Introduction

Household inflation expectations are characterized by strong heterogeneity. While some of this heterogeneity can be related to, for example, inflation experiences (Malmendier and Nagel, 2016), IQ (D’Acunto et al., 2019), age, education, gender, and financial literacy (Bruine de Bruin et al., 2010), most of the heterogeneity remains unexplained. Based on a new survey of German households, we explore to which extent the information channels that households use to inform themselves about monetary policy contribute to explaining variation in inflation expectations. Although these information channels are closely related to the same socioeconomic characteristics that explain inflation expectations, we find strong evidence that information channels have a stand-alone effect on quantitative inflation expectations. Specifically, households who rely on traditional media such as newspapers or television have lower and more accurate views of inflation over the last year, lower inflation expectations for the coming year, and are less uncertain about inflation than households which do not inform themselves. Thus, information channels do not only affect the level of expected inflation but also inflation uncertainty. We show that inflation uncertainty is particularly high among those who use social media to find out about monetary policy. In sharp contrast, we find that information channels do not explain qualitative inflation expectations. Instead, individual inflation experiences determine beliefs about whether inflation will go up or down. Individuals with higher inflation experience are more likely to expect that inflation will increase than individuals with lower inflation experience. Similarly, the expected response of inflation to an unexpected change in the interest rate by the European Central Bank is driven by experience. We propose the interpretation that households obtain inflation numbers from the media, but their “economic model” is shaped by experience.

A first look at the data

Our analysis is based on data from the Bundesbank Online Pilot Survey on Consumer Expectations (SCE), which covers a representative sample of the German population and contains detailed information about the respondents’ socioeconomic characteristics. We focus on the subset of individuals who participated in the June 2019 wave, to which we contributed two specific questions on information channels and a hypothetical interest-rate increase.

Individuals were asked to provide a point prediction of the German rate of inflation (CPI-based) over the previous and the next twelve months. We refer to the former as perceived and to the latter as expected inflation. On average, expected inflation was 2.5%, while actual inflation turned out to be 0.6% only.1 Thus, in line with previous literature, we find that households overestimate inflation.

In the SCE, we asked a question on the information channels through which individuals find out about the ECB’s monetary policy. From the following answers, individuals were allowed to select all those that apply: i) traditional media, ii) social media, iii) ECB communication channels, iv) other sources, and v) “I do not follow the ECB’s monetary policy”.

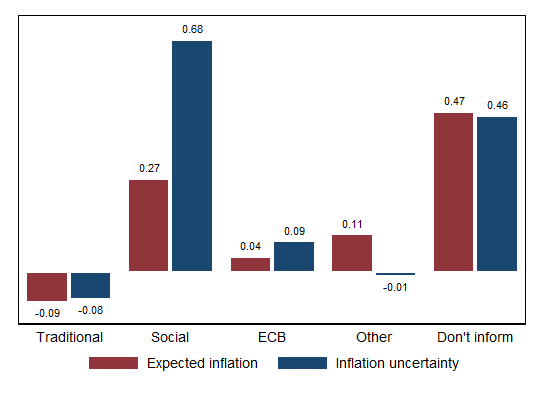

Figure 1 shows the average inflation expectation within each of these groups minus the average inflation expectation in the full sample (red bars). Households who rely on traditional media have below average inflation expectations, while households who do not inform themselves have the highest inflation expectations.

The Bundesbank survey also asked for histogram forecasts for the rate of inflation over the next twelve months. We measure individual inflation uncertainty by the standard deviation of the histogram forecast. The blue bars in Figure 1 depict the average inflation uncertainty within each group minus the full-sample average inflation uncertainty. The figure reveals that users of social media are most uncertain, while users of traditional media are least uncertain.

Figure 1: The figure shows the average expected inflation conditional on the information channel minus the unconditional average of expected inflation (red bars) and the average inflation uncertainty conditional on the information channel minus the unconditional average of inflation uncertainty (blue bars). On average, expected inflation and inflation uncertainty were equal to 2.50% and 1.60%, respectively. All deviations are expressed in percentage points.

Finally, SCE participants were asked for their qualitative inflation expectations. Specifically, individuals were asked whether they believe that the inflation rate would decrease (significantly or slightly), stay roughly the same, or increase (slightly or significantly). We find that the qualitative inflation expectations are well aligned with the quantitative expectations: on average, individuals who expect that inflation will decrease, stay the same, or increase have expected inflation rates of 1.65%, 2.16%, and 2.74%, respectively.

Although Figure 1 provides preliminary evidence for a link between information channels and inflation expectations, drawing strong conclusions would be premature: the same variables that have predictive power for inflation expectations are also strong predictors of household information channels. For example, higher education and income increase the likelihood of using traditional media and of reporting low inflation expectations. Similarly, women are less likely to inform themselves about monetary policy than men and hold, on average, higher inflation expectations. Older individuals are more likely to use traditional media and have experienced higher inflation rates in the past. Thus, we control for those characteristics when exploring the effect of information channels on inflation expectations.

Does media make inflation expectations?

Quantitative expectations

In a first step, we regress households’ perceived and expected inflation rates on information channels, inflation experiences, and socioeconomic characteristics.2

Traditional media turn out to be highly relevant. For individuals who use this information channel, perceived and expected inflation is roughly 0.55 percentage points lower than for individuals who do not inform themselves about monetary policy. Given that the average inflation expectation is 2.5%, this is a sizable effect. While traditional media directly affect perceived inflation, the effect on expected inflation may be direct (e.g., by providing inflation forecasts) and/or indirect via perceived inflation (i.e., by providing current inflation numbers, which in turn influence expectations). Our regressions suggest that the effect on expected inflation mainly works indirectly via perceived inflation. Because perceived and expected inflation are too high on average, households that rely on traditional media have more accurate expectations.

We find no evidence that lifetime inflation experiences affect perceived inflation and only weak evidence that they affect expected inflation. The latter finding is in contrast to Malmendier and Nagel (2016) but consistent with the notion that individuals do not remember inflation experience in the form of numerical values. However, we also acknowledge that we might fail to detect an existing relationship in our data set, as it lacks a time series dimension.

Our results regarding socioeconomic characteristics like gender, education, income and age are broadly in line with the previous literature. Additionally, we find that households without housing property tend to display higher perceived and expected inflation.

Inflation uncertainty

Information channels also play a prominent role in explaining inflation uncertainty. The average inflation uncertainty in our sample is 1.6%. While using traditional media reduces inflation uncertainty by 0.34 percentage points, following social media increases it by 0.54 percentage points. Again, both effects are relative to those individuals who do not inform themselves. The finding that users of social media are more uncertain about future inflation suggests that central banks should put more emphasis on disseminating accurate information through channels other than traditional media (see also Bundesbank, 2019).

Inflation experiences are an important determinant of inflation uncertainty. We find that inflation uncertainty decreases by 0.25 percentage points if inflation experience increases by one standard deviation (0.36%). This finding is consistent with the empirical observation that higher levels of inflation typically go hand in hand with higher inflation variability (Conrad and Hartmann, 2019). Individuals who have experienced phases of high inflation and, as a result, also high inflation volatility might therefore be more certain about the inflation outlook in the current low inflation environment.

Qualitative inflation expectations

We now turn to the analysis of qualitative expectations. Probit regressions for qualitative inflation expectations lead to strikingly different results. Information channels are uninformative about households’ expected direction of inflation. In sharp contrast, lifetime inflation experiences play a crucial role. In the low inflation environment of June 2019, individuals who have experienced higher inflation rates in the past are more likely to expect an increase in the inflation rate. For example, the probability that an individual expects an increase in inflation rises by 14.47 percentage points when switching from an individual with inflation experience at the 5th percentile (corresponding to 1.29%) to an individual with experience at the 95th percentile (corresponding to 1.62%). In line with Malmendier and Nagel (2016), our estimates suggest that individuals consider inflation experiences from large parts of their life when asked for their qualitative inflation expectations.

Interpretation

To sum up, our results suggest that households learn about the level of current and future inflation rates primarily from traditional media, but individual inflation experience is key for explaining the expected change in inflation. A potential explanation would be that traditional media are important for obtaining the correct figures, i.e., for gaining an accurate picture of the current state of the economy, such as actual inflation numbers. In contrast, qualitative inflation expectations might be driven by the ‟economic model” that the households entertain. This model could be shaped by individual experiences.3

Response to changes in the policy rate

We provide further support for our proposed interpretation by studying how households react to an unexpected change in the policy rate. Specifically, we asked the households that participated in the SCE how they would update their inflation expectations in response to an unexpected increase in the policy rate by the ECB. First, we find that most households do not update their inflation expectations at all and that more households adjust upwards rather than downwards. Although the latter finding is at odds with standard theory, it has been previously observed for households and is in line with the notion that the increase in the interest rate has an information effect (Eminidou et al., 2020) or that households entertain a misspecified model of the effect of monetary policy shocks on inflation (Andre et al., 2019, Candia et al., 2020). Second, by running probit regressions, we show that information channels do not explain this expectation updating. Inflation experiences, in contrast, have strong predictive power: individuals with experience of higher inflation are more likely to revise their inflation expectations upwards in response to an unexpected increase in the interest rate. We suggest two potential interpretations. First, households might have experienced rising interest rates during times of high inflation and hence mentally connect these two phenomena. Second, and alternatively, high experienced inflation rates could impact negatively on the perception that monetary policy is capable of reducing inflation. In both cases, inflation experiences (rather than information channels) have shaped the economic model used by individuals.

Conclusion

We interpret our findings as follows. Only traditional media provide households with comparatively accurate information about the level of inflation. This result can be rationalized by a high information content and a comprehensible coverage of inflation and monetary policy in traditional media. Perceived inflation and quantitative forecasts, which typically do not move too far away from perceived inflation rates, are, therefore, very dependent on the information channel used. In contrast, lifetime inflation experience appears to play a limited role.

When forming expectations about the direction of future inflation, however, experience is crucial, while information channels are less important. This finding is consistent with the hypothesis that experiences, rather than information channels, influence individuals’ “economic model”, i.e., how agents think about the basic mechanics of the economy. This is supported by our observations regarding the answers to a thought experiment in which the European Central Bank unexpectedly raises interest rates.

Our finding that users of social media – mainly younger individuals – are most uncertain about future inflation, suggests that central banks should not focus exclusively on direct central bank information channels to communicate news about monetary policy. Instead, they should communicate in a way that ensures coverage in the broader media. ∎

Andre, P., C. Pizzinelli, C. Roth, and J. Wohlfart (2019). Subjective models of the macroeconomy: Evidence from experts and a representative sample. CESifo Working Paper 7850.

Bruine de Bruin, W., W. Vanderklaauw, J. S. Downs, B. Fischhoff, G. Topa, and O. Amantier (2010). Expectations of inflation: The role of demographic variables, expectation formation, and financial literacy. The Journal of Consumer Affairs 44 (2), 381-402.

Bundesbank (2019). The relevance of surveys of expectations for the Deutsche Bundesbank. Monthly Report 12/19.

Candia, B., O. Coibion, and Y. Gorodnichenko (2020). Communication and the beliefs of economic agents. NBER Working Paper 27800.

Conrad, C. and M. Hartmann (2019). On the determinants of long-run inflation uncertainty: Evidence from a panel of 17 developed economies. European Journal of Political Economy 56, 233-250.

D’Acunto, F., D. Hoang and M. Paloviita and M. Weber (2019). Cognitive abilities and inflation expectations. American Economic Review, Papers & Proceedings 102, 562-566.

Eminidou, S., M. Zachariadis, and E. Andreou (2020). Inflation expectations and monetary policy surprises. Scandinavian Journal of Economics 122 (1), 306-339.

Malmendier, U. and S. Nagel (2011). Depression babies: Do macroeconomic experiences affect risk taking? The Quarterly Journal of Economics 126 (1), 373-416.

Malmendier, U. and S. Nagel (2016). Learning from inflation experiences. The Quarterly Journal of Economics 131 (1), 53-87.

Following Bundesbank (2019), we focus on individuals with expectations in the range of -12% to 12%.