Fluctuations in global financial markets can severely destabilize emerging market economies (EMEs). The academic and policy debate on enhancing EME resilience generally focuses on the role of capital controls and foreign exchange intervention, as these tools directly target international transactions. Yet, we find that macroprudential regulation—a less controversial policy tool—can already strongly bolster the resilience of EMEs against global financial shocks. Macroprudential regulation also facilitates a more countercyclical monetary policy response to fluctuations in global financial conditions.

In recent years, there has been a robust academic and policy debate on how to enhance the resilience of emerging market economies (EMEs) to the ebbs and flows of the global financial cycle. The discussion has focused on the use of foreign exchange intervention and capital controls since these tools directly target international transactions by offsetting or curbing capital flows, respectively. However, these tools are often controversial, partly due to concerns that they may be misused in a beggar-thy-neighbour manner.

In our study (Bergant et al., 2023), we show that a less controversial tool—namely macroprudential regulation—can be highly effective in bolstering the resilience of EMEs to global financial shocks and promoting a more countercyclical use of monetary policy.

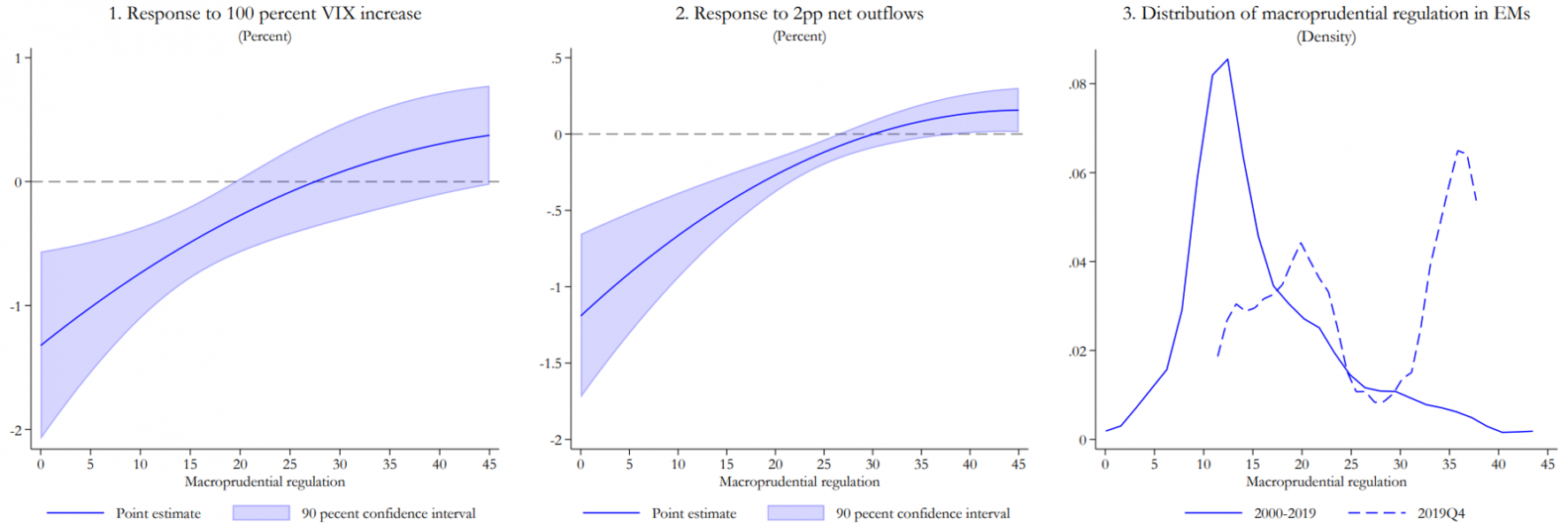

The analysis is based on panel data for 38 EMEs between 2000 and 2019. The baseline empirical model examines whether the responsiveness of economic activity in EMEs to global financial shocks—captured by movements in the VIX, US monetary policy, and capital flows push factors—is influenced by the strength of macroprudential regulation. As illustrated in Figure 1, we find that when macroprudential regulation is weak, an increase in the VIX or a sudden capital outflow can significantly reduce GDP in EMEs. For example, a doubling of the VIX—as experienced during the global financial crisis—can reduce GDP in EMEs by 1.2 percent. However, macroprudential regulation can offset the impact of such shocks. Indeed, if macroprudential regulation is sufficiently stringent, global financial shocks do not have significant effects on EMEs’ economic activity.

Figure 1: GDP response in EMEs to global financial shocks

Notes: The x-axis denotes the level of macroprudential regulation. Panels 1 and 2 show the GDP response to global financial shocks for different levels of macroprudential regulation; panel 3 shows the probability density function of macroprudential regulation in the sample. Net capital outflows are scaled by the HP-trend of GDP. The shaded areas correspond to 90 percent confidence intervals computed with Driscoll-Kraay standard errors.

We also examine if macroprudential regulation generates adverse cross-country spillovers. A possible concern is that if a country shields itself from fluctuations in global financial conditions through strict macroprudential regulation, other countries could become exposed to greater volatility. For example, measures that reduce risk taking in one country could lead to the relocation of risky financial activities to other countries, making them more susceptible to global financial shocks. However, we do not find evidence of such adverse spillovers. On the contrary, macroprudential regulation appears to have positive spillover effects when countries face capital flow shocks. This may be because countries with stringent macroprudential regulation support more stable trade and financial flows, benefiting other countries too.

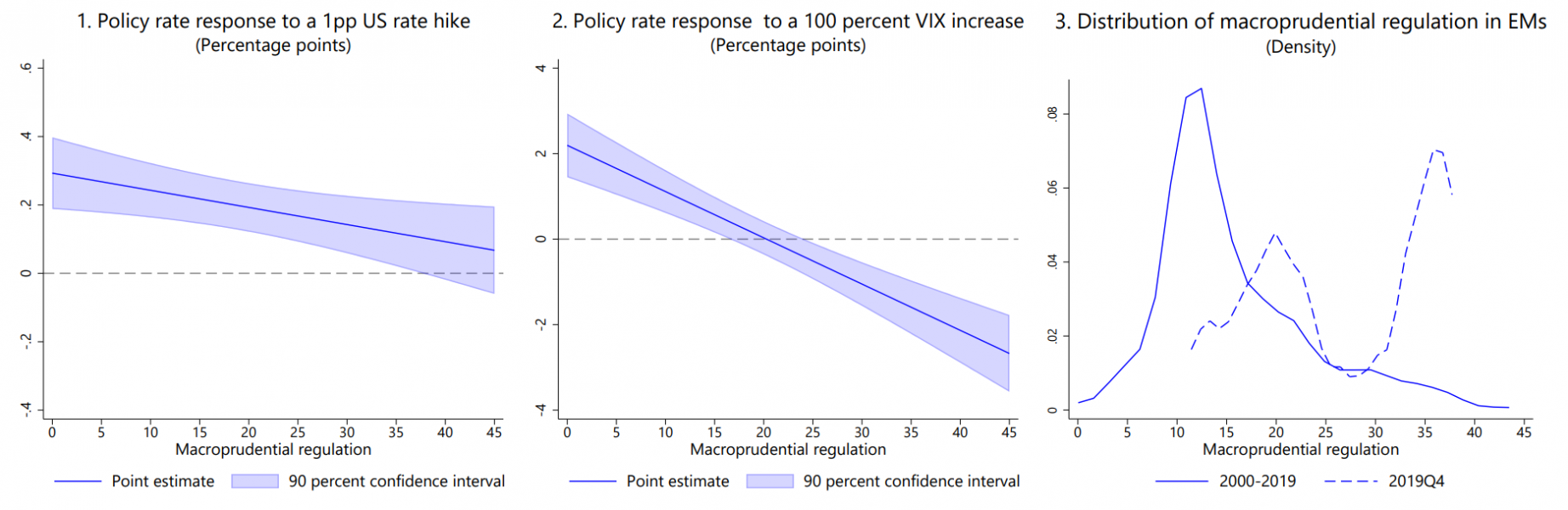

A potential mechanism through which macroprudential regulation reduces the sensitivity of EMEs’ economic activity to global financial shocks is by allowing for a more countercyclical monetary policy response. As shown in Figure 2, when macroprudential regulation is loose, an interest rate hike in the US or an increase in the VIX prompts EME central banks to raise rates, thereby weakening domestic activity. This is likely because central banks try to support the exchange rate and curb capital outflows due to concerns about financial stability. Conversely, when macroprudential regulation is sufficiently stringent, financial stability risks are less acute and central banks can respond more countercyclically, for example by cutting interest rates in response to a rise in the VIX.

Figure 2: Policy rate response in EMEs to global financial shocks

Notes: The x-axis denotes the level of macroprudential regulation. Panels 1 to 2 show the policy rate response to global financial shocks for different levels of macroprudential regulation; panel 3 shows the probability density function of macroprudential regulation in the sample. Net capital outflows are scaled by the HP-trend of GDP. The shaded areas correspond to 90 percent confidence intervals computed with Driscoll-Kraay standard errors.

Our findings demonstrate the effectiveness of macroprudential regulation in mitigating the macroeconomic impact of global financial shocks on EMEs and in facilitating a more countercyclical response of monetary policy. These results are particularly relevant from a policymaking perspective because we do not find evidence that capital controls provide similar benefits. As a result, our analysis strongly advocates for the use of macroprudential regulation as a critical defense line against the destabilizing effects of global financial volatility.

Bergant Katharina, Francesco Grigoli, Niels-Jakob Hansen and Damiano Sandri. 2023. “Dampening global financial shocks: can macroprudential regulation help (more than capital controls)?” BIS Working Paper No 1097.