The views, opinions, findings, and conclusions or recommendations expressed in this paper are strictly those of the author. They do not necessarily reflect the views of the Swiss National Bank (SNB). The SNB takes no responsibility for any errors or omissions in, or for the correctness of, the information contained in this paper.

The global financial crisis of 2007–2008 might constitute another structural change in IMF lending after the Latin American debt crisis and the end of the Cold War. I find that with the crisis, the importance of financial corporations in IMF lending decisions has risen as major IMF shareholders seek to protect the exposure of their banks, which increased strongly in the years before the crisis. To impress global financial markets, they influence programme design towards more money and more conditions, specifically prior actions. This serves to keep the programme country’s market access and avoid default. While financial corporate interests are associated with a larger programme size for all countries, the positive link with more prior actions is only present for countries for which market access matters. For countries with limited market access, IMF staff’s technocratic interests in parsimonious conditionality dominate.

The history of IMF lending decisions since the founding of the institution in 1945 has by no means been homogenous. As Moser and Sturm (2011) describe, there have been at least two structural changes in the IMF lending process since the end of the Cold War. These are the end of the Latin American debt crisis in the late 1980s and the inclusion of the countries of the former Soviet bloc in the early 1990s, which led to almost global IMF membership (p. 2).

The IMF dramatically increased its lending volume because of the global financial crisis (GFC) of 2007–2008. It also extended its support to advanced economies, unseen for many years. Helped by a massive strengthening of its lending power (IMF, 2013a), the IMF played a crucial role in the stabilization of the international financial and monetary system. However, with this renewed visibility of IMF lending, criticism resurfaced that not only were economic considerations driving lending decisions but also the interests of the IMF’s most powerful member states. An example is the highly debated 2010 programme for Greece, which was widely considered to be influenced by an interest in protecting heavily exposed European and US financial corporations (Catan & Talley, 2013; Independent Evaluation Office of the International Monetary Fund [IEO], 2016).

In my paper (Andresen, 2022), I analyse how the influence of the financial corporate interests of major IMF shareholders on IMF lending has changed with the GFC. This research builds on large body of literature on factors influencing IMF lending design, according to which key determinants of IMF lending are international reserves, economic growth, currency crises, past IMF involvement, elections, and US geopolitical interests in the programme country (see, for example, Moser and Sturm 2011 and Dreher et al. 2015). Looking more specifically at the effect of financial corporate interests on IMF lending, this appears related to larger IMF programmes and softer conditionality (Oatley and Yackee 2004, Broz and Hawes 2006, Breen 2014). These findings relate to the time before the GFC. Presbitero and Zazzaro (2012) look at programmes from 2008 to 2010 and similarly find a relation with larger IMF programmes.

Based on the IMF’s design as laid out in the IMF Article of Agreements, two main actors shape IMF policy, specifically IMF lending decisions. These are the IMF shareholders − the states or governments − and IMF staff, the employees working at the Fund.2

For IMF staff, there are two principal types of interests to influence IMF lending design. IMF staff acts out of bureaucratic interests when it serve its institution’s interest in financial survival. As for the IMF, this is guaranteed by the interest earned on programmes, IMF staff has an incentive to aim for larger programmes than necessary from an economic perspective. IMF staff can also serve technocratic interests, such as when it bases its decision-making on beliefs about economic principles and concerns about global financial stability (Copelovitch, 2010, p. 50).

States also have the power and the interests to shape IMF lending design. The influencing power of states, as IMF members, on decisions of the IMF via the executive board is enshrined in the IMF’s articles of agreement. Most obviously, states requesting IMF lending may be driven by domestic interests in their negotiations with IMF staff. They can, for example, try to limit the reform needs in a programme, with the goal of limiting public protests in the country against unpopular reforms. States can also try to influence IMF decisions out of geopolitical interests. There is plenty of research on the role of geopolitical interests, most notably of the US, in IMF lending decisions.3

It could be assumed that financial corporate interests influence IMF lending decisions similarly to geopolitics. However, the mechanism is less straightforward. While geopolitical interests are inherent to the state itself, this is not the case for the interests of financial corporations. Financial corporations are not state actors, and they do not have a formal say on IMF decisions. For their interests to matter, it must be assumed that channels exist through which the interests of corporations can influence states, such that the states will take the corporations’ interests into account when negotiating IMF programmes and will effectively negotiate on their behalf.

In this context, a first question is what the goal of financial corporations’ influence on IMF lending could be. The literature describes two. The first goal is based on Gould’s (2003) research on how the fact that financial corporations act as supplementary financiers to IMF programmes influences conditionality. She finds that if supplementary financing by the private sector is a key factor for an IMF programme, the programme’s conditionality tends to contain more aspects that are beneficial for the banking sector. A second goal is protecting the interests of financial corporations that are exposed in the country requesting an IMF programme. This second goal is the focus of this study, as it is closer to the anecdotal evidence observed in the IMF programmes for Euro Area countries after the GFC.

A second question is through which channels financial corporate interests could influence IMF lending decisions. This relates to the more general question of how financial corporations influence policy-making by states. According to Young (2018), they do so through their normal business activities, through organized advocacy (lobbying), and through their enmeshment in elite networks (p. 386). In that sense, their influence can be both passive and active. If countries act out of fear of a negative financial market reaction, the power of financial corporations appears passive. However, if financial corporations actively influence state behaviour through lobbying or enmeshment in elite networks, their power becomes strategic.

In the context of financial corporate interests influencing IMF lending decisions, both active and passive channels are possible. If the banks of a particular country A are heavily exposed to another country B that is struggling economically, it is possible that the banks of country A will lobby their government to influence an IMF programme in a way that is beneficial to them. It is, however, also possible that the government of country A is afraid of the negative effect on its economy if one of its banks crashes, and hence, will act the same without explicit lobbying (Breen, 2014, p. 5).

During the era of the great moderation − after the end of the Cold War and before the GFC − the low-risk environment and the increasing search for yields contributed to increasing financial interconnectedness and a higher exposure of banks in countries outside their domestic markets. When the GFC hit and eventually evolved into the European debt crisis, protecting banks that had become heavily exposed to struggling countries such as Greece and Ireland became a major driving force of policy-making by IMF member states.

The importance of preserving financial stability became more acute for both governments and the IMF. At the same time, exposed banks likely increased their lobbying, leading to stronger state-corporation relations. Hence, it could be assumed that the influence of financial corporate interests on IMF policy-making increased with the GFC, both through the direct channel of lobbying and closer state-corporation relations and through the indirect channel of state interests in preserving financial stability.

The importance of protecting exposed banks is striking in the case of the first IMF programme for Greece, and there is a large amount of literature criticizing the role played by protecting financial corporate interests in the programme.4 In spring 2010, Greece became the first country in the Euro Area to receive an IMF programme of 30 billion euro. In his account of the negotiations around the IMF programme, Blustein (2015) describes how the programme was widely perceived as a means to pay European banks that were heavily exposed in Greece. Struggling German and French banks were among the largest holders of Greek bonds, and because of the IMF programme, they received payment in full and on time of their outstanding investments (p. 1). Blustein also describes how the fear that debt restructuring in Greece, which would have become necessary without the proposed IMF deal, would have become a Lehman-like event in which investors pulled their money out from all over Europe (p. 11).

The case is similarly compelling for Ireland, which received a 22.5 billion euro IMF programme in 2010. In his analysis of the programme, Breen (2012) finds strong support for economic and financial interests influencing the IMF programme for Ireland. He describes how during the negotiations on the programme design between the Irish authorities and IMF staff, there was initial agreement that some form of haircut should be imposed on senior bondholders of Irish banks. However, the European Central Bank and other IMF shareholders intervened to ensure that all senior bondholders had their losses covered. Breen assumes that France and Germany acted in this way to avoid the exposure of the weaknesses in their banks, which were heavily exposed to Ireland and other struggling European economies (p. 9).

To better understand how the influence of financial corporations on IMF lending has changed with the GFC, I analyse a yearly panel dataset from 1993 to 2016 for 120 countries. I focus on variables reflecting IMF programme design (loan size and two types of inbuilt-conditions: prior actions and quantitative performance criteria, QPC), as well as measures of claims of financial corporations of the major IMF shareholders − the US, the UK, Germany, Japan, and France. QPC are specific, measurable conditions (such as ceilings on new debt) that are under the control of authorities. Prior actions are policy steps a country needs to meet before the IMF executive board approves a programme or completes a review. These conditions are even tougher than QPC, as they cannot be waived. While all IMF programmes with conditionality will have QPC, prior actions are optional (IMF, 2021).

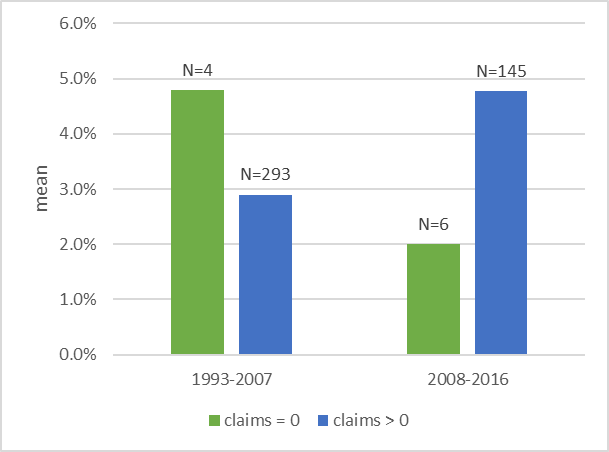

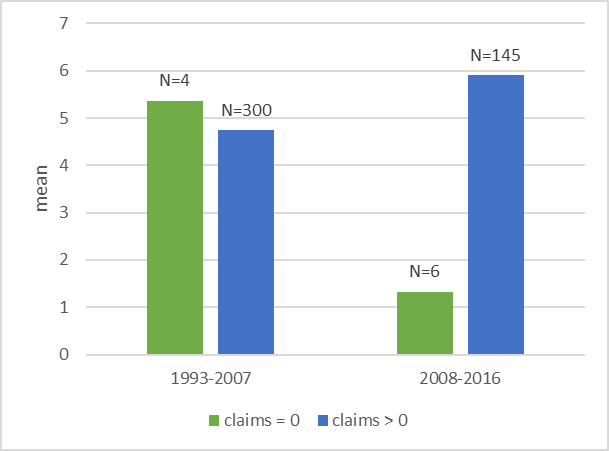

Figures 1 and 2 give some descriptive evidence about the relations between financial claims and IMF programme design variables. Figure 1 shows that IMF programs were smaller in the presence of claims of foreign banks before the GFC and considerably larger after the crisis. Figure 2 relates financial claims to programme conditionality, specifically prior actions, and finds a similar pattern. While the presence of claims mattered little to the number of prior actions before the GFC, there were considerably more prior actions in IMF programmes in the presence of claims after the crisis. For QPC, there is less of a pattern (not depicted).

Figure 1: Average IMF programme size, depending on the presence of claims of foreign banks, before and after the global financial crisis

Figure 2: Average number of prior actions in an IMF programme, depending on the presence of claims of foreign banks, before and after the global financial crisis

Notes: Figures 1 and 2 show the mean number of IMF loan size and prior actions, respectively, for the period before the global financial crisis (1993–2007) and after (2008–2016). The green bar shows the mean if there were no claims of foreign banks, whereas the blue bar shows the mean in the presence of such claims. Above the bars, the number of observations are shown.

In my paper (Andresen, 2022), I conduct a more detailed analysis of the influence of financial corporations on IMF lending and the change with the GFC, with the following findings:

The main finding is that the GFC constitutes another structural change in IMF lending, as the importance of financial corporations in IMF lending decisions has risen. Major IMF shareholders protect the exposure of their banks, which had risen significantly in the years before the GFC. To impress markets, they influence programme design in the country in which their banks are exposed towards larger lending amounts and tougher conditionality − specifically, more prior actions. This serves to keep the programme country’s market access and avoid default. While financial corporate interests are associated with a larger programme size for all countries, the positive link with more prior actions is only present for countries for which market access matters. For countries with limited market access, IMF staff’s technocratic interests in parsimonious conditionality dominate.

For future research, it would be interesting to go beyond the interests of the major IMF shareholders and account for the changing global order by capturing the interests of emerging global powers such as China. It would be interesting to see if and how Chinese financial corporate interests affect IMF lending. Furthermore, given that China has become a key global creditor, the role of Chinese sovereign and corporate debt in addition to financial interests could be of interest in IMF programme design for exposed countries.

Andresen, L. L. (2022). The influence of financial corporations on IMF lending: Has it changed with the global financial crisis? SNB Working Papers, 4(2022).

Blustein, P. (2015). Laid low: The IMF, the euro zone and the first rescue of Greece.

Breen, M. (2012). The International Politics of Ireland’s EU/IMF Bailout. Irish Studies in International Affairs, 75-87.

Breen, M. (2014). IMF conditionality and the economic exposure of its shareholders, European Journal of International Relations, 1-21.

Broz, J. L., & Hawes, M. B. (2006). Congressional politics of financing the International Monetary Fund. International Organization, 60(2), 367-399.

Catan, T. & Talley, I. (2013). Past rifts over Greece cloud talks on rescue. The Wall Street Journal. Retrieved from http://online.wsj.com.

Copelovitch, M. S. (2010). Master or servant? Common agency and the political economy of IMF lending. International Studies Quarterly, 54(1), 49-77.

Dreher, A., Sturm, J. E., & Vreeland, J. R. (2015). Politics and IMF conditionality. Journal of Conflict Resolution, 59(1), 120-148.

Gould, E. R. (2003). Money talks: Supplementary financiers and international monetary fund conditionality. International Organization, 57(3), 551-586.

International Monetary Fund [IMF] (2013). Factsheet: IMF’s response to the global economic crisis. Retrieved from http://www.imf.org.

International Monetary Fund [IMF] (2021). Factsheet: IMF Conditionality. Retrieved from http://www.imf.org.

Independent Evaluation Office of the International Monetary Fund [IEO] (2016). The IMF and the Crises in Greece, Ireland, and Portugal. Retrieved from http://www.ieo-imf.org.

Moser, C., & Sturm, J. E. (2011). Explaining IMF lending decisions after the Cold War. The Review of International Organizations, 6(3-4), 307-340.

Oatley, T., & Yackee, J. (2004). American interests and IMF lending. International Politics, 41(3), 415-429.

Presbitero, A. F., & Zazzaro, A. (2012). IMF lending in times of crisis: Political influences and crisis prevention. World Development, 40(10), 1944-1969.

Young, K. (2018). The modern financial corporation and global policy. In Handbook of the International Political Economy of the Corporation. Edward Elgar Publishing.

See Copelovitch (2010) for a detailed overview of the various types of actors and their interests in IMF policy design.

For a good overview, see Moser and Sturm (2011).

See IEO (2016), p. 4, for a good overview.