This policy brief is based on: Ruo Chen and Esti Kemp, “Putting Out the NBFire: Lessons from the UK’s Liability-Driven Investment (LDI) Crisis,” IMF Working Papers 2023/210 (Washington: International Monetary Fund). The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Liability Driven Investment (LDI) funds were at the center of the UK gilt market stress in the aftermath of the UK “mini-budget” in September 2022. With imminent and growing financial stability risk, the Bank of England (BoE) undertook temporary gilt purchases on financial stability grounds to restore orderly market conditions and allow LDI funds time to build their capital positions. The LDI crisis echoed past stress episodes in the large and diverse non-bank financial institution (NBFI) sector (the “Dash for Cash” and “Archegos” crises), underscoring common vulnerabilities such as liquidity stress, leverage, and interconnectedness. More broadly the event highlighted key gaps and policy issues related to the monitoring of financial stability risks in the broader NBFI sector for both individual jurisdictions and international standard-setting bodies.

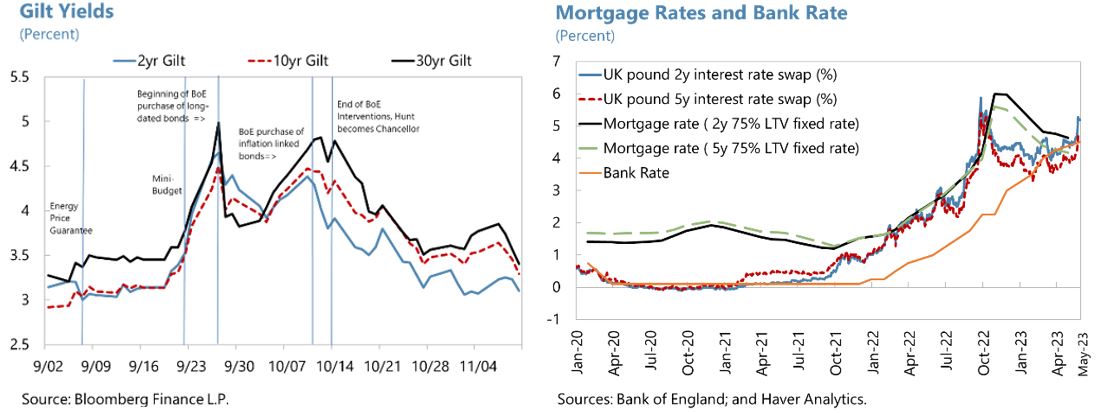

The “mini-budget” in September 2022 unnerved the UK’s core financial markets. While aimed at promoting economic growth, the £45 billion unfunded tax cuts were announced against the backdrop of historically high inflation and increasing yields. In addition, unlike most budgets, this “mini-budget” was not accompanied by an assessment by the Office for Budget Responsibility (OBR), the fiscal watchdog. The market’s concerns about fiscal sustainably, skepticism around growth objectives/impact, and increased uncertainty around how inflation would be brought down, triggered a swift selloff in UK assets. By the following trading day, the pound fell to its lowest-ever level on record (1.03) against the dollar, while gilt prices collapsed. Most strikingly, the 30-year gilt yield jumped by an historic 140 basis points over three days, with moves intensified by the pension funds’ forced sell-off of long-dated gilts (see below).

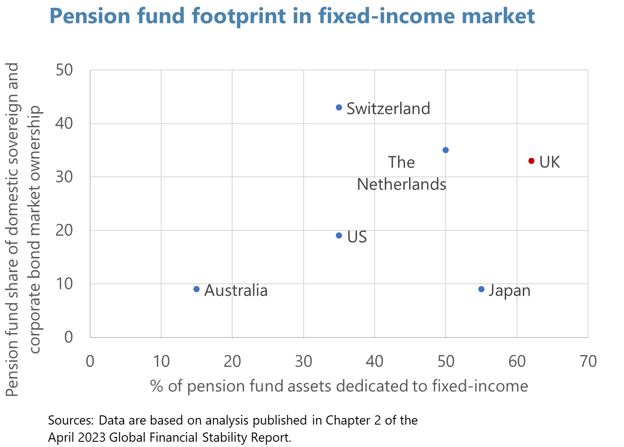

The quick and sharp increase in gilt yields saw the net asset value of LDI funds fall significantly and forced funds to raise cash quickly to post additional collateral on secured borrowing and to meet higher margin calls. The use of leverage under the LDI strategy, through repurchase agreements and derivatives such as interest rate swaps, allows defined benefit pension (DB) funds to obtain a higher exposure to long-term gilts and to hedge the interest rate and inflation risk in their liabilities, while also freeing up resources to invest in higher-yielding risk/growth assets. While higher yields improve pension funds’ solvency ratios, they also meant losses for the LDI funds, which had to either rebalance their portfolios, for example by asking their pension fund investors for more capital, or had to deleverage. Pension funds generally have several days or weeks to raise cash to top-up their collateral in their LDI positions. However, the sudden and unprecedented move in gilt yields after the “mini-budget” required pension funds to raise a significant amount of cash before the opening of each business day. While segregated LDI account managers had ready access to additional assets and cash, pooled LDI funds with a large number of small DB pension fund investors faced operational challenges in mobilizing extra liquidity. Market liquidity – measured by bid-ask spreads – deteriorated rapidly, and without cash to meet the margin and collateral calls, pooled LDI funds attempted to sell gilts, to raise liquidity and deleverage, contributing to the fire-sale dynamics.

The concentrated nature of LDI strategies and large exposures in the gilt market meant that this forced selling behavior represented a sudden and profound shift in supply-demand dynamics in the gilt market. Large quantities of gilt sales, particularly in long-dated and inflation-linked varieties, in an increasingly illiquid market pushed yields even higher, and further increased the required collateral payments. Other assets, including money market funds (MMFs) and investments in open-ended funds, were also liquidated. While MMFs were able to meet redemptions, some real estate funds had to suspend redemptions. Disorderly conditions became evident in the gilt markets, with an increasing risk of spreading to other market segments.

The market turmoil also spilled over to the real economy, with swap rates spiking and several mortgage providers discontinuing mortgage offerings temporarily as it became difficult to price markets. Amid higher gilt yields, interest rate swaps increased—the 2-yr interest rate swap typically used to price mortgage products reaching 6% in the aftermath of the mini-budget. While rates have stabilized since then, they remain at higher levels than prior to the crisis.

With imminent and growing financial stability risk, the BoE announced a temporary and targeted purchase of long-term gilts on September 28. The intervention constituted an emergency action of the BoE to stabilize markets and was supported by close coordination among key stakeholders, including overseas regulators. To restore orderly market conditions, the BoE announced that it would buy up to £5 billion in 20-year or longer-term gilts daily over 13 business days, ending October 14 (implying a maximum of £65 billion in total).1 With the daily turnover in the long-term gilt market of around £12 billion, this appeared to provide a sufficient liquidity backstop. The market calmed immediately, with the 30-year gilt yield dropping more than 100 bps on the first day of the intervention (although yields rose again in the days that followed with markets’ concerns regarding fiscal policy had yet been addressed). Still, approaching the end of the intervention period, markets became increasingly anxious about the October 14 expiration “cliff edge.” Given the possibility of heightened gilt-selling pressure during the last week of its emergency operation, the BoE expanded its financial stability measures on October 10 and 11. The BoE announced also announced a Temporary Expanded Collateral Repo Facility (TECRF) for banks through November 10 with expanded collateral, however ultimately this facility saw a small take-up.

The reversal of key “mini-budget” measures that was announced by the fiscal authorities also proved beneficial to calm the market. Although the start of the BoE intervention on September 28 did calm down the market, with yields dropping sharply, gilt yields resumed an upward trend between September 30 and October 12. It was in this context that the then-PM Truss dropped her plan of removing the planned corporate tax rise and appointed Jeremy Hunt as the new chancellor (October 14). The following Monday (October 17), the new chancellor scrapped most of the remaining tax cuts in the “mini-budget,” and markets staged a major (and sustained) rally in response to what they perceived as a renewed commitment to fiscal discipline.

The BoE’s financial stability intervention, together with the aforementioned fiscal policy reversals, successfully restored orderly market conditions in the aftermath of the “mini-budget” and enabled the LDI funds to build their resilience. The intervention was indeed temporary and targeted. Its operation lasted for 13 days and bought a total of £19.3 billion in long-dated gilts. In total, DB pension schemes and LDI funds sold an estimated £37 billion in gilts over this period; this is smaller than the estimated total margin and collateral calls these entities faced over this period (roughly £70 billion), reflecting the fact that LDI funds and pension schemes were also able to sell assets other than gilts (such as equities or corporate bonds) and use existing cash buffers in order to meet these obligations as well. Market intelligence suggests LDI funds also raised tens of billions worth of pounds in capital from end-investors, which also reduced their leverage. The BoE successfully unwound all its financial stability gilt purchases by January 12, 2023, just three months after the end of its stability intervention.

The LDI stress episode was not completely idiosyncratic, echoing NBFI vulnerabilities in past stress episodes—including liquidity stress, leverage, and interconnectedness. The leveraged positions taken on by funds, liquidity shortages that they faced as a result of margin calls, and the impact that their selling of gilts had on the broader market demonstrated how quickly financial stress can amplify and spread. The ‘Dash for Cash’ in March 2020 and Archegos stress event in March 2021 are also examples where leverage, a liquidity shortage, and interconnectedness generated financial stability risks, particularly where markets were intermediated by dealers. Therefore, our takeaways focus on the key lessons for mitigating and managing NBFI vulnerabilities more broadly.

Strengthening NBFIs’ liquidity management is a key part of reducing NBFI vulnerabilities. This includes enhancing liquidity regulation of NBFIs holding leveraged exposures in core markets, in order to reduce risks of future disruption as well as the need for central bank backstops. Recent events demonstrated that stress tests were too mild and that mandated liquidity buffers for NBFIs should be reevaluated and strengthened if required. In terms of measures taken by LDI funds in the immediate aftermath of the crisis, funds have been strengthened considerably and secured an average yield buffer (“headroom”) of around 300-400 bps. In addition, the UK authorities have recommended stronger safeguards (a minimum liquidity requirement for pension funds investing in LDI strategies to withstand a 250 bps move in long-dated gilt yields as part of a steady-state level of resilience, see BoE 2023a) and operational resilience to both pension funds and LDI managers. Moreover, ongoing work on liquidity mismatches in investment funds is important – with money market and open-ended fund regulation to be enhanced in line with recent Financial Stability Board proposals. For MMFs, policy proposals include measures to reduce liquidity transformation (i.e., hold a higher share of liquid assets) or move the cost of redeeming to those investors that redeem (i.e., swing pricing for example). Moreover, there is a need to ensure that open-ended funds use adequate liquidity management tools.

Ex-ante liquidity facilities for NBFIs, such as contingent liquidity lines with banks, could be pre-negotiated. The repo window that the BoE set up, which would have involved banks, only saw a small take-up. This reveals that banks are unlikely to play the role of providing liquidity to NBFIs during a crisis, partly as a result of the more stringent regulations that they have been subject to since the GFC. Therefore, ex-ante liquidity facilities for the NBFIs with banks could be helpful to be negotiated, for example, contingency liquidity lines. There is precedent for this in Denmark.

Informational gaps around NBFI activities and exposures, and lack of systemic oversight have been common threads in all recent crises involving NBFIs. For example, following the Archegos episode, concerns were raised about banks’ risk management, margin requirements for over-the-counter (OTC) derivatives, the opacity of family offices, and the ability of regulators to monitor system-wide risks. Relatedly, the Basel Committee on Banking Supervision (BCBS) highlighted vulnerabilities and deficiencies in the risk management of banks related to NBFIs, including insufficient information collection on clients’ positions and exposures, together with limited efforts to understand and assess clients’ investing strategies.

Visibility of some parts of the NBFI sector has improved in recent years, but the LDI episode showed that UK regulators still have limited visibility and regulatory oversight of pooled and single client funds where leverage and liquidity data are not readily available. The UK’s Financial Sector Assessment Program (FSAP, IMF 2022) recommended the UK authorities collect or systematize the collection and reporting of data for all Sterling holdings by all investors. Such data could help to enhance the analysis of the concentration of NBFI investors in key sterling markets, including holders of various gilt maturities with similar business models and their behavior in stress together with resulting implications for liquidity in these markets. These data would also be critical for proper NBFI supervision and designing appropriate backstop facilities. In addition to margin calls, for insurers – liquidity risks could stem from higher outflows as a result of policy surrenders (i.e., cancellation of policies) or catastrophe events, and also from lower premiums. To analyze combined liquidity drains, more granular data and a monitoring framework is needed. For a comprehensive analysis of liquidity risks, insurance supervisors should enhance its supervisory reporting and monitor cash pooling arrangements within insurance groups. Moreover, intermediaries such as prime brokers should have access to data on a fund’s overall leverage, not just the portion to which they have contributed.

All data collection efforts need continued international coordination, but the UK authorities should continue to take the lead in this area. The UK NBFI sector is internationally connected thus information collection and supervision would require international cooperation. In this respect, the UK authorities should continue strengthening information sharing with relevant third-country authorities, including monitoring and supervising internationally active NBFIs. However, closing these data gaps would support a holistic overview of NBFI vulnerabilities, but in itself would likely be insufficient to assess and respond to financial stability risks.

Moreover, continued horizon scanning is a critical for identifying and assessing NBFI vulnerabilities and also to improve systemic oversight. The NBFI sector comprises a set of diverse institutions with different business plans and levels of risk taking and is continuously evolving and adapting. Hence, continued monitoring and improvement in assessments are required. The LDI crisis was triggered by a fiscal event resulting in historical moves in gilt yields, exceeding any standard stress test parameters. This illustrates the importance of macroeconomic policy coordination, but it also challenges the assurance from standard stress tests. In this context, reverse stress testing with a purpose of reverse stress testing is to identify extreme events or circumstances that could potentially cause significant financial stability risks can be used as a complementary tool. By identifying these scenarios, the authorities and financial institutions can develop contingency plans and risk mitigation strategies to ensure resilience.

The design of BoE’s financial stability intervention greatly benefited from timely information provided by market intelligence which helped to tailor the BoE’s response to LDI stress. For example, once stress emerged, market intelligence confirmed that leverage was already high and that a swift intervention from the BoE was needed, thus after consideration a repo facility for LDI funds was ruled out and targeted gilt purchases were seen as the best option.

While the BoE’s intervention also involved gilt purchases, the implementation was quite different during the dash for cash episode where monetary policy was expected to loosen. Typically, central bank asset purchases contribute towards monetary easing, and accompanies situations where central banks are lowering interest rates. In the case of the LDI stress event, the BoE had already set out its plans for quantitative tightening – first by stopping reinvestments from March 2022 and then also announced plans for active gilt sales i.e., selling gilts, against a backdrop of interest rate hikes to tame inflation. When the BoE intervened, it paused the planned start of active gilt sales. Moreover, backstop pricing meant that, unlike in QE, the BoE did not set out to buy a given quantity of gilts in each auction. Rather, the Bank set a backstop price relative to the market for each gilt, above which it would not purchase. This ensured the intervention remained a backstop to market functioning, with the Bank purchasing only as much as required by the market to restore orderly functioning.

Still, given the potential perceived tensions between price stability and financial stability, transparency and clear communication are critical for conducting effective market interventions during stress episodes. Policies such as opening central bank liquidity support to NBFIs may make achieving price stability complicated if it involves asset purchases, while raising moral hazard concerns. For example, purchasing sovereign bonds to improve market functionality while raising policy rates and conducting quantitative tightening could create communication challenges. In such a scenario, clear communication by the central bank becomes even more important, especially if such measures are prolonged and untargeted (see GFSR April 2023). In this context, BoE’s firm communication with markets on the temporary and targeted nature of the intervention and with pension funds on the need to recapitalize their funds swiftly was proven critical, despite some market participants initially perceiving tensions.

At the same time, backstops for the functioning of core markets such as sovereign debt markets should be strengthened, whilst minimizing moral hazard. For entities for which data are collected and analyzed, and which are subject to appropriate supervision and systemically interconnected, consideration could be given to grant access to a central bank liquidity backstop. In the context of the UK, the inclusion of certain NBFIs in the BoE’s operational framework could improve the BoE’s options in future stress situations – for example allowing appropriately regulated and systemically interconnected NBFIs possible access to some liquidity support from the BoE’s facilities would widen the range of options available to counteract future market-wide stresses. The UK FSAP stressed that such support should be focused on maintaining the functioning of the core markets (such as gilts and gilt repos). Expanding the toolkit would be especially important as the BoE is currently in a monetary tightening phase. The design of facilities accessible to NBFIs should reflect their diverse nature and safeguards would need to be in place with risk remaining in the marketplace to avoid moral hazard.2

European Systemic Risk Board (2023), “EU Non-bank Financial Intermediation Risk Monitor 2023”, June 2023.

Central Bank of Ireland (2022), Industry Letter – Liability Driven Investments Funds. Industry letter, November 2022.

Ruo Chen and Esti Kemp, “Putting Out the NBFire: Lessons from the UK’s Liability-Driven Investment (LDI) Crisis,” IMF Working Papers 2023/210 (Washington: International Monetary Fund).

Financial Conduct Authority (2023), “Further guidance on enhancing resilience in Liability Driven Investment,” April 24, 2023.

Hauser, Andrew (2022), “Thirteen days in October: how central bank balance sheets can support monetary and financial stability,” Speech given at ECB’s 2022 Conference on Money Markets, November 4, 2022.

International Monetary Fund (2022), “United Kingdom: Financial Sector Assessment Program-Financial System Stability Assessment”, International Monetary Fund, Country Report No. 2022/057.

International Monetary Fund (2023a), “Global Financial Stability Report: Safeguarding Financial Stability Amid High Inflation and Geopolitical Risks”, International Monetary Fund, Global Financial Stability Report April 2023.

Pinter, Gabor (2023), “An Anatomy of the 2022 Gilt Market Crisis,” Bank of England, Staff Working Paper No. 1019, 2023.

The Pension Regulator (2023), “Using leveraged liability-driven investment,” April 24, 2023.

For more information on the BoE intervention, see Hauser (2022).

See also IMF, 2023a for further guidelines for central bank intervention to provide liquidity.