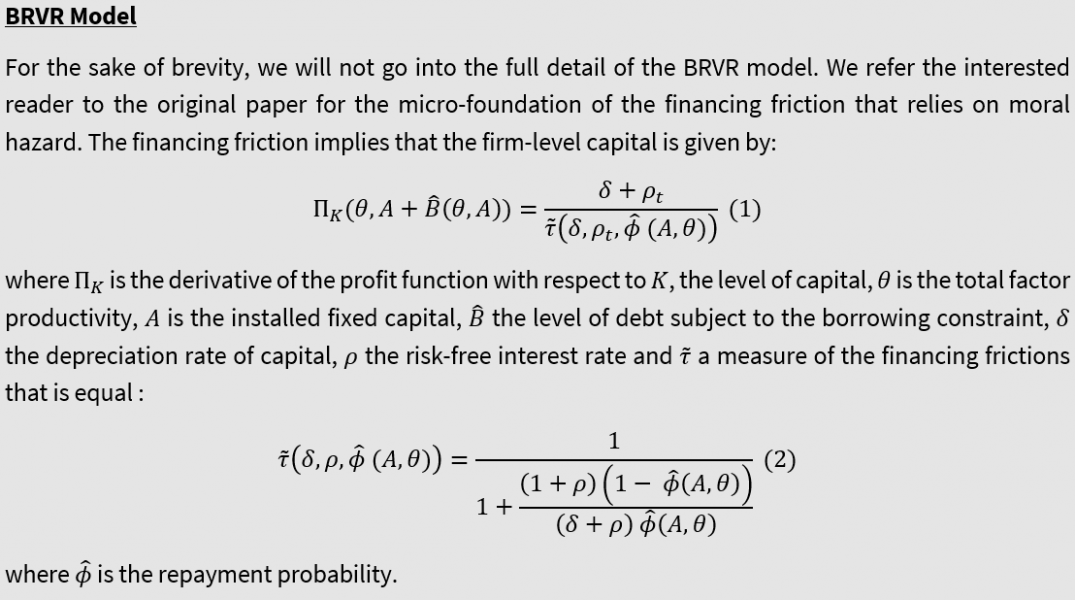

References

Besley, T. J., Roland, I. A., & Van Reenen, J. (2020). The aggregate consequences of default risk: evidence from firm-level data (No. w26686). National Bureau of Economic Research.

Buera, Francisco J. and Yongseok Shin. 2011. “Self-Insurance vs. Self-Financing: A Welfare Analysis of the Persistence of Shocks.” Journal of Economic Theory 146 (3): 845–862.

Catherine, S., Chaney, T., Huang, Z., Sraer, D. A., & Thesmar, D. (2018). Quantifying reduced-form evidence on collateral constraints. Available at SSRN 2631055.

Chaney, T., Sraer, D., & Thesmar, D. (2012). The collateral channel: How real estate shocks affect corporate investment. American Economic Review, 102(6), 2381-2409.

Fougère, D., Lecat, R., & Ray, S. (2019). Real estate prices and corporate investment: theory and evidence of heterogeneous effects across firms. Journal of Money, Credit and Banking, 51(6), 1503-1546.

Gertler, M., & Bernanke, B. (1989). Agency Costs, Net Worth and Business Fluctuations. American Economic Review, 79, 14-31.

Holmstrom, B., & Tirole, J. (1997). Financial intermediation, loanable funds, and the real sector. the Quarterly Journal of Economic, 112(3), 663-691.

Hsieh, C. T., & Klenow, P. J. (2009). Misallocation and manufacturing TFP in China and India. The Quarterly journal of Economic, 124(4), 1403-1448.

Khan, Aubhik and Julia K. Thomas. 2013. “Credit Shocks and Aggregate Fluctuations in an Economy with Production Heterogeneity.” Journal of Political Economy 121 (6): 1055–1107.

Midrigan, Virgiliu and Daniel Yi Xu. 2014. “Finance and Misallocation: Evidence from Plant-Level Data.” American Economic Review 104 (2): 422–458.

Moll, Benjamin. 2014. “Productivity Losses from Financial Frictions: Can Self-Financing Undo Capital Misallocation?” American Economic Review 104 (10): 3186–3221.

Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American economic review, 71(3), 393-410.

Appendix A

Appendix B

|

Weighting sectors according to their actual size in the value-added

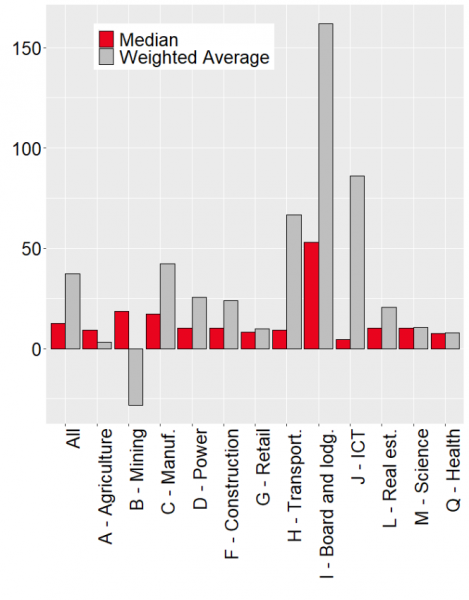

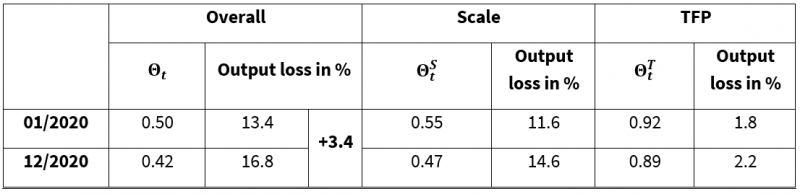

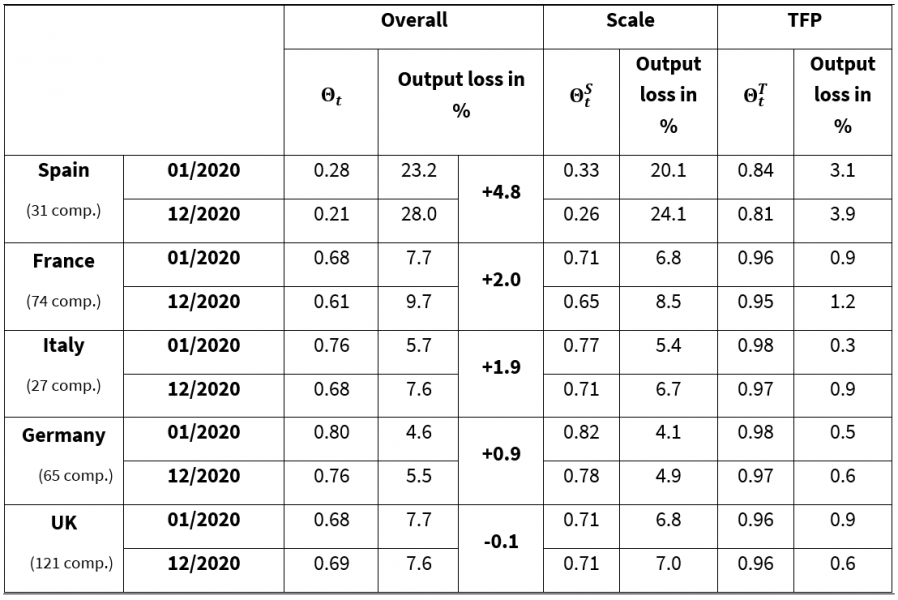

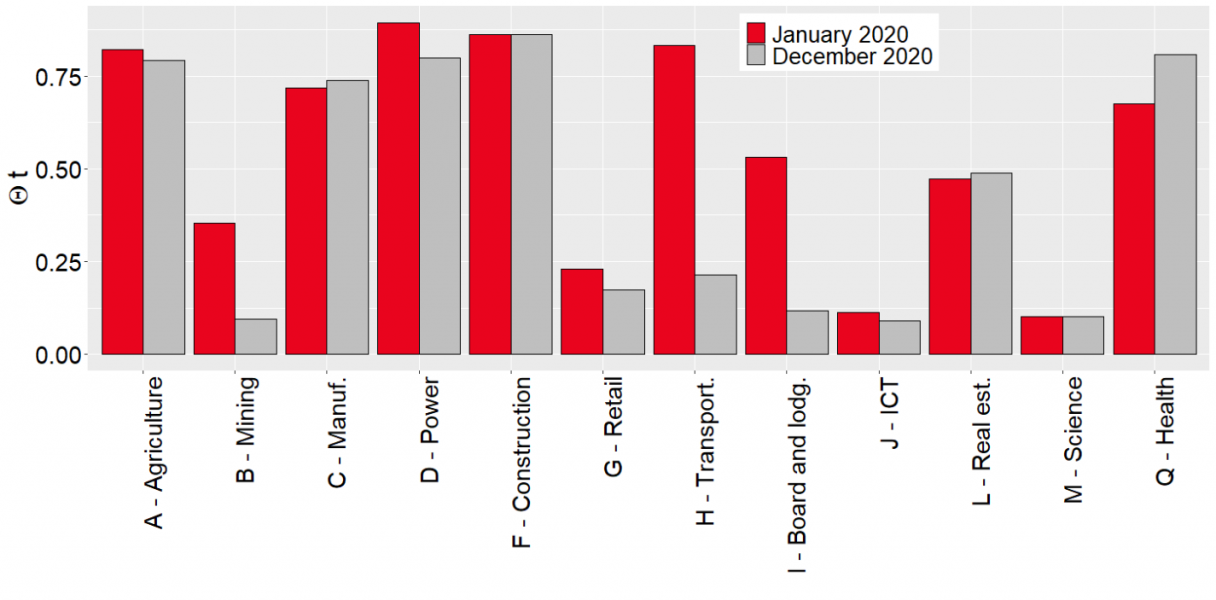

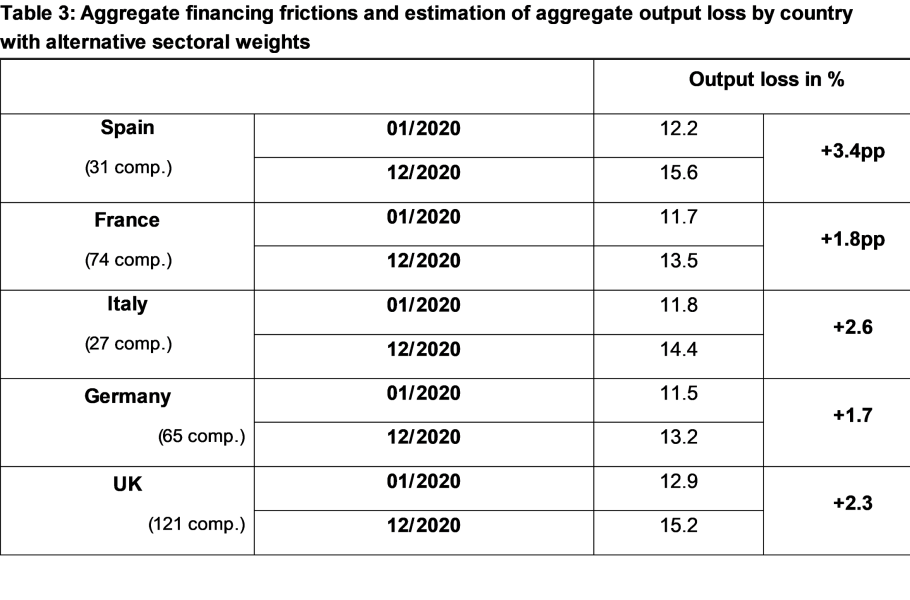

The striking sectoral heterogeneity of the effects of the crisis suggests that the sectoral composition of the sample of listed firms, notably at the country level, is a key determinant of our estimates of the output loses resulting from the crisis.

If the sectoral weights in the sample of listed firms significantly differ from the sectoral weights in the entire economy, our results are likely to be biased.

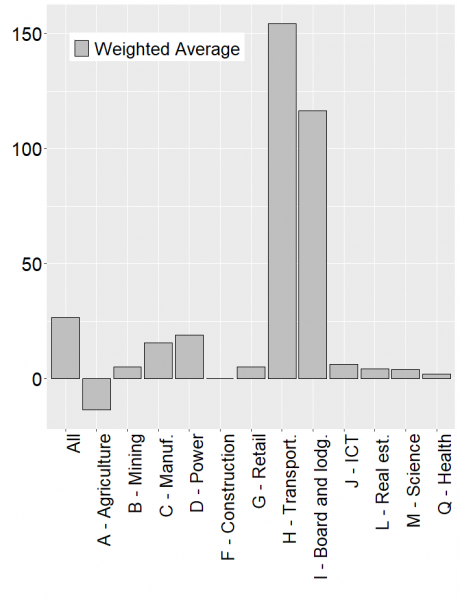

As a robustness check, we compute alternative measures for the aggregate impact of the crisis by weighting the estimated measures of sectoral frictions (i.e. θjt) by the sectoral weight of each sector in the economy, as measured by the number of employees by sector reported by Eurostat.

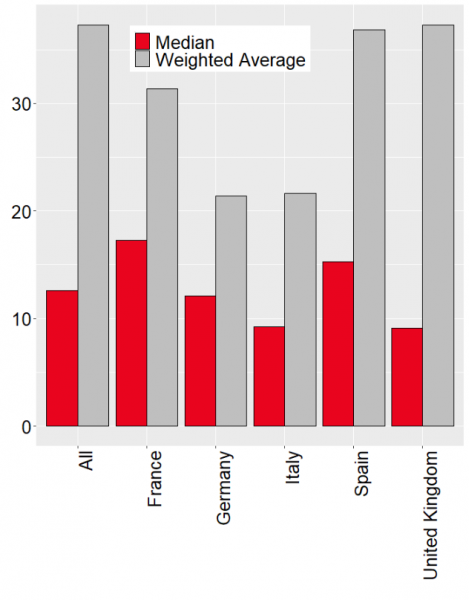

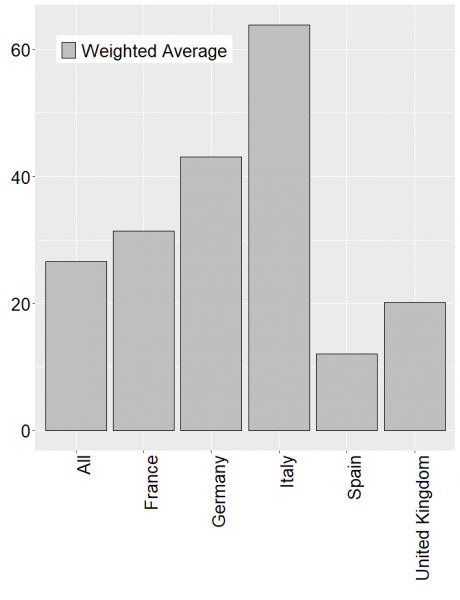

The results reported in Table 3 suggest that these alternative weights do not significantly alter the results at the aggregate level. At the European level, newly weighted frictions are estimated to increase the output loss from 12.0% to 15.2%, that is a 3.2 percentage point increase. At the country level however, the estimated output losses are altered, notably in Germany and in the UK, by this alternative weighting strategy. Using these alternative weights, we estimate that the output losses increase by +1.8pp in France, +1.7pp in Germany, +3.4pp in Spain, +2.6pp in Italy and +2.3pp in the UK.

|