Regulatory authorities faced with a bank whose underlying solvency is uncertain must make a series of decisions, including how and when to intervene. In a recent paper, we analyse the optimal timing of policy interventions in troubled banks and show that it may sometimes be optimal to delay intervention. The reason is that delaying intervention increases the chance that information arrives that reveals the bank’s true solvency state. At the same time, delaying intervention gives uninsured creditors the opportunity to withdraw, which raises the cost of bailing out insured depositors if the bank is ultimately resolved. The optimal timing of resolution trades off these costs with the option value of making a more efficient resolution decision following the arrival of information.

A key challenge for regulatory authorities is judging whether a bank facing liquidity problems is fundamentally insolvent (a gone concern), or whether it is just illiquid and could avoid insolvency if given adequate policy support (a going concern). While resolution policies differ in their details across jurisdictions, a common feature is that regulatory authorities enjoy considerable flexibility in determining whether a financial institution has reached a point of non-viability (PONV) and should be resolved (EBA, 2015; FDIC, 2019). This flexibility raises an important question: what determines the optimal timing of regulatory authorities’ intervention decision?

In our paper, “The Optimal Timing of Policy Interventions in Troubled Banks” (König et al., 2022), we provide an answer to this question. We show that the optimal timing of resolution trades off the value of delaying intervention in order to obtain additional information about a troubled bank’s true solvency state, with the costs from bailing out insured depositors if the bank is ultimately resolved. We also analyse how the optimal timing of resolution is affected by other commonly used policy tools, including emergency liquidity support and public equity injections.

Our model considers a bank with a long-term asset financed by a mix of uninsured debt, insured deposits and equity. The long-term asset (e.g., a loan portfolio) is illiquid, in the sense that liquidating the asset before maturity creates a dead-weight loss. At some date, a “rumour” breaks out that the bank’s asset may have become impaired by a shock.2 This rumour raises doubts about the bank’s ability to repay its debt in full and prompts uninsured creditors to start withdrawing their funds, which forces the bank to engage in costly asset sales. Furthermore, by draining resources from the bank, uninsured debt withdrawals circumvent the de jure seniority of insured depositors in resolution. Because the policy authority has to make insured depositors whole in case the bank is resolved, the uninsured debt withdrawals create dilution costs for the policy authority.

Resolving the bank immediately after the rumour breaks out stops uninsured creditors from withdrawing and minimizes the dilution costs incurred by the policy authority. However, if the rumour is false and the bank’s asset is in fact unimpaired, then resolution creates an efficiency loss due to the dead-weight loss from liquidating the asset. Delaying resolution gives the policy authority time to collect additional information about the bank’s true solvency state and therefore reduces the risk of mistakenly resolving a solvent bank. The optimal resolutiondate — i.e., the optimal determination of the bank’s PONV — trades-off the value from avoiding the resolution of a fundamentally solvent bank with the dilution costs from allowing uninsured creditors to continue withdrawing.

In practice, policy authorities can deploy additional instruments including emergency liquidity support or equity injections before resolution measures are invoked. In our model, providing liquidity support does not eliminate the uncertainty about the bank’s solvency state and does not stop uninsured debt withdrawals. However, liquidity support allows the bank to meet funding withdrawals without engaging in costly asset sales. Liquidity support therefore avoids debt withdrawals from depleting the bank’s equity and prevents the bank from defaulting due to illiquidity. The provision of liquidity support comes at the cost of exposing the policy authority to counter-party risk, which increases the losses borne by the policy authority if the bank turns out to be fundamentally insolvent.

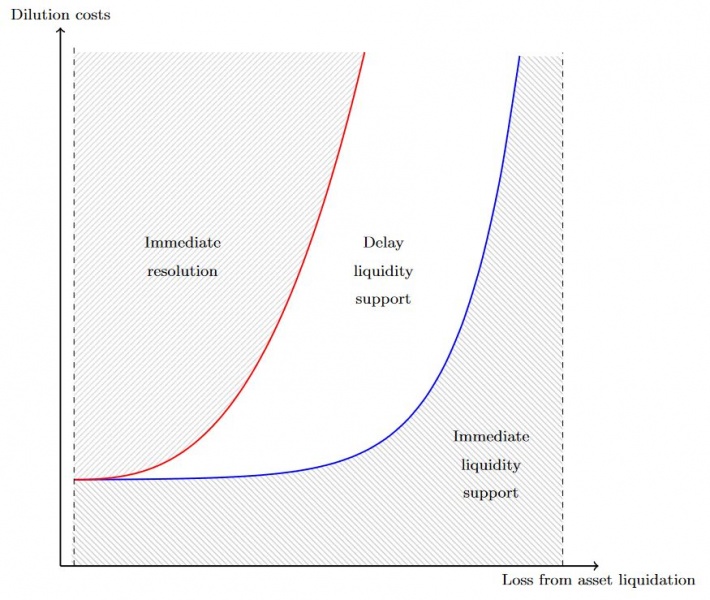

Figure 1 shows the policy authority’s optimal intervention decision in terms of the dilution costs (y-axis) and the dead-weight loss from asset liquidation (x-axis). For combinations of these costs above the red curve, the authority resolves the bank immediately when the rumour starts. Here, the dilution costs are large relative to the loss from asset liquidation, implying that waiting or supporting the bank is less attractive, compared to immediate resolution. In contrast, below the blue curve, the authority immediately provides liquidity support once the rumour starts. Here, liquidation losses are large compared to the dilution costs, which leads the authority to choose to prevent costly asset sales notwithstanding the risk of incurring higher losses from providing liquidity support. In the intermediate region, the authority optimally delays the provision of liquidity support. The reason is that delaying liquidity support reduces the authority’s losses should the bank turn out to be insolvent and at the same time eliminates the risk of inefficiently resolving a fundamentally solvent bank.

Figure 1: Immediate support may not always be optimal

The key benefit of liquidity support is that it avoids the inefficient liquidation of the bank’s assets. An alternative policy that avoids costly asset sales is to directly inject equity into the bank in order to increase the bank’s pledgeable income and to incentivize uninsured creditors to roll over their claims.

We show that although the policy authority may sometimes delay liquidity support, it is never optimal to delay equity injections: i.e., if equity injections are the preferred policy tool, then equity is always injected immediately once the rumour starts. The reason is that the minimum equity injection needed in order for the bank to be able to roll over its uninsured debt increases if intervention is delayed. We also show that equity injections are preferred to immediate liquidity support whenever the average maturity of uninsured debt is relatively short or the bank is financed with relatively few insured deposits. A short average debt maturity structure implies that a large fraction of uninsured creditors are able to withdraw before additional information about the bank’s solvency arrives, which increases the authority’s counter-party risk exposure from providing liquidity support. A small insured deposit base, in contrast, reduces the minimum equity injection needed in order for the bank to be able to roll over its uninsured debt.

An effective and efficient bank resolution framework is an indispensable element of a modern regulatory and supervisory architecture. Recent reforms have improved the harmonization of rules to increase the speed of resolution activities in the European Union (EU, 2014), or were aimed at developing common principles to foster a coordinated resolution of multinational banks (FSB, 2014). Ongoing reforms of the crisis management and deposit insurance framework in the European Union seek to further improve existing bank resolution directives. However, despite strong interest from policy institutions in such questions, surprisingly little has been written about the optimal timing of resolution and the determinants of the optimal PONV.

Our paper provides a first attempt at understanding the trade-offs faced by policymakers having to decide whether and when to resolve a troubled bank whose underlying solvency is uncertain. The optimal timing of intervention in our model can be framed in terms of weighing the benefits of avoiding a type-I error (preventing the inefficient resolution of a solvent bank) and the costs of making a type-II error (keeping an insolvent bank afloat). Our results show that delaying intervention may sometimes be optimal. As such, they offer a rationale for the empirically documented lag between the appearance of the first signs of trouble at a bank and its eventual resolution, as could be observed, for example, in the case of the resolution of Indy Mac in 2008 or in the more recent case of Banco Popular in 2017. Our model also shows how the optimal determination of a bank’s PONV depends on a bank’s balance sheet characteristics (e.g., insured deposit base, debt maturity structure) and the broader macroeconomic and institutional environment (e.g., market liquidity condition, supervisory systems). Taken together, our findings provide support for the flexibility enjoyed by policymakers when dealing with troubled banks.

EBA. 2015. Guidelines on the interpretation of the different circumstances when an institution shall be considered as failing or likely to fail under Article 32(6) of Directive 2014/59/EU. EBA/GL/2015/07. URL: EBA-GL-2015-07 GL on failing or likely to fail.pdf (europa.eu)

EU. 2014. DIRECTIVE 2014/59/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL. Official Journal of the European Union. L 173 / 190. URL: DUMMY (europa.eu)

FDIC. 2019. Resolutions Handbook. URL: Resolutions Handbook (fdic.gov)

FSB. 2019. Key Attributes of Effective Resolution Regimes for Financial Institutions. URL: Key Attributes of Effective Resolution Regimes for Financial Institutions – Financial Stability Board (fsb.org)

König, P. J., P. Mayer, D. Pothier. 2022. Optimal Timing of Policy Interventions in Troubled Banks. Discussion Paper 10/2022. Deutsche Bundesbank. URL: Optimal timing of policy interventions in troubled banks (bundesbank.de)

Santos, J., Suarez, J. (2019). Liquidity standards and the value of an informed lender

of last resort. Journal of Financial Economics, 132(2), 351 – 368. URL: Liquidity standards and the value of an informed lender of last resort – ScienceDirect.

Disclaimer: The views in this article are those of the authors and do not necessarily represent the views of the Deutsche Bundesbank or the Eurosystem.

Our model builds on Santos and Suarez (2020). However, they abstract from insured deposits, costly bail-outs of insured deposits and asset liquidations. Moreover, their paper focuses on the related but different issue of the relationship between liquidity requirements and lender-of-last-resort actions.