This policy brief is based on ECB Working Paper Series No 2916. The views expressed are those of the authors and do not necessarily reflect those of the ECB.

In this policy brief, we explore the ongoing support of fossil fuel-based firms by banks and assess the role of public guaranteed loans (PGLs) in directing resources towards greener economic activities to facilitate the climate transition process. Using a unique pan-European credit register dataset that integrates supervisory bank data with firm-level greenhouse gas emission data and financial information, our analysis reveals three main findings. First, European banks perceive lending to green companies as riskier compared to their brown counterparts, a phenomenon which we call “green-transition risk”. Second, we provide evidence that during the COVID-19 pandemic, European banks strategically leveraged PGLs to allocate resources towards environmentally sustainable activities, thereby increasing the proportion of green loans in their portfolios and partially transferring the inherent “green-transition risk” to European governments and citizens. Third, our study shows that banks prefer giving PGLs to financially strong green firms rather than those that are less profitable and more in debt, which could challenge the financial support needed by green businesses during the pandemic.

Over the last few years, policymakers, governments, and supranational institutions have devoted increasing attention to environmental factors, introducing ad-hoc regulations and initiatives aimed at reducing CO2 emissions (Bolton and Kacperczyk, 2021). These efforts all aim to fight climate change and protect public health. Achieving a carbon-neutral economy necessitates fundamental shifts in our existing economic structures. Transitioning to renewable energy systems requires comprehensive changes across various sectors. It involves the development and deployment of new technologies, infrastructure upgrades, changes in energy production, distribution, and consumption patterns. It also entails promoting energy efficiency and implementing policies that incentivize the adoption of renewable energy solutions. Banks are positioned to play a pivotal role in this transformation by directing funds and penalizing firms that do not adhere to environmental benchmarks, particularly in Europe where corporate financing is predominantly bank-driven. However, banks continue to finance a substantial number of enterprises reliant on fossil fuels (Kacperczyk and Peydro, 2021; Laeven and Popov, 2023). In Buchetti et al. (2024), we investigate the dilemma faced by financial institutions, caught between promoting green financing, driven by regulatory demands and sustainability goals, and the challenges of unfamiliar climate policies and the hidden costs of greener technologies.

To examine why banks, continue to finance a substantial number of enterprises reliant on fossil fuels, we assess the default probabilities (PDs) for companies within identical industry location-size (ILS) clusters, comparing them based on their greenhouse gas (GHG) emission intensity. Furthermore, we explore a potential remedy to lessen the green transition risk and incentivize green financing. We propose that PGLs could enable banks to move their portfolios towards more sustainable firms by offering protection against the increased default probabilities. The PGL model ensures that banks are not solely responsible for the heightened risk of default when financing eco-friendlier businesses, as the government absorbs this risk. This incentivizes banks to extend more credit to sustainable enterprises, thereby aligning their lending practices with the expectations of regulators and policymakers regarding climate and environmental risks.

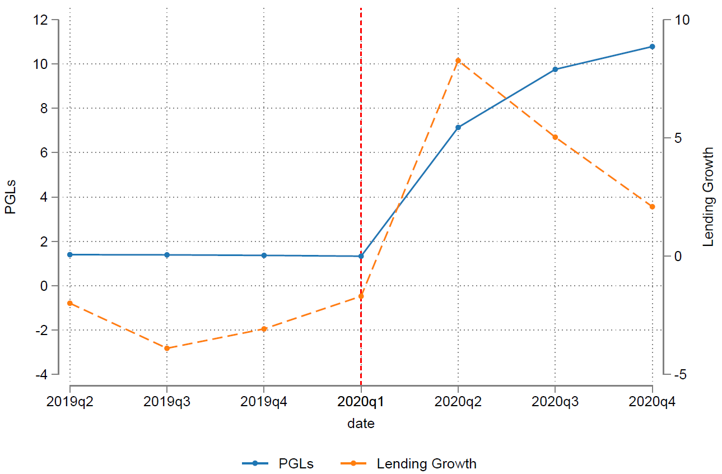

Therefore, the introduction of the PGL framework during the COVID-19 pandemic can offer valuable support by transferring default risk (partially or entirely) to the government (and thereby public finances), potentially encouraging banks to increase their lending (Figure 1). Indeed, we find that this implicit protection may encourage banks to “take on more risks”, providing more credit to greener companies at the expense of browner companies. In this way, banks may “kill two birds with one stone”: transferring default risk (partially or entirely) to the government while decarbonizing their lending portfolio and fulfilling the expectations of supervisors and policymakers regarding the reduction of climate-related and environmental risks. To test this hypothesis, we exploit the deployment of PGLs during the COVID-19 pandemic and investigate whether these have been directed primarily towards greener firms.

Figure 1: An analysis of the dynamics surrounding the key variable of interest

(Public Guarantee Loans (PGLs) and Lending Growth)

Notes: The blue line represents the proportion of loans subject to government guarantees at the bank-firm level. In contrast, the dashed orange line depicts Lending Growth, capturing the logarithmic changes in outstanding nominal loan amounts as they move from bank i to firm f.

Our findings highlight three key points. First, EU banks perceive lending to environmentally friendly (‘green’) companies as riskier compared to lending to traditional (‘brown’) firms, a situation we describe as ‘green-transition risk’. Second, the study finds that throughout the COVID-19 pandemic, European banks strategically used PGLs to direct resources towards green initiatives, thereby increasing the share of green loans in their portfolios and effectively transferring some of the green transition risks to European governments and the public. Third, banks prefer granting PGLs to financially stable green companies rather than to less profitable, highly indebted green companies, a trend that might hinder the ability of financially needy green enterprises to obtain support during the COVID-19 crisis.

These findings underscore the dilemma faced by financial institutions, which are motivated to pursue green lending to achieve sustainability targets and comply with regulatory demands but are hindered by the perceived riskiness of such investments. This risk perception is fueled by uncertainties and potential hidden costs linked to green technologies and initiatives, alongside the evolving nature of climate policies which lack consistent predictability. These uncertainties hinder banks’ capacity to evaluate and manage climate-related risks effectively, influencing investment decisions, elevating capital costs, and restricting support for low-carbon ventures. In essence, banks are caught between the incentives for green lending and the perceived risks that accompany it, due to uncertainties in future developments and costs associated with eco-friendly technologies and projects.

This policy brief investigates why banks might prefer financing more traditional, ‘browner’ firms. We suggest that the hesitancy to shift towards greener investments may stem from the perceived elevated risks linked with green financing, leading to heightened capital allocation and monitoring expenses. We refer to this as ‘green-transition-risk,’ where banks view engagements with eco-friendly firms as riskier than with their less environmentally conscious counterparts. We argue that introducing green public guarantee lending frameworks could mitigate these barriers and shift market dynamics to a new equilibrium, where green lending becomes more competitive and achieves better outcomes. Our findings are crucial for European policymakers. By strategically utilizing PGLs, governments can alter banking practices to foster the growth of sustainable industries and advance the decarbonization of the global economy. Our research enriches the dialogue on how the banking sector and governmental interventions, via PGLs, can facilitate the green transition. The examined large-scale PGLs schemes, designed to uphold private credit during the COVID-19 crisis, underscore the dual role of PGLs: as a reaction to shocks impairing economic fundamentals and as an incentive for potentially credit-restricted businesses under normal circumstances. The success of PGLs in promoting the green transition centres on the ability of policymakers to shape and implement these government-supported credit guarantees.

It is crucial to realize a delicate balance: policymakers need to incentivize banks to fund eco-friendly enterprises without promoting excessive risk-taking, which could if over-relied upon, strain public finances and impact European citizens. Policymakers are advised to set forth suitable eligibility conditions, oversight processes, and pricing strategies for loans to ensure PGLs benefit the intended entities without unnecessarily intensifying the risk profile of the banks’ lending portfolios.

Bolton, P. and Kacperczyk, M. (2021). Do investors care about carbon risk? Journal of Financial Economics, 142(2):517–549.

Buchetti, B., Miquel-Flores, I., Perdichizzi, S., and Reghezza, A. (2024). Greening the economy: How public-guaranteed loans influence firm-level resource allocation. ECB Working Paper Series.

Kacperczyk, M. and Peydro, J.-L. (2021). Carbon emissions and the bank-lending channel. Technical report, Centre for Economic Policy Research.

Laeven, L. and Popov, A. (2023). Carbon taxes and the geography of fossil lending. Journal of International Economics, 144:103797.