Disclaimer: The views expressed in this Policy Brief are solely those of the author, and do not necessarily reflect the views of the European Central Bank.

What are the consequences for price stability if the Treasury is limited in its willingness or ability to raise primary surpluses, and the central bank accommodates its interest-rate policy to the fiscal conditions? I address this question in a dynamic stochastic sticky-price model with endogenous shifts between an “orthodox” and a “fiscally-dominant” policy regime. The risk of future regime shifts has encompassing effects on equilibrium. Inflation is systematically higher than it would be if fiscal policy always adjusted its primary surplus sufficiently and monetary policy was solely concerned with price stability. This inflation bias is increasing in the real value of government debt. Regime-switching probabilities are not invariant to policy. The central bank can attenuate the risk of a shift to the fiscally-dominant regime by raising the real interest rate sufficiently moderately when inflation increases. Lower fiscal dominance risk, in turn, mitigates the inflation bias.

“Political pressures could arise and grow to keep interest rates lower than the rationale of price stability would call for.” (Weidmann, 2020)

“In near term, whether fiscal policy will have sufficient policy space to deliver on its various goals will depend on central banks’ reaction functions.” Draghi (2024)

Recent economic events have once again brought to the forefront the interdependence of monetary and fiscal policies. After a decade of low inflation and low interest rates, the global economy experienced a strong surge in inflation, and central banks embarked on a path of rising policy rates. The prospect of rising, and, subsequently, persistently higher interest rates, coupled with demands for governments to increase public spending, has sparked concerns about fiscal policy and the sustainability of elevated government debt levels. Historically, such economic conditions have often led to pressures on central banks to accommodate debt-management objectives and relegate price stability to the back seat (e.g., Humpage, 2016). What would be the consequences of such monetary-fiscal coordination? Can the goal of price stability occasionally take a back seat without jeopardizing price stability more generally? And, if not, what, if anything, can central banks do to preserve price stability without putting fiscal stability at risk.

In Schmidt (2024), I address these questions in a dynamic stochastic sticky-price model that gives rise to endogenous policy regime shifts. The public sector consists of a fiscal authority and a central bank. Fiscal policy is governed by a feedback rule for the primary surplus with an upper limit. When the real value of government debt is sufficiently low, an increase in the debt level begets an increase in the primary surplus and vice versa. Monetary policy focuses on its price stability goal and sets the policy rate according to a conventional Taylor rule. That is the “orthodox” policy regime. When government debt is high, the surplus limit binds. An increase in the debt level does not beget a rise in the primary surplus. The central bank, worried about the implications of high interest rates for fiscal stability, deviates from the conventional Taylor rule and—in the spirit of the concerns echoed by Weidmann—keeps the policy rate below some upper bound.1 That is when the economy is in the “fiscally-dominant” regime.2

In the model, the occasional subordination of the goal of price stability to the goal of fiscal stability results in a systematic failure to achieve the price stability goal. Under the considered monetary-fiscal configuration, inflation is generically higher than it would be if fiscal policy always adjusted its primary surplus sufficiently to variations in government debt and monetary policy was solely concerned with inflation stabilization. The size of the inflation bias increases with the real value of government debt.

Suppose that the primary surplus is below its limit—the economy is in the orthodox policy regime—when the economy is buffeted by an inflationary shock. The central bank raises the nominal interest rate aggressively so as to engineer an increase in the real interest rate (i.e. it abides by the so-called Taylor principle). Debt servicing costs increase, and in response the fiscal authority raises its primary surplus. When public debt is high to begin with and the inflationary shock is sufficiently large, the surplus limit becomes binding—the economy transitions to the fiscally-dominant regime.

In the fiscally-dominant regime, the monetary policy response to shocks is generically asymmetric. The central bank always lowers the nominal interest rate in response to deflationary shocks, but, because of the interest-rate upper bound, it increases the interest rate less aggressively, if at all, in response to sufficiently large inflationary shocks. Consequently, the real interest rate declines, both, when the economy is hit by a deflationary shock and when it is hit by a (sufficiently large) inflationary shock. A lower real interest rate relaxes the fiscal authority’s debt burden—the central bank helps to maintain fiscal stability. At the same time, the asymmetric monetary policy gives rise to an asymmetric inflation response. Inflation increases more in response to an inflationary shock than it declines in response to a deflationary shock of the same magnitude.

This asymmetric inflation profile gets baked into agents’ expectations. The mere possibility of a binding upper bound on the nominal interest rate in the fiscally-dominant regime shifts inflation expectations upwards in all states of the world, i.e. both in the fiscally-dominant regime and in the orthodox regime. Higher inflation expectations, in turn, put upward pressure on actual inflation. Under conventional parameterizations of the monetary policy rule, the central bank does not fully offset these inflationary pressures, giving rise to the aforementioned inflation bias.

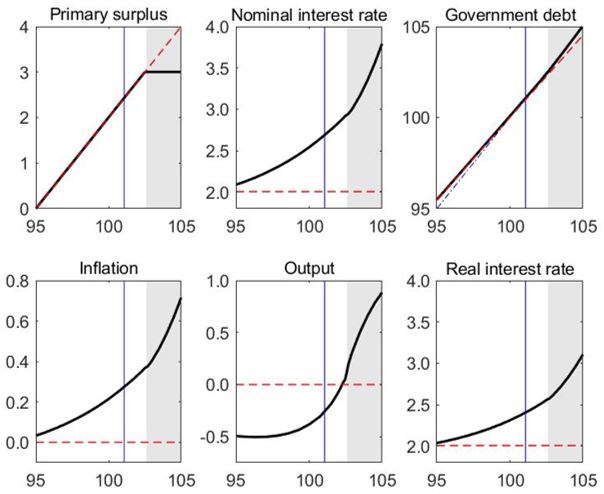

Figure 1: Equilibrium responses to government debt

Notes: Solid black lines (dashed red lines) show responses for the policy configuration with regime shifts (benchmark configuration). The surplus is expressed in percent of steady-state output. Interest rates and inflation are expressed in annualized percent. Government debt is expressed as percent of annualized steady-state output. Output is expressed in percentage deviations from steady state. The vertical solid blue lines indicate the risky steady state.

Figure 1 provides a numerical illustration.3 It shows the equilibrium responses of key model variables to the beginning-of-period government debt ratio (solid black lines). When public debt is sufficiently high the surplus limit binds and the economy is in the fiscally-dominant regime (gray-shaded area), and it is in the orthodox regime (non-shaded area) otherwise. In both policy regimes, and for all levels of government debt, the equilibrium response of inflation is strictly positive. The size of the inflation response is increasing in the debt level. This is very different from the response of inflation under a benchmark policy configuration where fiscal policy always adjusts its primary surplus sufficiently to variations in government debt (dashed red lines). In this case, the inflation rate is invariant to the government debt ratio, and price stability prevails. The difference between the two equilibrium responses provides a measure of the inflationary bias.

The link between inflation and government debt has features of a vicious cycle: A higher debt level, ceteris paribus, raises the risk of a shift to the fiscally-dominant regime. The higher the risk of a shift to the fiscally-dominant regime, the larger is the inflation bias and, as a result of the monetary policy tightening, the real interest rate. A higher real interest rate, in turn, puts upward pressure on the debt level.

Hence, we are left with the final question —is there anything the central bank can do to preserve price stability or at least mitigate the inflation bias without putting fiscal stability at risk? According to the model, the answer is yes. Since policy regime shifts arise endogenously, the probability of a regime shift is not invariant to policy. A central bank can reduce the risk of a shift to the fiscally-dominant regime by responding more moderately to inflation in normal times while making sure to abide by the Taylor principle consistent with its price stability goal. A more moderate nominal interest rate response to inflation implies that real interest rates will increase less in the wake of an inflationary shock, thereby mitigating the fiscal consequences of the monetary policy tightening. A lower risk of shifting to the fiscally-dominant regime helps to anchor inflation expectations at the central bank’s target. The inflation bias shrinks accordingly, and may even disappear. In addition, inflation volatility may decline. While a more modest response to inflation, ceteris paribus, increases inflation volatility, lowering the risk of fiscal dominance reduces inflation volatility. I show that the second effect may dominate in equilibrium.

These results come with some caveats. First, in the model, agents have perfect knowledge of the central bank’s reaction function. In practice, the private sector may misinterpret a moderate response to inflation as an implicit renouncement of the price stability goal. Second, in the model, the fiscal authority’s reaction function is invariant to the central bank’s reaction function. In practice, the fiscal authority could be tempted to exploit, and, thereby, undo the central bank’s attenuation of fiscal dominance risk.

Draghi, M. (2024): “Economic Policy in a Changing World,” Speech given at the National Association of Business Economists, Washington DC, 15 February 2024.

Humpage, O. (2016): “Fiscal Dominance and US Monetary: 1940-1975,” Federal Reserve Bank of Cleveland Working Paper No. 16-32.

Meltzer, A. (2003): A History of the Federal Reserve, Volume 1: 1913-1951, University of Chicago Press.

Sargent, T. (1982): “Beyond Demand and Supply Curves in Macroeconomics,” American Economic Review, 72, 382-389.

Schmidt, S. (2024): “Monetary-fiscal Policy Interactions when Price Stability Occasionally Takes a Back Seat,” European Central Bank Working Paper No. 2889.

Weidmann, J. (2020): “Too Close to Comfort? The Relationship between Monetary and Fiscal Policy,” Speech given at the OMFIF Virtual Panel, London, 5 November 2020.

The U.S. Federal Reserve System maintained interest rate ceilings in the 1940s. See, e.g., Meltzer (2003).

Sargent (1982) defines fiscal dominance as a policy configuration where “the fiscal authorit[y] select[s] a path or policy for government expenditures and explicit taxes implying growth rates of total government indebtedness to which the monetary authority must adjust”.

See Schmidt (2024) for details on the model and its parameterization.