inefficient, and it’s not clear that businesses do much better. That said, several studies report that inflation expectations are better anchored if people have better knowledge about monetary policy, and if they receive information about the central bank’s target, its inflation forecast, or its policy instruments. Moving inflation expectations consistently with monetary policy cycles seems even more difficult. Monetary policy decisions largely go unnoticed, or do not move inflation expectations, and households often take a view of inflation that experts would characterise as stagflationary, namely interpreting higher inflation as bad news about their real incomes. As a result, households that expect higher inflation may lower their spending rather than raise it.

Taken together, these considerations suggest that central banks must design their communication strategies carefully—to generate understanding, not misunderstanding. One challenge is to ensure consistency between the simpler messages geared toward the general public and the more nuanced messages targeted at expert audiences. Inconsistent messages not only risk confusion, they might even degrade the well-established communication with experts.

There is often a trade-off between accuracy and simplicity. Central banks may reach households better by communicating in simpler ways and with shorter messages. However, if they get too simple and short, they may generate a false sense of precision and certainty and even undermine trust if actual developments differ from the central bank’s messages.

Overall, we conclude that the potential benefits from more and better central bank communication with the general public are important enough that central bankers should keep trying to achieve them. Perhaps the largest benefits from central bank communication with the general public accrue when the central bank explains its role clearly and clarifies its objectives. Wouldn’t it be nice if the citizenry at least understood that control of inflation was monetary policy’s principal job, that interest rates are its principal instrument, and that raising interest rates is the way to fight inflation? We argue that this is where central banks should focus their attention first—and where they might have some success.

Blinder, A., J. de Haan, M. Ehrmann, M. Fratzscher and D. Jansen (2008). What we know and what we would like to know about central bank communication. VoxEU, https://cepr.org/voxeu/columns/what-we-know-and-what-we-would-know-about-central-bank-communication.

Blinder, A., M. Ehrmann, J. de Haan and D. Jansen (2022). Central Bank Communication with the General Public: Promise or False Hope?. CEPR Discussion Paper No. 17441.

Bulíř, A., M. Cihák and D. Jansen (2013). Measuring the clarity of central-bank communication. VoxEU, https://new.cepr.org/voxeu/columns/measuring-clarity-central-bank-communication.

Coibion, O., Y. Gorodnichenko and M. Weber (2019). Monetary policy communications and their effects on household inflation expectations. VoxEU, https://cepr.org/voxeu/columns/monetary-policy-communications-and-their-effects-household-inflation-expectations.

Coibion, O., Y. Gorodnichenko, E.S. Knotek II and R. Schoenle (2020). Average inflation targeting and household expectations. VoxEU, https://cepr.org/voxeu/columns/average-inflation-targeting-and-household-expectations.

Ehrmann, M., S. Holton, D. Kedan and G. Phelan (2022). Views on monetary policy communication by former ECB policymakers. VoxEU, https://cepr.org/voxeu/columns/views-monetary-policy-communication-former-ecb-policymakers.

Ter Ellen, S., V.H. Larsen and L.A. Thorsrud (2020). Narrative monetary policy surprises and the media: How central banks reach the general public. VoxEU, https://voxeu.org/article/narrative-monetary-policy-surprises-and-media.

Issing, O. (2018). The uncertain future of central bank independence. VoxEU, https://cepr.org/voxeu/columns/uncertain-future-central-bank-independence.

Istrefi, K., F. Odendahl and G. Sestieri (2022). ECB Communication and its Impact on Financial Markets. SUERF Policy Brief 306. ECB Communication and its Impact on Financial Markets.

van der Cruijsen, C.A.B., D. Jansen and J. de Haan (2015). What the general public knows about monetary policy. VoxEU, https://cepr.org/voxeu/columns/what-general-public-knows-about-monetary-policy.

Weber, M. (2022). Subjective inflation expectations of households and firms. SUERF Policy Brief 365. Subjective inflation expectations of households and firms.