The material presented here is based on a recent IMF blog, How a Russian Natural Gas Cutoff Could Weigh on Europe’s Economies, July 19, 2022 (IMF, 2022a).

A full Russian gas shut-off would nevertheless be unprecedented. Three key questions arise: the degree of country vulnerability to outright shortages (in addition to still higher prices); the economic impact; and how to manage and minimize the impacts (there is no established blueprint, though policymakers are moving swiftly).

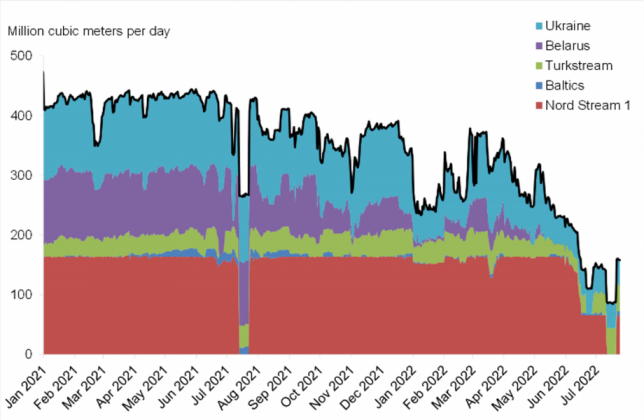

Chart 1: Russian Pipeline Gas Supplies to EU by Route

Sources: European Network of Transmission System Operators for Gas: Gas Transmission System Operator of Ukraine; staff calculations. Note: Last data point is 7/24. Recent data are provisional.

Gas has provided a growing share of European energy in recent years, along with renewables, while the use of coal and oil has declined. Power generation is the largest user, followed by homes and industry.

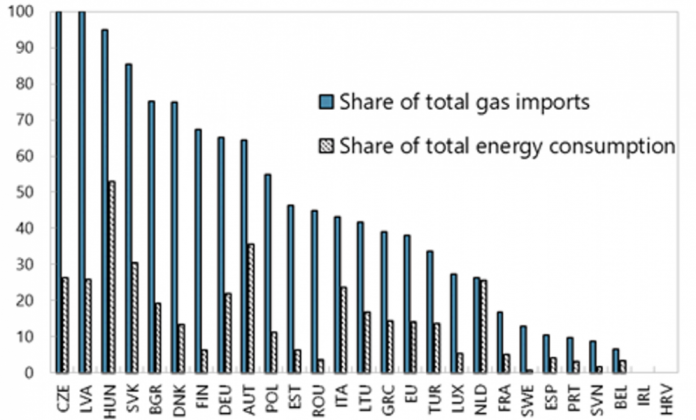

Dependence on Russia for gas and other energy sources varies widely by nation (Chart 2). As of 2020, some economies strongly relied on Russian gas imports for their energy needs, like the Czech Republic and Hungary, while some countries didn’t rely at all on Russian supplies of the fuel.

Chart 2: Russian Gas Dependance, 2020 (percent)

Sources: Eurostat, Gazprom and staff calculations. Note: Some countries may re-export Russian gas, which could affect Russia‘s share in total imports and energy consumption.

The major gas arteries from Russia enter through Germany, Poland, Ukraine and Turkey, accounting for 42 percent of gas import capacity. Other pipelines from Norway, the United Kingdom, Northern Africa, and the Caspian region account for 30 percent. Liquefied natural gas (LNG), most of which arrives by ship, accounts for the remainder of import capacity, with the largest share arriving at terminals in Spain, France, and Italy.

Within this infrastructure, pipelines are historically not used at full capacity, e.g., in 2021 only 61% of capacity was used. And while LNG imports have substantially increased in recent months, only 66 percent of daily LNG import capacity is being used on average.

However, technical constraints in transmission within Europe create potential bottlenecks that could fragment the European gas market. Spain, for example, is the EU’s largest LNG importer, with more than a third of total capacity, but it can send only a tenth of what it imports on to neighboring France. North-south constraints exist in France, Italy, and Germany. And pipelines designed to flow east to west leave other countries, especially in Central Europe, effectively disconnected from Europe’s spare capacity.

Gas storage is meant to smooth temporary market disruptions or spikes in demand during winter. But it is not enough to compensate for a full Russian gas shut-off. And the recent reduction in Russian gas flows and spike in prices may prevent sufficient storage accumulation during the summer season (when gas usage is lower). As of late June, EU gas storage was at 55 percent of capacity, a relatively low level but still higher than 2018 and 2021 around the same time.

More reliance on the global LNG market will be necessary but is not without complications. With limited global capacity to export LNG from the US, Qatar, and other places, prices need to rise to attract cargoes from other destinations (largely in Asia, where adjustment to the shock then partially spills over to). Scaling up import and export infrastructure takes time and is capital intensive. It generally requires customers in Europe to sign longer-term contracts with LNG exporters, which some have been reluctant to do given the uncertainty about how they would square with the green energy transition.

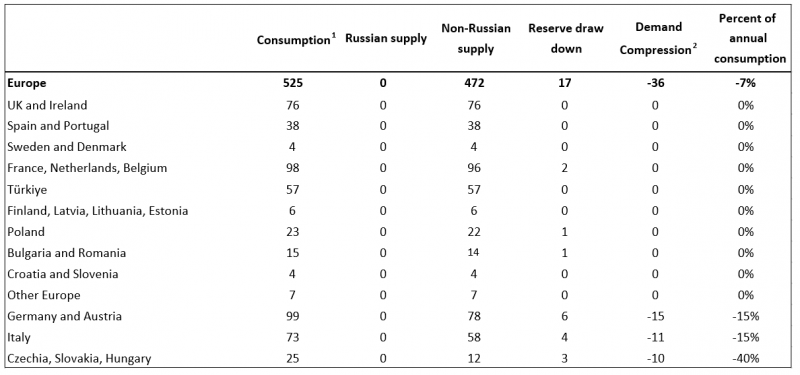

To date, European infrastructure and global supply have been able to cope with the 60 percent drop in Russian gas deliveries, as gas consumption declined by 9 percent in the first quarter of 2022 relative to the previous year and alternative supplies are being tapped. This is in line with our assessment that a reduction of around 70 percent of Russian gas could be managed in the short-term and explains why some countries have been able to unilaterally halt Russian imports. In a generalized shut-off, diversification would be much more difficult, with the possibility of re-routing gas within Europe reduced (as bottlenecks could show up) and substituting gas for alternative fuels made more difficult by high demand for these. Several countries would be at considerable risks of shortages (Table 1).

Table 1: Gas Flows in Adverse Scenario (BCM)

1 Includes some demand compression based on the higher gas prices witnessed to date

2 Required reduction in demand in order to meet available supply. This could be achieved through market-based price adjustment and/or government rationing.

Note: The columns of the table should be read in the same way as the gas flow charts above. For Italy, for example, consumption without a gas shut-off would be around 73bcm over the next 12-months. Alternative non-Russian gas supplies are around 58bcm. This could be supplemented with an additional 4bcm draw-down of reserves, net over the year (draw-down may be higher at peak demand). This leaves a potential shortfall of 11bcm, representing 15 percent of annual consumption.

As a total Russian gas shut-off would be an unprecedented event, the right modeling assumptions are highly uncertain and vary between countries. The shut-off would likely interact with countries’ intensity of Russian gas use in energy consumption, delayed demand reductions (due to delayed price pass through) and physical constraints in the importation, storage, and distribution of gas. This could cause very high prices, and possibly physical gas shortages in some countries (reflecting market fragmentation and price divergence).

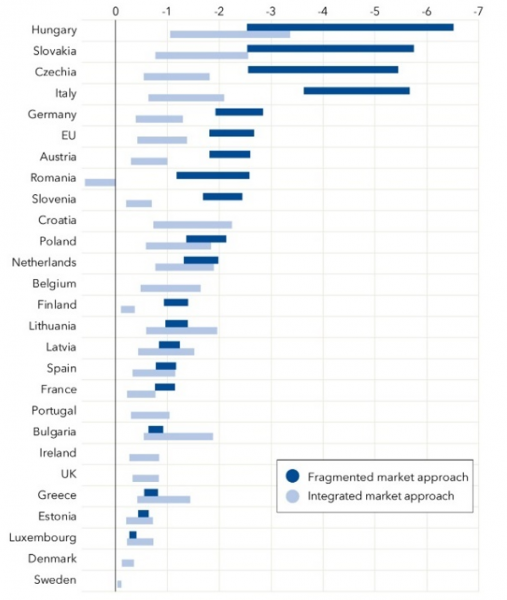

We gauge impacts in two ways. One is an integrated-market approach that assumes gas can get where it is needed, and prices adjust to clear markets.1 Another is a fragmented-market approach that is best used when the gas cannot go where needed no matter how much prices rise.2 Both approaches capture supply side effects, while only the second approach takes into account some aggregate demand impacts. Both abstract from full impacts (notably that could come through confidence channels).

A full shut-off would likely impact economic activity in the EU significantly. Here, in order to simplify the estimation and make it comparable with the results in the literature to date, we focus on the impact relative to a counterfactual with no reduced gas supply in 2022. In addition, also for simplicity, the simulations assume that the shut-off starts at end-June.

If EU gas market remains integrated both internally and with the rest of the world, our integrated-market approach suggests that the global LNG market would help buffer economic impacts. That is because reduced consumption is distributed across all countries connected to the global market. The estimated economic impact is thus at the lower end of the light blue interval of chart 3. At the extreme, in complete absence of LNG support, the impact of the shock is noticeably magnified as soaring gas prices would have to work by depressing consumption only in the EU, leading to substantial aggregate output losses (upper end of the light blue interval in the chart).

Chart 3: Output losses—A Russian gas supply shut-off has varying impacts across Europe (percent of GDP)

Source: IMF staff estimates

If physical constraints are binding, fragmenting the gas market in Europe, the output impact would be especially significant for some countries in Central and Eastern Europe, notably the Czech Republic, Hungary, and Slovakia, where the intensity of Russian gas use is high and alternatives supply sources are scarce. They could face lower GDP growth of as much as 6 percentage points relative to the pre-shock baseline (dark blue intervals in chart 3). Italy would also face significant impacts due to its high reliance on gas in electricity production. The effects on Austria and Germany would be lower but could still be significant, depending on the availability of alternative sources of gas and the ability to lower household gas consumption.3 For many other countries with sufficient access to international LNG markets the impact on GDP would be moderate – possibly below one percentage point. These economic impacts would be larger to the extent strong demand and confidence channels operate.

Germany, the world’s fourth-largest economy, is among the countries significantly exposed to the risk of Russia fully cutting off its gas exports. Gas accounts for a quarter of German energy use, and nearly all of it is imported. Germany has pipeline connections to Norway and can access LNG terminals in neighboring countries, like Belgium and the Netherlands. But spare capacity through both sources is limited.

Germany is taking steps to further integrate with global gas markets. The government has announced that four new floating LNG terminals will gradually be established by 2024. Germany will also reduce gas use in electricity generation in favor of coal. However, even with these measures, and assuming that re-exports of gas can be curtailed in line with the June curtailment in Nord Stream 1 flows to Germany, we find that Germany can only narrowly avoid shortages of gas in the next two winters. Furthermore, reserves drop to low levels, leaving the country vulnerable to a stoppage of the remaining supplies of Russian gas. If these were to stop, our research suggests that gas consumption might need to be cut by a further 10-20 percent in the next two winters.

To understand the macroeconomic outlook for Germany in the event of a full shut off, and to further consider policy options, we dug deeper. Starting with the baseline outlook in our Article IV Consultation—which already embeds the partial shut-off seen to-date—we extended the time period of the assessment through 2027, and incorporated additional demand side impacts operating through uncertainty channels. Our estimates suggest that uncertainty channels would notably add to the economic impacts from a full shut-off and that impacts would peak in 2023, and tail off thereafter as alternative sources of gas came online. The rise in wholesale gas prices could also increase inflation significantly in 2022 and 2023. Simulations illustrate that voluntary gas-saving by households could limit the GDP loss significantly, as could a well-designed gas rationing scheme, which for example lets downstream and gas intensive industry bear more of the gas shortages. However, rationing decisions go beyond economics as they must reflect social, legal, and technical considerations too.

The EU and national responses have been swift, and many countries have already started to source alternative supplies, replace gas with other fuels where possible, and update contingency plans. They should continue to alleviate infrastructure bottlenecks and other market-integration constraints (such as reversing flows from Western to Eastern Europe or expanding floating LNG terminals that can serve Central Europe) to allow markets to continue to function. Bilateral solidarity agreements – which stipulate the details of burden sharing among neighboring countries –are also crucial crisis preparation tools.

Incentivizing lower natural gas demand is key to help mitigate the impact of a full gas shut-off. When and how this is done matters. Part of the answer is greater energy efficiency. Efforts such as better insulating buildings and proper maintenance on household natural gas equipment help over the medium term and should be further accelerated. But part of the short-term answer also relies on consumers adjusting their behavior to save energy. Earlier action can help create more room to build storage before the heavy winter usage season. And bringing households into the equation can reduce the potential need to significantly curtail firms’ production in the face of shortages (which would then spread through Europe’s tightly integrated supply chains to neighboring countries).

We see a lot of progress in this area to date. Individual countries have launched campaigns to encourage household and government energy savings during the heating season (e.g., Germany and Italy, with its campaign to reduce indoor temperature settings). The approval by the European Council of a plan for countries to voluntarily reduce gas demand by 15 percent during the 2022-23 winter is a potentially important initiative and a sign of European solidarity, which will be needed. The REPowerEU strategy also emphasizes demand savings, with an important role for maintaining price signals to allow for endogenous demand adjustment.

There does, however, remain a gap between ambition and reality to date in this dimension. Forthcoming work by IMF economists (Celasun et al, 2022) shows that many countries have chosen policies which strongly limit the pass-through of wholesale prices to consumers. A better alternative would be to allow greater passthrough to incentivize demand adjustment, and then compensate vulnerable households in a targeted way. We also see scope for further public campaigns to clearly communicate the challenges of the moment across Europe, with the aim of maintaining a high level of solidarity between and within countries.

Our research shows that the economic fallout from a Russian gas shutoff can be partially mitigated. Beyond measures already taken, further action should focus on risk mitigation and crisis preparedness. Governments must boost efforts to secure supplies from global LNG markets and alternative sources, continue to alleviate infrastructure bottlenecks to import and distribute gas, plan to share supplies in an emergency across the EU, act decisively to encourage energy savings while protecting vulnerable households, and prepare smart gas rationing programs. This is a moment for Europe to build upon the decisive action and solidarity displayed during the pandemic to address the challenging moment it faces today.

Albrizio, Silvia, John Bluedorn, Christoffer Koch, Andrea Pescatori, and Martin Stuermer (2022), Market Size and Supply Disruptions: Sharing the Pain from a Potential Russian Gas Shut-off to the European Union, IMF Working Paper WP/22/143.

Celasun, Oya, Dora Iakova, Ian Parry, Anil Ari, Nicolas Arregui, Aiko Mineshima, and Iulia Teodoru, Simon Black, Victor Mylonas, and Karly Zhunussova (2022), Surging Energy Prices in Europe in the Aftermath of the War: How to Support the Vulnerable and Speed up the Transition away from Fossil Fuels, IMF Working Paper, WP/22/152.

Di Bella, Gabriel, Mark Flanagan, Karim Foda, Svitlana Maslova, Alex Pienkowski, Martin Stuermer, and Frederik Toscani (2022), Natural Gas in Europe: The Potential Impact of Disruptions to Supply, IMF Working Paper, WP/22/145.

IMF (2022a), How a Russian Natural Gas Cutoff Could Weigh on Europe’s Economies, https://blogs.imf.org/2022/07/19/how-a-russian-natural-gas-cutoff-could-weigh-on-europes-economies/.

IMF (2022b), Gloomy and More Uncertain, World Economic Outlook Update, July 2022.

Lan, Ting, Galen Sher and Jing Zhou (2022), The Economic Impacts on Germany of a Potential Russian Gas Shutoff, IMF Working Paper 2022/144.

See Albrizio et al (2022) for more details.

See Di Bella et al (2022) for more details.

For a more detailed analysis of the impact on Germany see Lan, Sher and Zhou (2022).