References

Amiti, M., M. Dai, R. Feenstra and J. Romalis (2018) How Did China’s WTO Entry Affect U.S. Prices? Federal Reserve Bank of New York Staff Reports No. 817. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr817.pdf?la=en

Auer, R., C. Borio and A. Filardo (2017) The globalization of inflation: the growing importance of global value chains, BIS Working Papers No 602. https://www.bis.org/publ/work602.pdf

Bernhofen, D. , Z. El-Sahli and R. Kneller (2013) Estimating the effects of the container revolution on world trade, Lund University, Economics Department Working Paper 2013:4. https://project.nek.lu.se/publications/workpap/papers/WP13_4.pdf

BIS (20221) BIS Annual Economic Report June 2022. https://www.bis.org/publ/arpdf/ar2022e.pdf

ECB (2021) The implications of globalization for the ECB monetary policy strategy. ECB Occasional Paper 263. https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op263~9b56a71297.en.pdf

European Parliament (2015) Is globalization reducing the ability of central banks to control inflation. https://www.europarl.europa.eu/cmsdata/105466/IPOL_IDA(2015)563476_EN.pdf

Goodhart, C. and M. Pradhan (2020) The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival. Palgrave. Macmillan, London.

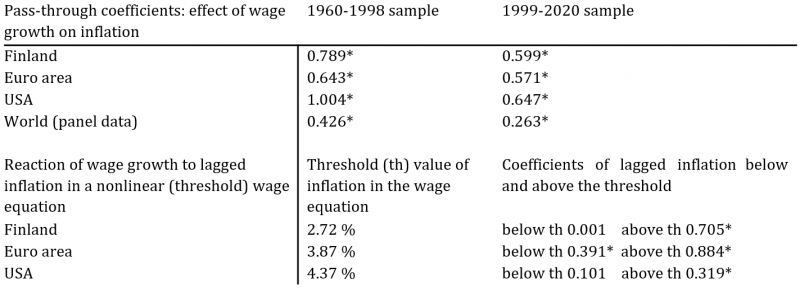

Kohlscheen, E, and Moessner, R. (2021) Globalisation and the Decoupling of Inflation from Domestic Labour Costs. CESifo Working Paper 9281. https://www.cesifo.org/en/publikationen/2021/working-paper/globalisation-and-decoupling-inflation-domestic-labour-costs

Pain, N., I. Koske and M. Sollie (2008) Globalisation and OECD Consumer Price, OECD Economic Studies 44. https://www.oecd.org/economy/42503918.pdf

Peneva, E. and J. Rudd (2015) The Passthrough of Labor Costs to Price Inflation, Finance and Economics Discussion Series 2015-042. Board of Governors of the Federal Reserve System, http://dx.doi.org/10.17016/FEDS.2015.042

Reis, Ricardo (2021) The People versus the Markets: A Parsimonious Model of Inflation Expectations,” CEPR Discussion Papers 15624.

Rudd, J. (2021) Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?): Federal Reserve Board. Finance and Economics Discussion Series 2021-62. https://www.federalreserve.gov/econres/feds/files/2021062pap.pdf

Stock, J. and Watson, M. (2021) Slack and Cyclically Sensitive Inflation. https://scholar.harvard.edu/files/stock/files/stock_watson_slack_and_critically_sensitive_inflation _070918.pdf