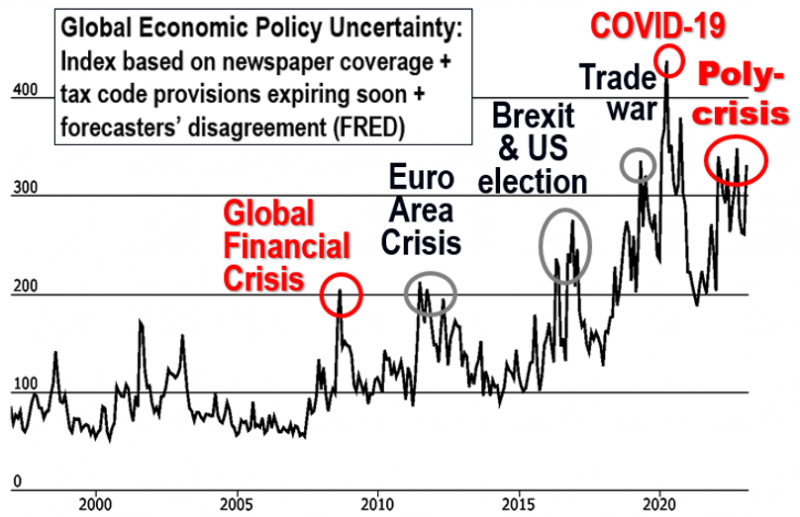

In economics, uncertainty is often defined as a non-quantifiable risk. Its probability and impact can hardly be predicted, especially in the absence of historical precedent. This applied both to the financial virus (US “subprime” loans hidden in securitized baskets) and the invisible coronavirus that triggered respectively the GFC and the GCC (for more, see my 2020 paper). Given the conjunction of the Russian war at the border of the European Union (and NATO), while US-Chinese tensions are climbing about trade and Taiwan, “uncertainty” currently remains a buzz word.

Chart 1: Index of Global Economic Policy Uncertainty (updated until end of June 2023, FRED)

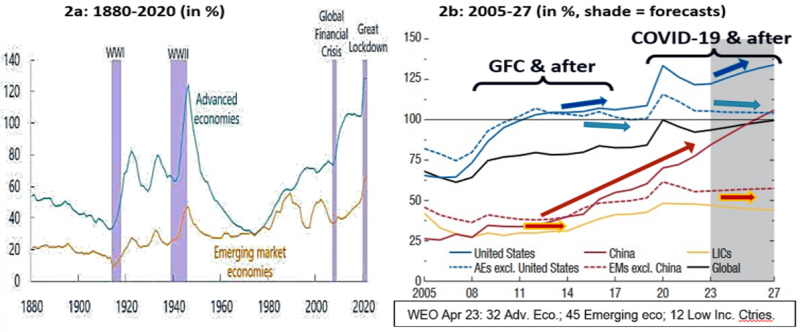

Chart 2: Public Debt/GDP in Advanced and Emerging Economies: long-term vs current (Source: IMF)

Let’s just recall here that mid-sized US banks were exempted from most of the regulatory reforms. In addition, the three US banks which failed in the first semester of 2023 had been poorly supervised despite bad management, notably in terms of liquidity and interest rate risks.

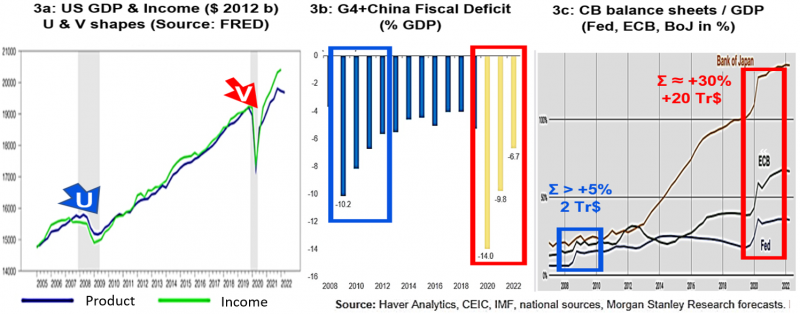

Chart 3: Examples of recession shapes, fiscal supports and monetary accommodations

Given higher public debt ratios in 2019 than in 2008, the fiscal space should logically have been slimmer. Yet Chart 3b aggregating China and the G4 (US + EA + Japan + UK) confirms that fiscal deficits over GDP plus China were larger to tackle the COVID-19 shock (in red) than during the GFC (in blue). Although interest rates were often already low, Chart 3c also confirms that monetary policy was more accommodative: see the rise in major central banks’ balance sheets, for instance, as QE was revived. Among the reasons why authorities could react more sharply were: the sense of urgency; the lack of precedent (the Spanish flu dating 100 years ago); the GFC lessons and also the absence of an obvious guilt, since it is more popular to subsidize people than banks!

Meanwhile, Chinese-US tensions regarding trade and Taiwan keep elevating. And even if there was no global financial crisis, international finance has become more of a weapon; examples with payment systems are evoked in my 2023 Policy Note.

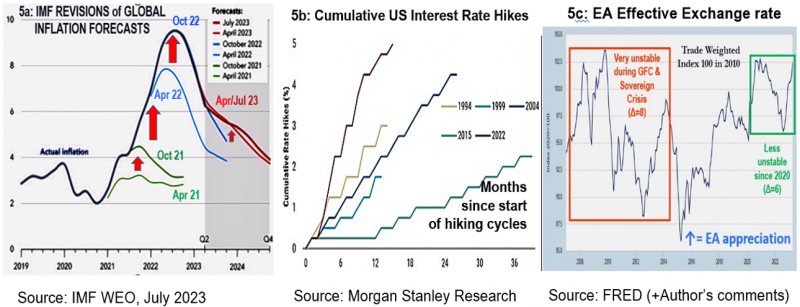

Chart 5: 5a. IMF Forecasts’ Revisions; 5b. Fed Hiking Cycles; 5c. Euro Area Effective Exchange Rate