This SUERF Policy Brief summarizes the paper titled ‘Reserve-backed tokens: a money for the future?’ which is forthcoming in the Journal of Payments Strategy and Systems, Vol 18, No 2. The views expressed in this brief are those of the author and do not necessarily reflect those of the BIS.

Exactly what form the money of the future will take remains an open question. CBDCs, tokenised deposits, and stablecoins are potential candidates. Tokens that are entirely and exclusively backed by central bank reserves – ie reserve-backed tokens (RBTs) – also offer a credible solution. RBTs pose a unique combination of benefits. They are safer than, and can crowd out, the unstable breeds of stablecoins. They can adopt a more flexible design than retail CBDCs and thus foster greater competition and innovation. Compared to bank deposits, RBTs are immune to runs and are unencumbered by legacy features. Naturally, there are attendant risks and unknowns, but careful design and gradual rollout can help harness the benefits of an RBT while mitigating the risks.

Technological advances such as distributed ledgers and tokenisation are forcing a fundamental rethink about money among policymakers and financial service providers. This shift also reflects users’ changing expectations. As such, the search for a money that is more suitable for increasingly digitalised economies is underway. While much of the money currently in use is already in digital form (eg bank deposits and e-money), recent focus is on tokenised money. Central banks are studying retail CBDCs, with some live rollouts already. Commercial banks are exploring tokenised deposits. And fintechs are issuing a wide variety of stablecoins. This brief examines a yet another form of tokenised money: tokens issued by regulated private entities that are solely and fully backed by central bank reserves, or reserve-backed tokens (RBTs).

RBTs are not an entirely new concept. Researchers have previously argued in favour of related arrangements.1 The Bank of England’s preferred model for systemic stablecoins is to have them fully backed by central bank reserves.2 In Hong Kong and the United Kingdom, select commercial banks are allowed to issue banknotes against a full backing of monetary authority securities or reserves. Going further back in time, RBTs find similarities with the narrow bank proposal in the Chicago Plan.

The goal of this brief is to present how an RBT could be designed to harness its potential as a tokenised money form, compare RBTs with alternatives such as retail CBDC, tokenised deposits, and stablecoins, and draw its implications for the financial system.

The overarching objective of an RBT is clear – to serve as a medium of exchange – but its optimal design is not. RBTs must add value relative to alternatives but not pose undue risks. This raises several design trade-offs.

A first issue is who should be given access to the central bank balance sheet and relatedly the license to issue RBTs. Banks may be a natural choice since they already have such access and are well regulated. However, not giving non-banks and fintechs access would raise fairness concerns. In the long term, therefore, a competitive licensing regime may be needed.

Second, the regulatory framework for RBTs could draw elements from the framework for banks but could be much simpler as banks are multipurpose entities that require more complex regulation. And while RBTs and stablecoins could share the same framework due to inherent similarities, oversight would have to be more stringent in the case of RBTs as they are ‘closer’ to the central bank.

Third, as a means of payment like cash, RBTs should not pay interest. Interest payments could jeopardize the very ethos of an RBT as then issuers would compete on interest rates and invest in riskier assets. A non-interest bearing RBT – combined with limits on wallet balances – would also help reduce the risk of disintermediating bank deposits and moderate the impact on the central bank balance sheet.

Fourth, to ensure that the RBT business model is a viable, interest on RBT reserves may be necessary. This would complement any transaction fee and auxiliary service fee charged by RBT issuers. And while paying interest on RBT reserves would entail a cost for the central bank, the RBT reserve rate could be distinct from the policy rate and instead be calibrated to match the profitability of peers in the payment business. Relatedly, keeping RBT reserves distinct from traditional ones would help limit an RBT’s monetary policy implications and also help from an accounting perspective. In terms of the operating model, a centralised ledger (like RTGS) may be used initially, while permissioned distributed ledger is likely to be more effective in the long term.

Finally, transfer models for RBTs – burn-issue (ie liabilities burnt and created during a transfer) versus bearer – entail trade-offs between singleness3 and functionality. Relatedly, interoperability with the crypto ecosystem would require balancing risk-management with wider appeal. As a result of these trade-offs, giving issuers some design flexibility – while ensuring a minimum degree of safety – could be the way forward. In the end, issuers may self-select into the type of RBT they would like to design depending on their target use case. This could support competition and innovation.

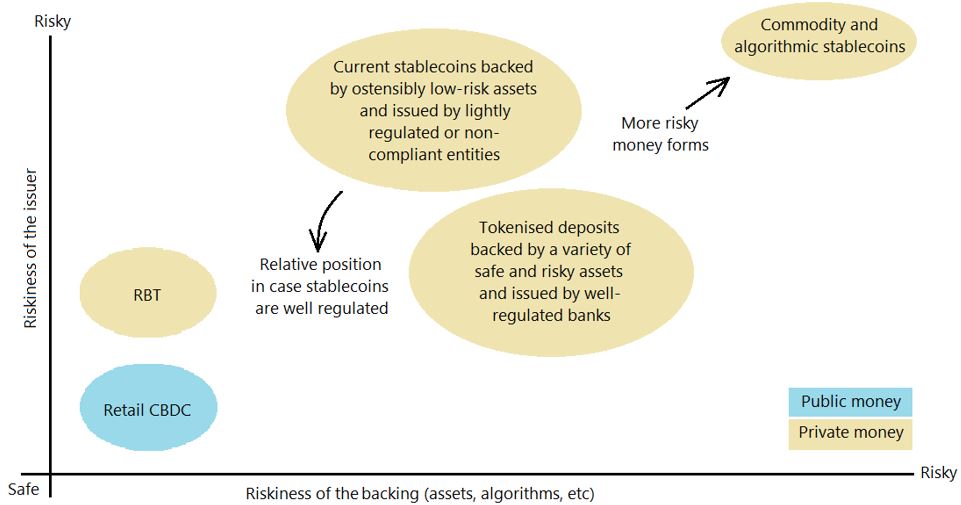

The various tokenised money forms can be seen as part of a continuum. As Figure 1 shows, the continuum can be described by two dimensions: the riskiness of the backing (x-axis), and the riskiness of the issuer (y-axis). By design, money forms that lie towards the upper right-hand corner of this continuum are riskier.

Figure 1: Tokenised money forms as part of a continuum

In terms of an RBT’s asset backing (ie position along x-axis), they are fully backed by central bank reserves, making them equally safe as CBDCs. Meanwhile, an RBT’s backing is safer than that of bank deposits (ie a variety of low and high risk assets), fiat-backed stablecoins (ie ostensibly low risk and highly liquid assets), and other stablecoins (ie those backed by commodities or algorithms).

In terms of an RBT’s issuer (ie position along y-axis), they are issued privately, making them riskier than central bank issued retail CBDCs. That said, an RBT issuer would be equally well regulated as a bank issuing deposits. And while the current breed of stablecoin issuers are riskier, they are likely to be at par with banks and RBT issuers once jurisdictions adopt regulatory frameworks for stablecoins based on the “same risk, same regulation” principle (eg MiCA in Europe).

All in all, while retail CBDC is the safest form of tokenised money, RBTs are safer than tokenised deposits and stablecoins – ie RBTs stand somewhere in the middle. Nonetheless, a comparison of the specific design features reveals that RBTs pose a unique combination of benefits relative to alternatives (Table 1).

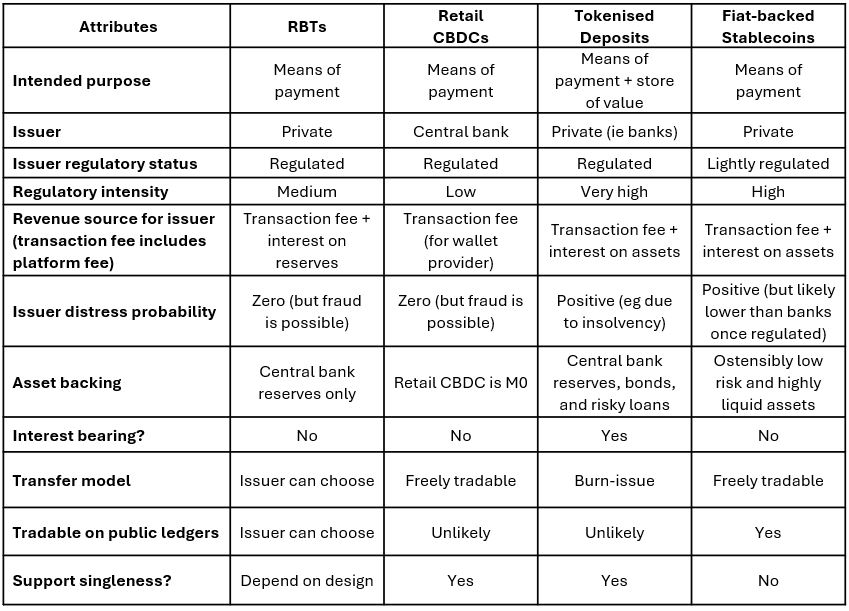

Table 1: A comparison of RBTs, retail CBDCs, tokenised deposits, and stablecoins

Retail CBDCs, being issued by central banks, contrast with RBTs which are privately issued but are backed by central bank reserves. This distinction makes RBTs operationally simpler for central banks as they would need to assume a bigger role as a CBDC issuer as compared to being an RBT enabler. Low RBT adoption would not be the central bank’s headache either, unlike in case of a retail CBDC. RBT issuers would also have greater skin in the game than retail CBDC wallet providers, especially because of interest on RBT reserves. This may attract greater financial interest from private players and encourage RBTs to be designed more flexibly, thus improving innovation. Additionally, RBTs help deepen public-private partnership, leveraging the strengths of both sectors – public sector providing the monetary backing and regulation and a competitive private sector building on top of it. All this is not to say that RBTs and retail CBDCs are substitutes. On the contrary, lessons from one engagement could inform the other.

Compared to fiat-backed stablecoins, RBTs constitute a safer arrangement. On the one hand, stablecoins have often broken their promise of convertibility at par and violated singleness. Stablecoin issuers have incentives to invest in riskier assets. And stablecoin sell-offs can trigger a fire-sale of the underlying assets and depress prices. Stablecoins also depend on custodians for the asset-backing. Moreover, so far, issuers tend to be lightly regulated and rely on complex contractual agreements (eg terms of redemption) that users may not fully appreciate. On the other hand, RBTs would be fully backed by central bank reserves – the ultimate unit of account – and only be issued by well-regulated entities. This would minimise scope for deviations from par and avoid dependency on custodians. A simpler balance sheet would improve transparency and help with compliance. As tokenised instruments, they would still capture the beneficial aspects of stablecoins (such as programmability and atomicity), but in a safer and more stable manner. In fact, crypto-friendly RBTs may become a trusted and preferred means of payment within the crypto ecosystem and displace unstable stablecoins. A safer crypto ecosystem would also imply fewer negative spillovers to traditional finance. Overall, RBTs can complement efforts to regulate crypto (stick-based approach) by ensuring that traditional finance remains attractive (carrot-based approach).

Compared to tokenised deposits too, RBTs pose benefits. Deposits serve multiple functions. They are used for both savings and payments, can have various maturities, and pay interest, and are subject to deposit insurance. This can make the tokenisation of deposits complicated, and thus uniform tokenisation across banks more challenging. More fundamentally, tokenised deposits can result in further use-cases for a bank’s liabilities and expose it to more demand shocks. This can make deposit funding more volatile and exacerbate bank runs. By contrast, RBTs have a clean slate advantage and a narrowly defined purpose, ie serve as a tokenised medium of exchange. Like tokenised deposits, RBTs would still be compatible with unified ledgers.4 Yet, RBTs would not have interest payment or deposit insurance considerations, making them a simpler money form. And while banks could issue RBTs using their existing balance sheet, they may prefer (or be required) to set up subsidiaries and issue RBTs using separate balance sheets. This could also allow banks to design RBTs more flexibly (eg with lower KYC requirements). In the end, banks may prefer RBTs over tokenised deposits.

RBTs may disintermediate banks in two ways. They could chip away demand deposits in normal times (depending on the relative use cases) and also time deposits during stress (eg due to flight to safety). In the longer run, RBTs may have structural implications and lead to narrower financial institutions. This would include RBT, stablecoin and e-money issuers that specialise in payments, and banks that focus on accepting time deposits (savings) and lending. These narrower and less complex institutions would likely be less risky and also easier to regulate.5 And while they may miss economies of scope that multi-purpose banks enjoy, robust data-sharing arrangements (eg open finance) could help preserve synergies across activities.

Meanwhile, as an alternative payment method, RBTs are poised to diminish the market share of conventional payment instruments such as cash and bank deposits. While replacing cash would have no impact on the central bank balance sheet, replacing deposits would. The magnitude of expansion, however, would be less than one-to-one relative to RBTs issued as deposits are also fractionally backed. Nonetheless, if the public perceives RBTs as a safe haven, significant demand could still arise and amplify the balance sheet impact. This perception could also introduce volatility to the central bank’s balance sheet, particularly during periods of financial stress. Such volatility may present challenges, including asset price fluctuations that affect the central bank’s capital, potential inflationary pressures, and financial stability risks. Central banks’ previous experiences in dealing with larger balance sheets (eg after quantitative easing programs) combined with safety features in the design of RBTs (eg wallet limits) and a gradual rollout could help deal with such risks.

The optimal form of money for an increasingly digitalized future remains uncertain. Therefore, a multi-pronged and experimental approach is necessary today. RBTs represent a unique proposition worth exploring alongside other tokenized money forms. RBTs offer private entities, not just banks, the opportunity to access a new central bank reserve facility, allowing for the development of innovative tokens tailored to sectoral needs. And while widening access to the central bank balance sheet presents new challenges, this is not entirely uncharted territory (eg omnibus accounts in the UK). Ultimately, a single money form may emerge dominant, but it is more likely that multiple forms coexist, interoperate, and serve different use cases.

For example, see Kahn, C. and Singh, M. (2021) ‘If stablecoins are money, they should be backed by reserves’, Risk.net, Feb and Adrian, T. and Mancini-Griffoli, T. (2021) ‘The rise of digital money’, Annual Review of Financial Economics, 13, 57-77.

Bank of England (2023) ‘Regulatory regime for systemic payment systems using stablecoins and related service providers’, Bank of England Discussion Paper, November.

Garratt, R. and Shin, H. S. (2023) ‘Stablecoins versus tokenised deposits: implications for the singleness of money’, BIS Bulletin No 73.

BIS (2023a), ‘Blueprint for the future monetary system: improving the old, enabling the new’, BIS Annual Economic Report, Chapter III, June.

See, for instance, Fisher, I. (1936) ‘100% Money and the Public Debt’, Economic Forum, 406-420 and Friedman, M. (1960) ‘A program for monetary stability’ for early arguments in favour of narrow banking.