References

Adrian, Tobias and Nellie Liang, (2018). ‘Monetary Policy, Financial Conditions, and Financial Stability’, International Journal of Central Banking 14(1): 73-131.

Agur, Itai and Maria Demertzis, (2018). “Will Macroprudential policy Counteract the Monetary Policy Effects on Bank Behavior?” Bruegel Working Paper, No. 1.

Ben-Haim, Yakov and Maria Demertzis, (2008). Confidence in Monetary Policy, DNB Working Paper No. 192.

Blanchard, Olivier, Giovanni Dell’Ariccia and Paolo Mauro, (2010). Rethinking Macroeconomic Policy, IMF Staff Position Note, February 12, 03.

Borio, Claudio and William White, (2004). Whither monetary policy and financial stability? The implications of evolving policy regimes, BIS Working Paper No. 147.

Claeys, G., (2016). ‘The decline of long-term rates: bond bubble or secular stagnation symptom?’ Policy Contribution 2016/16, Bruegel

Clayes, Gregory, Maria Demertzis and Jan Mazza, (2018). “A Monetary Policy Framework for the European Central Bank to deal with Uncertainty”, European Parliament, In-Depth Analysis, Requested by the ECON Committee.

Dell’Ariccia, Giovanni, Luc Laeven, and Gustavo Suarez, (2017). “Bank leverage and monetary policy’s risk-taking channel: Evidence from the United States”, Journal of Finance 72(2), 613-654.

Demertzis, Maria and Nicola Viegi, (2008). “Inflation Targets as Focal Points”, International Journal of Central Banking, Vol. 4 No. 1, March, 55-8.

Demertzis, Maria and Nicola Viegi, (2010). “Inflation Targeting: a Framework for Communication”, B.E. Journal of Macroeconomics (Topics), Vol. 9, 1.

Gersl, Adam, Petr Jakubík, Dorota Kowalczyk, Steven Ongena, and José-Luis Peydró, (2015). Monetary conditions and banks´ behaviour in the Czech Republic, Open Economies Review 26(3), 407-445.

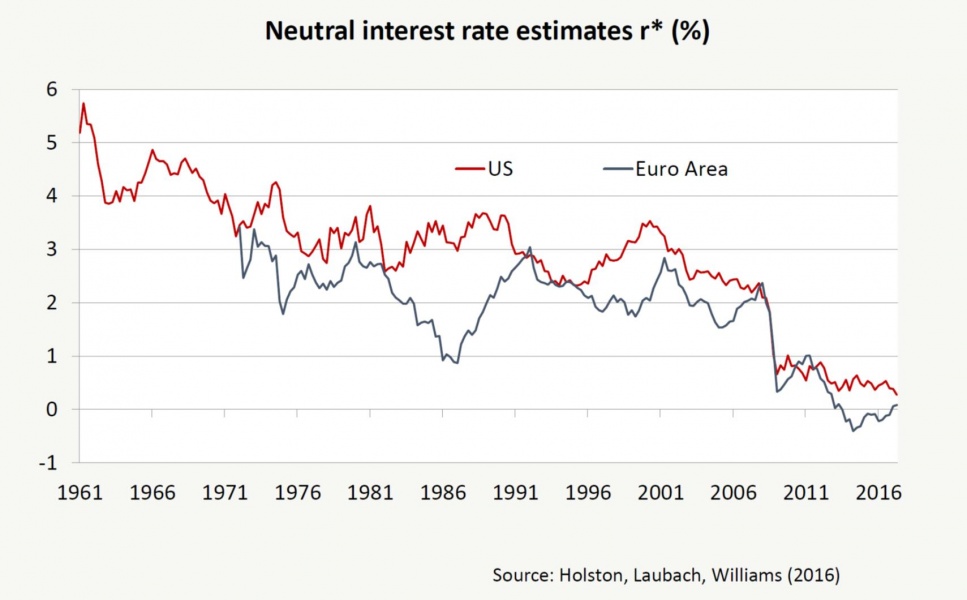

Holston, K., T. Laubach and John C. Williams, (2016). ‘Measuring the Natural Rate of Interest: International Trends and Determinants’, Working Paper Series 2016-11, Federal Reserve Bank of San Francisco.

Rajan, Raghuram G., (2006). Has finance made the world riskier? European Financial Management 12(4): 499-533.

Stein, Jeremy C., (2014). Incorporating financial stability considerations into a monetary policy framework, Speech at the Federal Reserve Board, Washington D.C., March 21, 2014.

Svensson, Lars E.O., (2014). “Inflation targeting and leaning against the wind“, International Journal of Central Banking 10(2), 103-114.