The views expressed in this contribution do not necessarily reflect the official position of the institutions with which the authors are affiliated or for which they work.

Major economic downturns leave important scars on the path of economic expansion. Drawing on data of 26 OECD countries since 1970 we show that fiscal expansions can mitigate scarring effects provided they boost government investment. However, active fiscal expansions are, on average, skewed towards current expenditure, and economies do not return to their pre-crisis trends exposing governments to sustainability risks. Policy makers face an important dilemma: (i) design fiscal support for the short run while taking into account long-term effects; and (ii) pivot in time from stabilisation to consolidation without cutting public investment.

To those committed to the Keynesian paradigm, the prominent role fiscal policy played during the Covid-19 pandemic was an overdue rehabilitation. Long shunned as slow and ill-timed, the forceful expansion of government budgets through borrowing effectively mitigated the short-term economic impact caused by the strict lockdown measures. Without it, the pandemic would undoubtedly have been much more disruptive for households and firms. However, as much as a single swallow does not make a summer, the effectiveness of fiscal policy during the Covid-19 pandemic does not undo a long history of mixed successes.

Since the early 1970s, major economic downturns have regularly come with lasting effects in spite of valiant attempts of fiscal policy makers to lean against the wind. Prominent studies by Blanchard et al. (2015) and Martin et al. (2015) offer a comprehensive and revealing overview of how output does not return to pre-crisis trends. To be clear, that output does not follow a linear trend is not a new insight. The two studies are just particularly prominent examples of a debate that gained new momentum in the wake of the Global Financial Crisis. Its roots reach back to the early 1980s, when Beveridge and Nelson (1981) and Nelson and Plosser (1982) convincingly showed that in sharp contrast to the notion prevailing at the time − and to some extent still today − the path of economic expansion is characterised by variable not stable trends.

Can fiscal policy avert or mitigate the scarring effects of major economic downturns? This question may sound odd to some ears. While there is no agreement on the exact size of fiscal multipliers, there is a very broad consensus that expansionary fiscal policy will typically boost economic activity − at least in the short run − ideally back to the trend observed before an economy enters a recession. So how can we reconcile the established effectiveness of fiscal stabilisation in the short run with the overwhelming evidence of scarring in the medium and long run?

In a recent paper, we shed light on this important issue. We analyse major economic downturns in 26 OECD countries, of which 14 in the EU, since the 1970s.2 We characterise the behaviour of fiscal policy before, during and after major recessions to establish a possible link between the short-term response and medium-term economic outcomes. We show that while fiscal policy can mitigate scarring effects, policy makers do generally not give enough attention to government investment. Moreover, economies do not return to their pre-crisis trend exposing governments to sustainability risks.

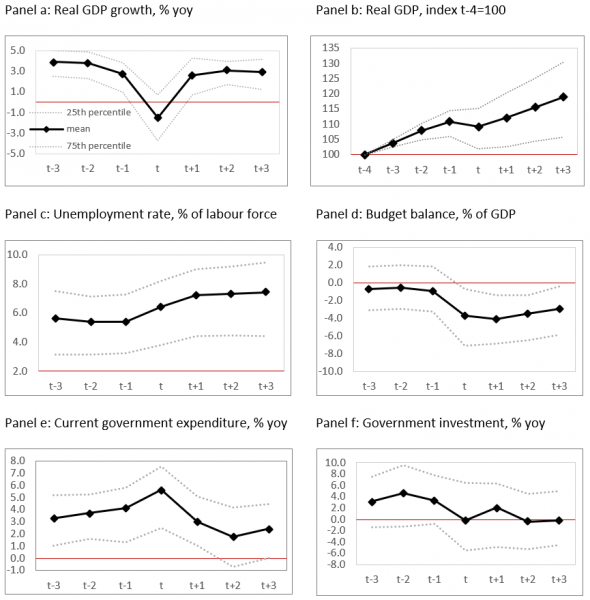

Figure 1 shows the average profile of how economies and fiscal policy behave around the more than 100 episodes of major economic downturns identified in our sample.3 For illustrative purposes, we focus on a time window of seven years: starting three years prior and ending three years after the downturn. The dotted lines are the 25th and 75th percentile; they provide an indication of the variability in the sample. Starting with real GDP (Panel a), economic activity drops in the year of the downturn − on average by around 2% on the previous year − and recovers in the following years. However, the recovery is fairly contained. Most importantly, economic growth does not overshoot the rates recorded prior to the recession, but actually drops to slightly lower numbers. As a result, real GDP resumes an upward trend but stays below the one recorded prior to the recession (Panel b). The downward shift of the trend is an indication of the lasting effect of the crisis. Employment recovers even less than output (Panel c), leaving countries with more jobseekers in percent of the labour force.4

Figure 1: Stylised facts of major economic downturns

Sources: OECD, own calculations.

Fiscal policy reacts quite forcefully, but focuses on the short term. On average, the budget deficit swells to close to 4% of GDP in the year of the recession, up from around 0.5% of GDP in the three years preceding the economic downturn (Panel d). The bulk of the fiscal impulse – around two thirds – stems from the operation of automatic stabilisers: discretionary spending is broadly kept in line with original plans and revenue losses are replaced with borrowing.5 In addition, governments typically accelerate current expenditure (Panel e) but pull the handbrake on public investment (Panel f). In the recovery phase, automatic stabilisers go into reverse and governments also reign in the expansion of current government expenditure. However, due to the permanent loss in output this is not enough to bring the deficit back to pre-recession levels. Public investment is adjusted downward, at the cost of weighing on economic growth further down the road.

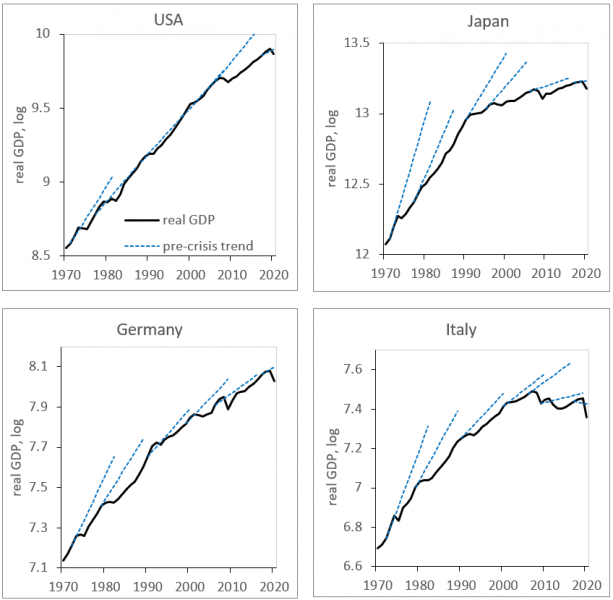

Quantifying the scarring effects of major economic downturns is not straightforward as there is no observable counterfactual. We cannot know for sure the course an economy would have followed had it not been affected by a recession. In our paper we adopt a pragmatic approach repeatedly tested in the literature: an extrapolation of the pre-crisis trend.6 Figure 2 illustrates the method for four larger countries: the US, Japan, Germany and Italy. The sequence of straight lines springing from actual real GDP are the constructed counterfactual trends of economic activity. The pattern of variable trends is clearly visible: In the wake of major downturns, real GDP typically embarks on a lower path of economic expansion.

Figure 2: Real GDP with pre-crisis trends of USA, Japan, Germany and Italy

Sources: OECD, own calculations.

We measure the size of scarring as the average difference between the pre-crisis trend and the actual evolution of real GDP in the 3 to 7 years after the major economic downturn. The focus on the medium term is motivated by the main objective of our analysis: we want to find out whether the short-term fiscal response – in terms of both size and composition – has any bearing on economic performance once the economic recession is over. The average annual scarring effect in our sample turns out to be quite large: it amounts to around 2%. Since the average drop of real GDP during economic downturns in our sample is about the same size, it means that the initial loss of output is not recovered; it turns out to be lasting. Averages obviously mask considerable variation across episodes and countries, but scarring effects of the size revealed in our sample have important implications and beg important questions for budgetary policies.

First, absent budgetary corrections after the recession, a lasting downward shift in GDP inevitably translates into a corresponding reduction in the level of government revenues and, ceteris paribus, into a lower budget surplus or higher deficit; issues of sustainability arise. With a budgetary sensitivity to the cycle of around 0.5, 2% of scarring per year translate, everything else equal, into a 1% of GDP permanent increase in the budget deficit.

Second, the ambition of stabilising output via expansionary fiscal policy is deeply rooted in all advance economies ever since Keynes postulated his theory of how to manage economic depressions in the 1930s. How can we explain the pervasive pattern of lasting shortfalls of real GDP after major economic downturns in spite of the quite forceful response of fiscal policy outlined above? More importantly, are there ways for fiscal policy to avert or at least mitigate scarring effects? Our rich data set offers a unique opportunity to shed some light on this critical policy issue. We ran a battery of regressions exposing our estimates of scarring to a series of potential determinants including in particular measures of the fiscal response.

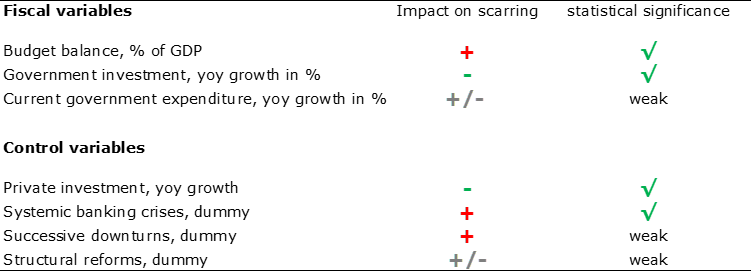

Table 1: Determinants of scarring – summary of our regression analysis

(Dependent variable = average scarring after major economic downturns)

Notes: A negative (positive) sign means that a variable is associated with lower (higher) scarring effects. The budget balance and the growth rate of government investment, current government expenditure and private investment are measured as difference with respect to the average of the 3 years prior to the economic downturn. Systemic banking crisis dummy as defined by Laeven, L. and Valencia, F. (2018) Systemic Banking Crises Revisited, IMF Working Paper, 18/206. Successive downturn dummy=1 if an economic downturn is followed by another downturn in t+2 to t+7. Structural reform dummy as defined by Duval, R. D. Furceri, B. Hu, J. Tovar Jalles, H. Nguyen (2018) A Narrative Database of Major Labor and Product Market Reforms in Advanced Economies, IMF Working Paper, WP/18/19.

Our findings − summarised in qualitative terms in Table 1 − are encouraging and discouraging at the same time.7 Starting with the bad news, our findings do not support the view that anything that stimulates demand in the short term mitigates scarring effects. The change in the budget balance yields stable results across alternative specifications: A higher deficit in the year of the downturn goes along with a higher scarring effect in the medium term. This is not entirely surprising. Handing out income support through higher current spending or simply keeping previously adopted expenditure plans on track when the economy tanks does not help address structural or supply side issues triggered by severe economic downturns. This is not to say that plain fiscal expansions are completely ineffective. On the contrary, most estimates of short-run fiscal multipliers are sizeable, especially in economic bad times.8 However, they tend to reverse fairly quickly.

The good news emerging from our statistical analysis is that a fiscal expansion can mitigate scarring if it involves an increase in government investment expenditure. In fact, our regressions clearly corroborate a plausible prior: government investment, apart from being a component of aggregate demand, can promote economic growth in the medium term through the supply side. In our sample, recessions with a stronger increase in government spending on investment are, everything else equal, followed by a more moderate downward shift in the trend of economic expansion.

However, the mitigating effect of fiscal policy on scarring comes with a snag. For starters, the estimated impact is comparatively small: A one percentage point increase in government investment reduces scarring by less than 0.1 percentage point of GDP, i.e. around 1/20 of the average scarring recorded in our sample. Second, governments have a preference for actively increasing budgetary items that offer a short-term boost, arguably because of their direct impact on voters. Public investment, in contrast, which mitigates scarring in the medium term, does not receive much attention in the fiscal response to major downturns. Moreover, countries with limited fiscal space do not have the means to launch ambitious fiscal responses.

Scarring effects are a recurring feature of major economic downturns. In our sample of 26 advanced OECD economies we identify more than 100 episodes in the period 1970-2019. In most cases, real GDP does not return to the trend observed prior to the downturn but embarks on a lower growth path. Three to seven years after the main shock, economic output still falls on average 2% per year short of the counterfactual level.

Our analysis shows that a fiscal expansion does not mitigate scarring effects unless it involves an increase in government investment. However, the impact turns out to be comparatively small, leaving governments with lower output levels and, by extension, with higher deficits and debt: the fiscal space to react to future negative shocks declines.

To counteract the vicious circle of scarring effects, weaker fiscal positions and back, policy makers would need to jettison deep-rooted habits. Fiscal expansions in the event of a recession make a lot of sense, as long as they are well timed and have the right composition. Timing is usually not a problem in the wake of major economic downturns; they generate the necessary sense of purpose and urgency among policy makers. The more important challenge is getting the composition of the fiscal response right, by giving more space to government investment, and switching from stabilisation to consolidation without cutting government investment.

To avert sustainability issues, two practical measures should be considered. First, over the medium and long term, policy makers should apply a safety margin on current expenditure. To account for scarring, its growth rate should be capped below prevailing estimates of sustainable medium-term potential output growth. Second, active discretionary fiscal expansions in response to major economic downturns should be temporary, ideally with explicit sunset clauses. Increases in current government expenditure exhibit a higher degree of inertia than investment. Once implemented, they are politically difficult to reverse even if the emergency that triggered them is over. Adopting them with an in-built expiry or review date would make a difference.

The way fiscal policy in the EU responded to the Covid-19 pandemic was much better than in the past suggesting that lessons may have been learned. The fiscal response was very quick, in large part targeted towards the health care sector and, most importantly, coupled with the Recovery and Resilience Facility, a major EU initiative to support investment and structural reforms. From this perspective, risks of seeing major scarring effects were certainly reduced.

We deliberately use the past tense because the economic fallout of the Russian invasion of Ukraine has dramatically affected prospects for the medium term. The sharp increase in energy prices ensuing from the war is a prototypical supply shock, which, if not reversed shortly, will require painful structural adjustments. Nonetheless, many governments seem to revert to the misconception that additional deficit spending can solve the problem. At the same time, higher energy prices have heightened the sense of urgency with regard to the green transition, which involves major investment spending including by the government. Time will tell which way the balance will move. Experience certainly supports the view that while plain fiscal stabilisation may help in the short run, it leaves us potentially worse off and more exposed in the medium term.

Ball, L. (2014). Long-term damage from the Great Recession in OECD countries. European Journal of Economics and Economic Policies: Intervention, 11(2), 149-160.

Batini, N., Eyraud, L. Forni, L. and Weber, A. (2014). Fiscal Multipliers: Size, Determinants, and Use in Macroeconomic Projections, IMF Technical Notes and Manuals.

Blanchard, O.J., Cerutti, E. and Summers, L.H. (2015). Inflation and Activity − Two Explorations and their Monetary Policy Implications, IMF Working Paper WP/15/230.

Beveridge, S. and Nelson, C.R. (1981). A new approach to the decomposition of economic time series into permanent and transitory components with particular attention to measurement of the `business cycle’, Journal of Monetary Economics, 7(2), 151-174.

Cerra. V., U. Panizza, and S. C. Saxena (2013). International evidence on Recovery from Recessions, Contemporary Economic Policy, 31(2): 424–439

in’t Veld, J., M. Larch, M. and Vandeweyer (2013). Automatic Fiscal Stabilisers: What They Are and What They Do. Open Economy Review 24: 147–163, https://doi.org/10.1007/s11079-012-9260-6

Harding, D. and Pagan, A. (2002). Dissecting the cycle: a methodological investigation, Journal of Monetary Economics, 49(2), 365-381, https://doi.org/10.1016/S0304-3932(01)00108-8

Martin, R., Munyan, T. and Wilson, B.A. (2015). Potential Output and Recessions: Are We Fooling Ourselves? International Finance Discussions Paper, No. 1145.

Nelson, C R, and C R Plosser (1982). Trends and random walks in macroeconomic time series: some evidence and implications, Journal of Monetary Economics 10(2): 139-162.

Disclaimer: The views expressed in this contribution do not necessarily reflect the official position of the institutions with which the authors are affiliated or for which they work.

Australia, Austria, Belgium, Canada, Switzerland, Germany, Denmark, Spain, Finland, France, United Kingdom. Greece, Ireland, Iceland, Italy, Japan, South Korea, Luxembourg, Mexico, The Netherlands, Norway, New Zealand, Portugal, Sweden, Turkey, USA.

To ensure robustness we use three different identification methods: (i) local minima of real GDP as per Harding, D. and Pagan, A. (2002) Dissecting the cycle: a methodological investigation, Journal of Monetary Economics, 49(2), 365-381; (ii) the output gap turns negative and smaller than -1% of potential GDP; and (iii) year-on-year real GDP growth of a given country decelerates by more than one standard deviation. Due to space constraints, this policy brief focuses on the output gap criterion. The full set of results can be found in our paper. All three criteria support the same conclusions.

These findings are very much in line with earlier studies on the effects of economic downturns or economic crises including in particular those mentioned in the introduction but also Cerra et al. (2013) and Ball (2014).

Governments generally do not lay off nurses, teachers of other public officials in the face of a recession, nor do they cut pensions or other major social transfer categories. Expenditure items directly linked to the cycle are very small relative to total spending and the effects of progressive and regressive taxes tend to wash out on the aggregate (see In ‘t Veld et al. 2013).

The pre-crisis trend is calculated as the 10-year average of real GDP growth. We exclude the two years prior to the crisis to account for the fact that the economy may have been in a boom before entering a recession.

The details of the regression analysis are discussed in Section 5 in our paper.

Batini et al. (2014) offer a comprehensive overview of the empirical literature on fiscal multipliers.