We measure the gains from phasing out coal as the social cost of carbon times the quantity of avoided emissions. By comparing the present value of avoided carbon emissions to the present value of the costs of ending coal plus the costs of replacing it with renewable energy, our baseline estimate is that the world could realize a net total gain of 77.89 trillion US dollars. This represents around 1.2% of current world GDP every year until 2100. The net benefits from ending coal are so large that renewed efforts, carbon pricing, and other financing policies, should be pursued.

International negotiators can’t agree on how to phase out coal, in part because of opposition to carbon taxes, and now even countries that had been able to abandon the fuel are reversing that progress as the war in Ukraine raises energy prices.

The most common concern about scrapping coal is that replacing it with renewable energy would be too expensive, but we show in new research that the economic benefits would far outweigh the costs.

We analyze this great carbon arbitrage, as we call it, in a recent working paper that calculates the cost of replacing coal with renewables, as well as the social benefits of this important transition. The benefits from ending coal use come from avoiding damage from climate change and harm to people’s health. Our estimate is that by doing so the world would yield a net gain of nearly $78 trillion through the end of this century. That’s around four-fifths of global gross domestic product now, and would be equivalent to about 1.2 percent of annual global economic output during the period. Per tonne of coal, the net gain is estimated to be $125, and per tonne of avoided coal emissions, the net gain is $55.

To determine both the size of the avoided emissions, as well as any potential losses from their prevention, we use a detailed dataset compiled by Asset Resolution on companies’ historical and projected global coal production based on the aggregation of production at the plant level.

The cost estimate for adopting renewable sources includes capital spending for new energy generation capacity equal to what’s lost with coal, plus compensation to coal companies for lost earnings when they are shut down. The cost estimate does not include compensation for affected workers, but this is likely to be small relative to the overall net gains from the transition. Additional compensation to make the switch to renewables feasible could be offered as long as the social benefits of phasing out coal exceed the more comprehensive set of costs.

We calculate the value of doing so by estimating the reduction in emissions from phasing out coal, and by applying a carbon price to those discharges. This in turn lets us estimate the economic gain from the transition. The difference between the value of the social benefits versus costs of replacement and compensation for missed coal revenues forms our baseline estimate of world’s net gain from finally ending our reliance on the fuel.

While our conservative estimate comes with an unavoidable uncertainty, given the decades-long timeframe, the enormous social benefits from what could be thought of as an inexpensive insurance policy are clear: paying a premium offers coverage for significant potential damages.

So sizeable are the potential gains that world leaders should pursue a global agreement to finance the phase-out of coal as a complement to carbon pricing or equivalent measures that currently don’t fully offset the negative effects of the emissions. We have chosen all our parameters, including the social cost of carbon, in a conservative way. The carbon arbitrage could in fact be bigger still for less conservative estimates.

Our research shows that ending coal use shouldn’t be seen as too costly because it provides economic benefits from reduced carbon emissions, such as avoiding physical damage to infrastructure caused by climate change. Investments in renewable energy also support economic growth and offer additional attendant benefits from innovation.

The analysis shows that phasing out coal isn’t just urgent because it would help limit the global temperature increase to 1.5 degrees Celsius. Importantly, the economic and health benefits are significant enough that we should push harder for global agreements that unleash the potential power of capital markets.

The bottom line for policy is that if compensation was built into an agreement to scrap coal, and if innovative financing packages could incentivize advanced, emerging and developing economies alike to end the fuel’s use, the net social gains from such an agreement would be enormous.

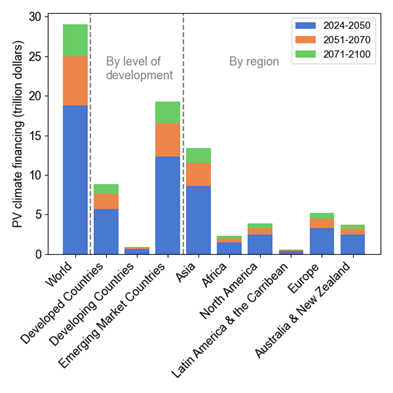

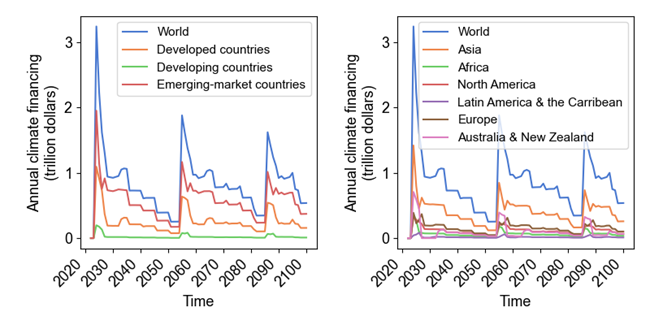

To better understand just how large the payments would need to be, we broke down the costs for different regions (see Figure 1). The present value of total financing that’s conditional on commitments to scrap coal is around $29 trillion globally, in line with what other studies estimate. That works out to between $500 billion and $2 trillion annually, with a front-loaded $3 trillion investment this decade (see Figure 2). Of the global financing need of around $29 trillion, we estimate that 46 percent is in Asia, 18 percent in Europe, 13 percent in North America, 13 percent in Australia and New Zealand, 8 percent in Africa, and 2 percent in Latin America and the Caribbean.

Figure 1: Present value of climate financing needs to replace phased-out coal with renewables.

Notes: The cost estimate captures the opportunity cost of coal and investment costs in renewables.

Figure 2: Annual climate financing needs to replace phased-out coal with renewables (non-discounted).

Notes: The cost captures the opportunity cost of coal and investment costs in renewables.

It’s a major funding challenge. But despite arguments that no government can afford such investments and that the private sector should steer its funding to renewable energy, most of the backing can indeed come from the private sector, once risks are reduced by sufficient public funds via so called blended finance, which could mean public funding of around 10 percent.

Broadly speaking, it’s in the interest of a government to finance 10 percent of its country’s total costs to replace coal with renewables if this amount is less than its resulting social benefits in terms of lower climate damages. A back-of-the-envelope calculation suggests this holds true for nearly all countries. Considerations of fairness, a country’s fiscal position, or both, may in certain cases call for foreign contributions to finance 10 percent of a country’s costs to phase out coal.

We view global carbon taxation at the social cost of carbon as a first-best solution. Public-private partnerships to finance the replacement of coal with renewables could accelerate the green transition and complement incomplete carbon pricing by helping to achieve the Paris Agreement’s aim of making finance flows consistent with a pathway toward low greenhouse gas emissions and climate-resilient development.

For their part, economists have two different approaches to what the profession calls internalizing negative externalities. That loosely translates as making companies pay more of the costs imposed by some harmful result of their activity, such as pollution. One, associated with Arthur C. Pigou, uses taxation or some other pricing to fully reflect the social cost of an economic activity. The other, linked to Ronald H. Coase, seeks an efficient social outcome through bargaining and contracting. Clearly, both approaches are needed for a global strategy to combat climate change.

Our research concludes that, under the kind of approach Coase pioneered, it’s sound economic logic to pay for the replacement of coal with renewables to reap a net social gain measuring in the tens of trillions of dollars.

Phasing out coal is not only a matter of urgency for the planet. It also makes economic sense because, as we show, the social gains far outweigh the costs of climate financing to end coal.

We created a dedicated website, greatcarbonarbitrage.com, on which you can explore our results!

Adrian, T., Bolton, P., and Kleinnijenhuis, A. (2022), “The Great Carbon Arbitrage”, IMF Working Paper No. 2022/107.

|

About the authors Tobias Adrian is the Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department. He leads the IMF’s work on financial sector surveillance and capacity building, monetary and macroprudential policies, financial regulation, debt management, and capital markets. Prior to joining the IMF, he was a Senior Vice President of the Federal Reserve Bank of New York, and the Associate Director of the Research and Statistics Group. Mr. Adrian has taught at Princeton University and New York University, and has published in economics and finance journals, including the American Economic Review and the Journal of Finance. His research focuses on the aggregate consequences of capital market developments. He holds a PhD from the Massachusetts Institute of Technology; an MSc from the London School of Economics; a Diplom from Goethe University Frankfurt; and a Maîtrise from Dauphine University Paris. Patrick Bolton was Professor of Business at Columbia Business School. His career began at University of California at Berkeley, then Harvard University, L’Ecole Polytechnique, LSE, l’Université Libre de Bruxelles, and Princeton University. He is a graduate of University of Cambridge, Institut d’Etudes Politiques de Paris and London School of Economics (PhD). His research and areas of interest are in contract theory and contracting issues in corporate finance and industrial organization. A central focus of his work is on the allocation of control and decision rights to contracting parties when long-term contracts are incomplete. This issue is relevant in many different contracting areas including: the firm’s choice of optimal debt structure, corporate governance and the firm’s optimal ownership structure, vertical integration, and constitution design. His work in industrial organization focuses on antitrust economics and the potential anticompetitive effects of various contracting practices. He recently published his first book, Contract Theory, with Mathias Dewatripont and has co-edited a second book with Howard Rosenthal, Credit Markets for the Poor. Alissa M. Kleinnijenhuis is a Research Scholar at the Stanford Institute of Economic Policy Research (SIEPR) at Stanford University. She is also a Senior Research Associate at the Institute for New Economic Thinking (INET) at the Oxford Martin School of the University of Oxford. Alissa is a Co-PI of a Market Ecology & Financial Stability Grant, supervising four PhD students, and Co-Founder of the Environmental Stress Testing and Scenarios Program (ESTS), both at the University of Oxford. She taught a novel course at Stanford University in Fall 2021 on Climate Finance. Kleinnijenhuis’ research examines how finance can advance the public good, focusing on how the financial sector can be leveraged as a first-order driver of a climate change solution. In particular, her research in area of climate finance examines how financial incentives can be aligned with limiting climate risks and financing the transition to a carbon-neutral economy. Her research is all about making the triangular sectors of finance – the public, private and academic sector – work for the green transition. Her second area of expertise concerns financial stability, financial crises, financial stress testing, and financial regulation. Her two focal areas of research – climate finance and financial stability – are linked by their emphasis on addressing externalities emerging from climate change and too-big-to-fail financial institutions. Dr. Kleinnijenhuis holds a BS from Utrecht University in Economics and Mathematics (cum laude), a MSc in Mathematics and Finance from the Imperial College London, and a DPhil (PhD) in Mathematical and Computational Finance from the University of Oxford. She was a Postdoctoral Fellow at the MIT Sloan School of Management and the MIT Golub Centre for Finance and Policy (GCFP) at the Massachusetts Institute of Technology. She has been a Visiting Scholar at Yale University and the University of California Santa Barbara, and has conducted research at Morgan Stanley and Allianz Global Investors. |