The expectations of households and firms determine virtually all forward-looking choices actual decision makers do. Inflation expectations take a special role, because they shape households consumption and savings decisions (D’Acunto et al, 2022a), households wage bargaining and labor supply (D’Acunto et al, 2022b), but also the investment and leverage choices (Hackethal et al. 2022 a,b). On the firm side, inflation expectations shape managers’ investment, hiring, and price setting decisions (Weber et al, 2022). A leading explanation for realized inflation dynamics, the New Keynesian Philipps Curve, also prescribes an important role to inflation expectations. Hence, it is not surprising that policymakers watch them closely and Jerome Powell (2021) recently argued, “Inflation expectations are terribly important. We spend a lot of time watching them.” Yet, for many decades after the rational expectations revolution, academic economists had lost interest in studying how actual decision makers form expectations, because the model directly implied the expectations of the representative agent. Moreover, traditionally, central banks typically focus on the inflation expectations of professional forecasters and financial markets. However, it is households and firms in our models whose decision central banks aim to influence and empirically, inflation expectations are dispersed, upward biased relative to ex-post realized inflation, and systematically related to characteristics of households and firms (D’Acunto et al, 2021a,b, forthcoming). In this brief, I review the recent, growing body of work that documents stylized facts on the formation of subjective inflation expectations, their determinants, and how they shape real decisions. I will focus on households but argue at the end that most points apply equally to firms.

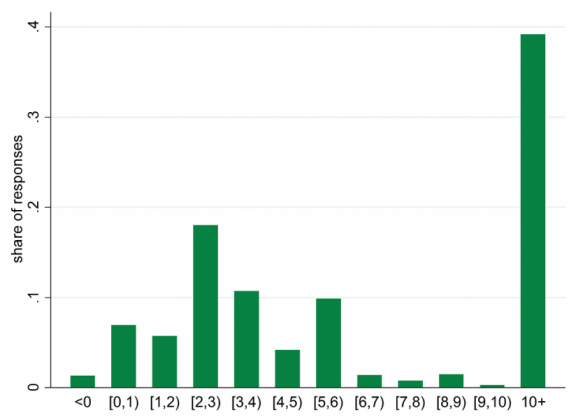

Figure 1: Perceived inflation target of Fed

A conventional policy narrative pertains that inflation expectations are well anchored so that changes in nominal policy rate transmit one-for-one to into perceived real interest rates via the Fisher equation. Yet, when we asked in Coibion et al (2022) 25,000 Americans in 2018 what they thought the average inflation rate was that the Federal Reserve tried to achieve over longer periods of time, only less than 20% of the survey participants answered a number around 2%, whereas almost 40% reported a number larger than 10% (see Figure 1). Not only do most ordinary households not have well-anchored expectations, they typically also overestimate future inflation relative to ex-post realizations. Using data from the New York Fed Survey of Consumer Expectations, in D’Acunto et al (2021a) we find that men on average expected an inflation rate of around 4% over the next twelve months during a sample period between 2011 and 2018 when realized inflation averaged below 2%, whereas women on average expected a rate of more than 6%. To dig deeper into the possible driving forces of this “gender gap” in inflation expectations, we fielded our own survey on the Nielsen homescan panel, which allowed us to survey male and female household heads at the same time. This within-household analysis made it feasible to keep constant many things that typically vary across survey participants like housing tenure, savings, and other determinants of inflation expectations. But even within households, we found that women on average expect higher inflation than men. Yet, when we split households based on the distribution of grocery duties across female and male household heads, we found that the gender gap was only present and in fact 50% larger in “traditional households” in which the male household head declared to never do any grocery shopping. In households in which the male household head instead stated to at least occasionally go grocery shopping, the gap disappeared because the male household heads also had higher inflation expectations. Hence, exposure to the volatile price changes during grocery shopping trips appear to manifest themselves in elevated inflation expectations of the grocery shoppers.

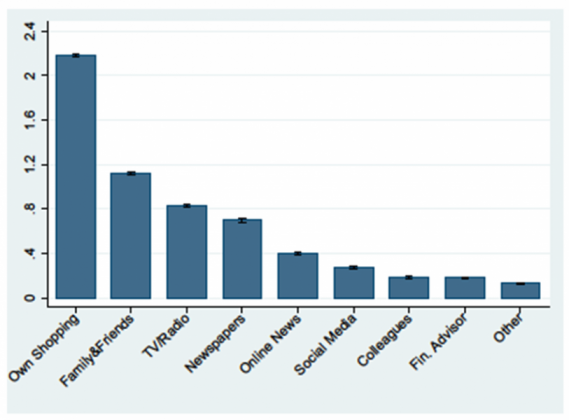

To better understand why this association appears in the data, we fielded another survey in D’Acunto et al (2021b), in which we directly asked survey participants which sources of information were most important to households when forming inflation expectations. Consistent with the seminal Lucas (1972) island model, we found that households rank “own grocery shopping experiences” as by far the most relevant source of information, before “Family and Friends,” “TV and Radio,” “Newspapers,” or other sources (see Figure 2). To directly establish a link between price changes observed while grocery shopping and inflation expectations, we levered the Nielsen homescan panel that allowed us to observe at the weekly frequency for 50,000 households the goods these households bought, where they bought them, which prices they paid, whether they purchased these goods on discounts, or used coupons. We then followed statistical agencies to create a chained Laspeyres price index but using household-specific consumption bundles and prices instead of the bundle of a representative household. Households with the highest realized inflation at the household level on average expected an inflation rate that was higher by 0.7 percentage than households with the lowest realized inflation rate over the previous twelve months. We can directly rule out that households might be forecasting their own inflation rate because we can observe their future realized household-level inflation rate.

In the Nielsen panel, we only observe around 25% of the overall consumption bundle for the average household. The fact that we can find a strong association between realized inflation at the household level for this subset of the bundle and overall inflation expectations suggests that grocery prices have a strong impact for how individuals think about inflation. At the same time, this finding also suggests that not all price changes are created equally for households. When we weight price changes by frequency of purchase rather than expenditure share, we find that this “Frequency CPI” drives the association between realized inflation and inflation expectations. In addition to putting larger weight on the price changes of frequently purchased goods, households also overweight positive relative to equal-sized negative price changes. These results can also explain why households immediately updated their inflation expectations in the summer of 2021 when most central banks still sang the gospel of temporary inflationary pressures in narrow categories. If these initial price spikes occur in categories that are salient to consumers, like rental cars, we can witness immediate increases in overall inflation expectations and workers in the US indeed immediately bargained for higher wages. These findings, however, also imply that even if central banks were successful in curbing realized inflation in the near term, household inflation expectations would still take time to come down again because ordinary consumers pay less attention to price cuts compared to price hikes.

Figure 2: Information sources for inflation

To better understand which role limited cognitive abilities might play for the focus on a handful of price changes to form expectations for overall inflation, in D’Acunto et al (2019, 2022c, forthcoming), we use data from Finland. Specifically, we were able to merge at the individual level measures of IQ for all men in Finland from the Finnish Defense Forces, income, wealth, and debt from annual registry data, as well as inflation and other expectations from the European Commission Consumer Survey for Finland. Empirically, we find that men in Finland at the bottom of the IQ distribution have mean absolute forecast errors for inflation of about 4.5%. Forecast errors monotonically decrease in measured IQ and are smaller by a factor of 2.5 for men in the top of the IQ distribution. It is also only men above the median IQ that increase their consumption spending when expecting higher inflation consistent with the consumer Euler equation. In D’Acunto et al (2022c), we show that men at the top of the IQ distribution are also more than twice as likely to take advantage of government subsidies like car scrappage schemes or to adjust their debt holdings to changes in interest rates. These results hold when we condition on education, income, and other observables and suggest that cognitive abilities are a central driving forces for inflation expectations and their association with real economic choices.

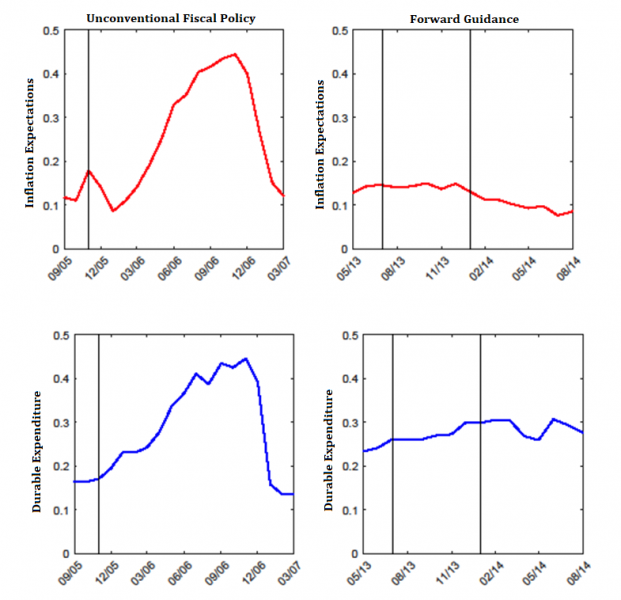

The important role of cognitive abilities suggests that policy complexity might play an important role for the effectiveness of economic policies, especially those that operate through household expectations. In D’Acunto et al (2022a), we compare the effectiveness of unconventional fiscal policies, preannounced increases of future consumption taxes that generate a predictable increase in future prices with forward guidance. Both policies, through the lens of the New Keynesian model, operate through inflation expectations and the consumer Euler equation. Yet, the policies differ quite substantially in their complexity and required understanding of economics to be effective. And indeed, when we compare their effectiveness using the micro data from the German version of the European Commission Consumer Survey, we find Germans only updated upwards their inflation expectations and spending plans after the announcement of former Chancellor Angela Merkel in November of 2005 to increase consumption taxes by three percentage points in January 2007 (left panels in Figure 3). Instead, Germans on average did not update neither their inflation expectations nor their consumption plans when former ECB President Mario Draghi for the first time explicitly used forward guidance as a policy tool in the summer of 2013 and firmly reiterated to keep interest rates at current or lower levels for an extended period of time in January 2014 (right panels in Figure 3).

Figure 3: Inflation expectations and spending

Given these findings, we studied in a series of papers how central banks should communicate to reach ordinary households who ultimately make consumption, savings, and debt decisions. In D’Acunto et al (2022d), we perform an information provision experiment in a customized survey with several thousand participants in Finland. In this survey, we first elicited individuals’ prior income change expectations and several sociodemographics. We then split the sample in three groups, a control group that did not receive any additional information and two treatment groups. We provided these groups with truthful information of policy actions by the ECB in the Spring of 2020 keeping constant the sender, Olli Rehn, Governor of the Finnish central bank, and the medium, his official Twitter account, but varied the content. One group received a “target” communication, that is, a message that specifies the aim of a policy without detailing which measures the central bank would implement to achieve it. Another group received information about the “instrument,” the specific policy that was implemented to achieve the goal. The target group received the announcement that the ECB will do whatever is necessary so that no Finn will suffer any economic harm from the pandemic. The instrument group, instead, read a sentence about the announcement of the Pandemic Emergency Purchase Programme. Finally, all survey participants answered the same questions again including the posterior elicitation of income change expectations. Empirically, we find that only the target communication is effective in improving individuals’ income expectations. The effect is concentrated within individuals with lower measures of cognitive abilities and who were unaware of the respective policies.

In Coibion et al (2022), we instead focus on the medium and the message of monetary policy communication. In another information provision experiment, we find that simple messages like current inflation, the inflation target, or the inflation forecast are most effective in managing individuals’ inflation expectations. Reading the official statement of the FOMC resulted in forecast revisions for inflation of similar magnitudes, even though it contained substantially more information and context. The coverage of the same FOMC meeting in newspapers, which are written for a lay audience and in substantially simpler language compared to the FOMC statement, instead, resulted in forecast revisions of only half the size. In the survey, we also elicited survey participants rating of the credibility of different news sources and found that households in the US on average rate newspapers the lowest in terms of credibility when it comes to information about the macroeconomy, whereas social media and Twitter in particular ranked highest. While possibly stronger in the US, this finding cautions against purely relying on the media as a means of transmission of monetary policy announcements to households. In the paper, we also show that individuals with exogenously higher inflation expectations increase their subsequent spending, both in survey data but also in actual spending data, which we observe via the Nielsen homescan panel.

Moreover, in D’Acunto et al (2022e), we document that also the identity of the sender of the message matters for the effectiveness of monetary policy communication. Specifically, we find in an information provision experiment in which we keep constant the message, forecasts for inflation and unemployment from the Summary of Economic Projections, that women and Black survey respondents are substantially more likely to incorporate these forecasts into their own subjective expectations when we make salient the presence of Mary Daly or Raphael Bostic, a female and Black male regional Fed President compared to making salient the presence of Thomas Barkin, a white male regional Fed President. We show in the paper that making salient the female or Black male presence on the FOMC increases the level of trust women and Black survey participants have in the Fed. In terms of mechanism, our results hint towards a taste for diversity channel, that is, preferring the representation of underrepresented groups on the FOMC relative to the majority of white men.

Finally, in Weber et al (2022a), we show that when individuals update their short run inflation expectations, they also update their long run inflation expectations in a similar fashion. This finding casts doubt on the idea that individuals temporarily change their short run expectations due to shocks but these changes do not transmit to long run expectations. Moreover, in Weber et al (2022b) we show that the stylized facts I discuss in this brief hold equally for firms. Other recent reviews of this literature are D’Acunto et al (2022g), Weber et al. (2022b), and Weber (forthcoming).

Taken together, these results show that individuals in general do not have well-anchored inflation expectations, that they focus on the price changes of salient, individual goods when forming inflation expectations, that households pay more attention to price increases relative to cuts but also that central banks can manage the expectations of households if they use simple messages. Yet, also the medium via which the message is transmitted and the identity of the messenger matters for the effectiveness. The biggest challenge for central banks remains reaching ordinary households who typically do not follow official releases and barely read the section on monetary policy in newspapers. More creative means of communications are called for.

Coibion, Olivier, Yuriy Gorodnichenko, and Michael Weber, 2022. “Monetary Policy Communications and their Effects on Household Inflation Expectations,” Journal of Political Economy 130(6): 1537–1584.

D’Acunto, Francesco, Daniel Hoang, and Michael Weber, 2022a “Managing Households’ Expectations with Unconventional Policies,” Review of Financial Studies 35(4): 1597–1642.

D’Acunto, Francesco, Daniel Hoang, Maritta Paloviita, and Michael Weber, 2021. “IQ, Expectations, and Choice,” Review of Economic Studies (forthcoming).

D’Acunto, Francesco, Daniel Hoang, Maritta Paloviita, and Michael Weber, 2019. “Cognitive Abilities and Inflation Expectations,” AEA Papers and Proceedings 109(5): 562-566.

D’Acunto, Francesco, Daniel Hoang, Maritta Paloviita, and Michael Weber, 2022c. “Human Frictions in the Transmission of Economic Policy,” Working Paper.

D’Acunto, Francesco, Daniel Hoang, Maritta Paloviita, and Michael Weber, 2022d. “Effective Policy Communication: Targets versus Instruments,” Working Paper.

D’Acunto, Francesco, Andreas Fuster, and Michael Weber, 2022e. “Diverse Policy Committees Can Reach Underrepresented Groups,” Working Paper.

D’Acunto, Francesco, Ulrike Malmendier, and Michael Weber, 2021a. “Gender roles produce divergent economic expectations,” Proceedings of the National Academy of Sciences 118(21): 1-10.

D’Acunto, Francesco, Ulrike Malmendier, Juan Ospina, and Michael Weber, 2021b. “Exposure to Grocery Prices and Inflation Expectations,” Journal of Political Economy 129(5): 1615-1639.

D’Acunto, Francesco, Ulrike Malmendier, and Michael Weber, 2022f. “What Do the Data Tell Us About Inflation Expectations?” Handbook of Economic Expectations (forthcoming).

D’Acunto, Francesco, Michael Weber, Olivier Coibion, and Yuriy Gorodnichenko, 2022b. “Wage-Price Spirals? Evidence from Households,” Working Paper.

Hackethal, Andreas, Philip Schnorpfeil, and Michael Weber, 2022a. “Inflation Expectations and Investment Choices,” Working Paper.

Hackethal, Andreas, Philip Schnorpfeil, and Michael Weber, 2022b. “Inflation Expectations, Net Nominal Positions, and Consumption,” Working Paper.

Lucas, Robert E. Jr. 1972. “Expectations and the Neutrality of Money.” Journal of Economic Theory 4(2): 103–124.

Weber, Michael, Francesco D’Acunto, Yuriy Gorodnichenko, and Coibion, Olivier, 2022. “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications,” Journal of Economic Perspectives (forthcoming).

Weber, Michael, Yuriy Gorodnichenko, and Coibion, Olivier, 2022b. “The Expected, Perceived, and Experienced Inflation of U.S. Households before and during the COVID19 Pandemic,” IMF Economic Review (forthcoming).

Weber, Michael, 2022. “Subjective Expectations and Reality,” Annual Review of Economics (forthcoming).