The views expressed in this Policy Brief are those of the authors and do not necessarily reflect those of the European Stability Mechanism (ESM).

Macroeconomic forecasts of economic policy institutions are usually accompanied by an assessment of risks to the projections. These risks are often not balanced around the baseline forecast.

“FOMC participants (Board members and Reserve Bank presidents) indicated that considerable uncertainty surrounded the outlook for economic growth and that they saw the risks around that outlook as skewed to the downside.”

Monetary Policy Report to Congress, Federal Reserve Board, Feb. 2008 (p.2)

“The outlook for the UK and global economies remains unusually uncertain. […] The risks are skewed to the downside.”

Monetary Policy Report, Bank of England, Aug. 2020 (p.1)

These two quotes from the onset of the Great Recession and the aftermath of the Covid-19 shock are two examples where policy-makers have used the notion of skewness to communicate their beliefs about the asymmetric distribution of risks. A precise assessment of economic risks provides the foundation for a clear communication by policy-makers that can support the individual risk assessment of households and businesses. Moreover, the adoption of appropriate economic policies to mitigate potential risks hinges on understanding them well in the first place. In a recent paper (Iseringhausen et al., 2022), we develop a novel measure of economy-wide expected skewness and study how changes in this measure, reflecting adjustments of existing risk assessments, link to the business cycle.

Recent work has found sizeable time variation in the asymmetry of risks. Adrian et al. (2019) highlight that downside risks to GDP growth are highly cyclical and partially predictable by measures of financial conditions (see also Giglio et al., 2016; Caldara et al., 2021).1 Adams et al. (2021) document similar features in the risk dynamics of unemployment and inflation (see also López-Salido and Loria, 2020). Dew-Becker (2021) highlights the presence of time-varying skewness in stock markets.

Motivated by these considerations, we propose a new measure to assess the balance of macroeconomic risks in the US economy. The purpose of this measure of aggregate expected skewness is to reflect the relative importance of downside and upside risks based on a large dataset of relevant macroeconomic and financial indicators (McCracken and Ng, 2016, 2020). The dataset includes, among others, indicators related to national income and product accounts, industrial production, labor markets, prices, interest rates, money and credit, and non-household balance sheets. As such, it covers most aspects of the US macroeconomy, all of which can provide signals of emerging risks. We develop an intuitive and simple two-step approach to measure aggregate asymmetry in the distribution of risks. First, for each of the more than 200 variables in the dataset, we compute a series-specific (quantile-based) measure of expected skewness for the next quarter, where the time variation in the quantiles of the distribution is retrieved based on the approach of Engle and Manganelli (2004). Second, we aggregate all these individual measures into a single expected skewness factor using principal component analysis.

Based on this measure, we document various regularities in the evolution of the balance of risks and contrast our measure with alternative measures of macro and micro skewness. We find that aggregate expected skewness:

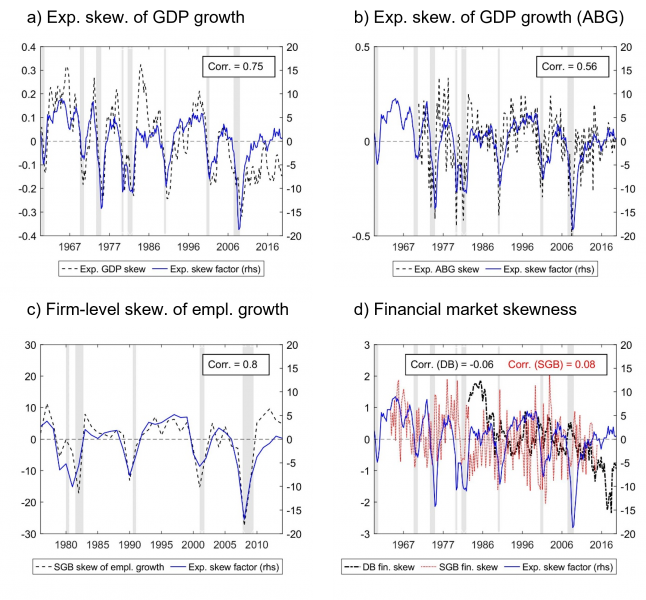

These results suggest that risks signalled by GDP growth alone may not always reflect the full set of risks in the economy. In addition, shifting risks to the downside during recessionary periods are a stylized fact that can be signalled by our aggregate skewness factor even though it does not explicitly include a composite index of financial conditions. Overall, these findings indicate that our economy-wide measure of skewness successfully captures different types of unbalanced risks emerging in the economy.

Figure 1: Expected skewness factor vs. other measures of skewness

Sources: Authors’ calculations based on FRED-QD, Chicago Fed, Salgado et al. (2019), and Dew-Becker (2021).

Notes: The figure contrasts the expected skewness factor of Iseringhausen et al. (2022) with alternative (expected) skewness measures, i.e., a) the skewness of GDP growth, b) the skewness of GDP growth based on Adrian et al. (2019), c) the cross-sectional firm-level skewness of employment growth and d) the option-implied skewness of the S&P500 (DB fin. skew.) as well as the cross-sectional skewness of firms’ stock returns (SGB fin. skew.). All alternative skewness series are de-meaned and the scale of the SGB fin. skew. measure is adjusted for comparability with the DB measure.

Changes in macroeconomic risk, uncertainty, and general sentiment can have a sizeable impact on business cycle fluctuations (see, e.g., Jurado et al., 2015). Using our measure of aggregate expected skewness, we show that changes in the relative importance of macroeconomic downside and upside risks, i.e., shifts in the balance of risks, also have important implications for business cycle dynamics.

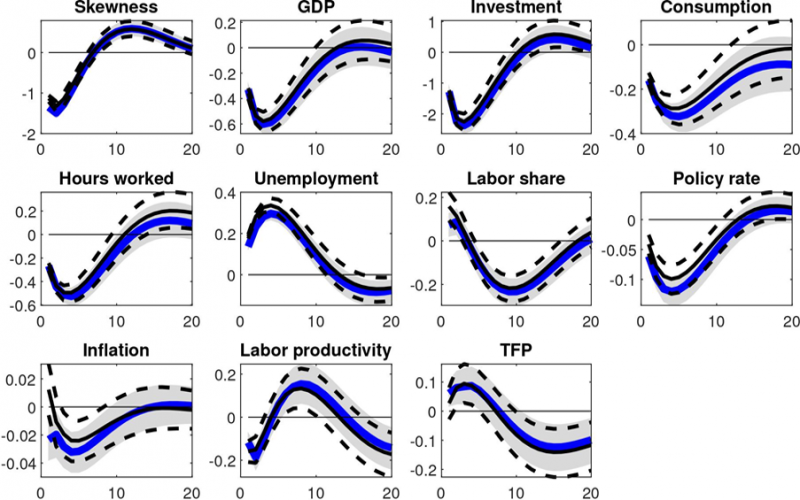

We use a vector autoregressive (VAR) model to study the dynamic relationship between changes in our factor-based measure of the balance of risks, and various macroeconomic variables (real GDP per capita, real investment per capita, real consumption per capita, hours worked per person, unemployment rate, labor share, effective federal funds rate, inflation, labor productivity and a measure of TFP). Within this setting we identify revisions in aggregate expected skewness that reflect a reassessment of the balance of risks due to the arrival of new information.

Figure 2: Responses to a skewness shock and the main business cycle shock

Notes: The figure shows the mean responses to a negative shock to expected skewness (blue) and to a contractionary main business cycle shock (black) (Angeletos et al., 2020) together with the 68% highest density intervals.

A downward revision in expected skewness, reflecting a shift towards a higher relative importance of downside compared to upside risks, can have contractionary effects on macroeconomic outcomes (Figure 2). Such a downward revision i) decreases output, investment, consumption, and hours worked; ii) increases unemployment; but iii) does not cause any meaningful changes in inflation and productivity. Interestingly, these responses to a negative change in perceived downside risk closely match the economy’s reaction to the main business cycle shock documented in Angeletos et al. (2020), with the latter being a powerful and robust stylized fact of the US economy. This highlights the key role that perceived risks, and especially their balance in terms of downside vs. upside risks, play in understanding business cycle fluctuations (see also Forni et al., 2021; Salgado et al., 2019).

Risks to the macroeconomic outlook are ubiquitous and more often skewed to the downside than not. The Covid-19 pandemic and the war in Ukraine are two examples where perceived risks have clearly shifted to the downside. Understanding the presence and evolution of such risks is paramount for economic policy institutions. Our work provides policy-makers with a timely measure of the macroeconomic risk balance considering information from numerous economic indicators. In addition, our analysis highlights the importance of accounting for a procyclical variation in the conditional skewness of macroeconomic data. Macroeconomic theories that search for shocks and propagation mechanisms behind macroeconomic fluctuations will need to be able to reproduce variations in aggregate skewness whose revisions are strongly affected by the main source of business cycle fluctuations.

Adams, P. A., Adrian, T., Boyarchenko, N. and Gianonne, D. (2021), “Forecasting Macroeconomic Risks”, International Journal of Forecasting, 37(3), 1173-91.

Adrian, T., Boyarchenko, N. and Gianonne, D. (2019), “Vulnerably Growth”, American Economic Review 109(4), 1263-89.

Angeletos, G.-M., Collard, F. and Dellas, H. (2020), “Business-Cycle Anatomy”, American Economic Review 110(10), 3030-70.

Caldara, D., Scotti, C. and Zhong, M. (2021), “Macroeconomic and Financial Risks: A Tale of Mean and Volatility”, International Finance Discussion Papers, No. 1326, Board of Governors of the Federal Reserve System (U.S.).

Delle Monache, D., De Polis and A., Petrella, I. (2021), “Modeling and Forecasting Macroeconomic Downside Risk”, Bank of Italy Temi di Discussione (Working Paper), No. 1324.

Dew-Becker, I. (2021), “Real-time forward-looking skewness over the business cycle”, Mimeo.

Engle, R. F. and Manganelli, S. (2004), “CAViaR: Conditional Autoregressive Value at Risk by Regression Quantiles”, Journal of Business & Economic Statistics 22(4), 367-381.

Forni, M., Gambetti, L. and Sala, L. (2021), “Downside and upside uncertainty shocks”, CEPR Discussion Papers, No. DP15881, Centre for Economic Policy Research.

Giglio, S., Kelly, B. and Pruitt, S. (2016), “Systemic risk and the macroeconomy: An empirical evaluation”, Journal of Financial Economics, 119(3), 457-471.

Iseringhausen, M., Petrella, I. and Theodoridis, K. (2022), “Aggregate Skewness and the Business Cycle”, ESM Working Papers, No. 53, European Stability Mechanism.

Jurado, K., Ludvigson, S. C. and Ng, S. (2015), “Measuring Uncertainty”, American Economic Review 105(3), 1177-1216.

López-Salido, J. D. and Loria, F. (2020), “Inflation at Risk”, Finance and Economics Discussion Series, No. 2020-013, Board of Governors of the Federal Reserve System (U.S.).

McCracken, M. W. and Ng. S. (2016), “FRED-MD: A monthly database for macroeconomic research”, Journal of Business & Economic Statistics, 34(4), 574-89.

McCracken, M. W. and Ng. S. (2020), “FRED-QD: A quarterly database for macroeconomic research”, Federal Reserve Bank of St. Louis Working Paper, No. 2020-005.

Salgado, S., Guvenen, F. and Bloom, N. (2019), “Skewed Business Cycles”, NBER Working Papers, No. 26565, National Bureau of Economic Research.